-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Capturing the Ups and Downs in Coronavirus Equity Markets

31 July 2020

3 min read

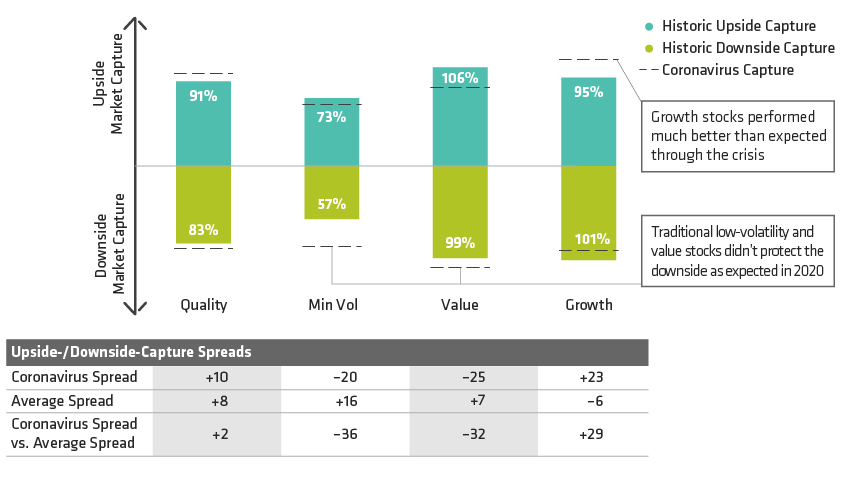

How Did Equity Factors Perform Through 2020 Volatility?

Global Factor Indices: Upside-/Downside-Capture Ratios During COVID-19 Downturn and Rebound

Past performance and current analysis do not guarantee future results.

As of June 30, 2020

Upside-/Downside-market capture calculated by dividing MSCI factor index return by MSCI World Index return. Average downside capture calculated using returns during the following periods. Average upside capture represents the three-month forward return from each period’s trough. Coronavirus (from February peak): February 19, 2020—March 23, 2020. Prior crises include: Rising Rates + Slowing Growth in China and Europe: September 2018—December 2018; Inflation + Fed Tightening: January 2018—March 2018; China’s Economy + Plummeting Oil Price: November 2015—February 2016; Greece + China Stock Market Crash: July 2015—September 2015; Concerns About Europe: May 2012—June 2012; Eurozone Debt Fears III: October 2011—November 2011; Eurozone Debt Fears II: May 2011—October 2011; Eurozone Debt Fears I: April 2010—May 2010; Global Financial Crisis: May 2008—March 2009; SARS: November 2002—March 2003; 2000 Tech Crash: March 2000—October 2002.

Spread is measured as upside capture minus downside capture.

Quality is represented by MSCI World Quality; Min Vol by MSCI World Minimum Volatility; Value by MSCI World Value; and Growth by MSCI World Growth.

Source: MSCI and AllianceBernstein (AB)

Fund Focus

ES AllianceBernstein Low Volatility Global Equity Fund

Balancing Global Equity Returns with Downside Mitigation for a Smoother Investment Journey

Capital at Risk

-

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

About the Authors