Investors are at a unique juncture today. The recovery from the dislocations from the COVID-19 pandemic seems well underway and is creating a unique landscape—as well as opportunities and risks. In our view, once this recovery has fully played out, investors will likely face a more familiar landscape—one with lower returns and the risk that an ill-timed market downturn could punish inefficient portfolios.

In order to participate and defend, we think investors need to build a better return path through better beta, efficient structure and targeted alpha. Each element can create a favorable return sequence and be even more powerful in combination. But to what end? Let’s examine how these three pillars might translate into one of the classic investment goals—pursuing stable growth when growth is harder to come by.

In Pursuit of Stable Growth…When Growth Is Harder to Find

Having climbed all the way back from its pandemic lows and then some, the S&P 500 is sporting valuations not seen since the time of the tech bubble. Broadly speaking, US stocks aren’t offering easy bargains for investors, and we don’t expect a big boost from expanding valuation multiples.

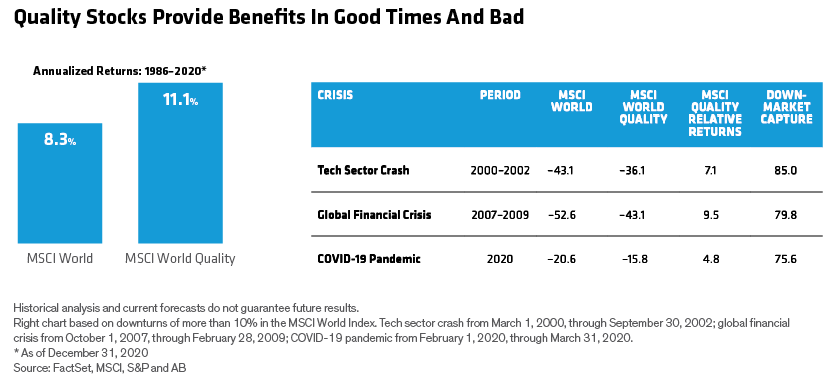

Combine this with the need for investors to guard against the downside, and we think an effective approach is to pursue the better beta of quality in equities. Quality equities have outpaced the broad equity market by a substantial margin over time (Display) while reducing the downside in notable sell-offs. During the pandemic, for example, the MSCI World Index fell by more than 20%; quality stocks, on the other hand, declined by less than 16%, a 76% down-market capture that cushioned against losses.

Quality Is Not a Backward-Looking Metric

In practice, investing in quality means leaning heavily on the stocks of companies supported by strong business models while staying ready to thoughtfully rebalance the mix of high-quality cyclical stocks and profitable growth stocks as visibility into the US economic recovery improves.

It may seem straightforward to find quality by using different combinations of metrics. However, based on our experience, quality is a forward-looking business characteristic, not a backward-looking metric—or even a combination of metrics. With so many ways to define quality using historical metrics, sizable performance differences are common among quality-seeking strategies.

In our view, in-depth fundamental research is the key to identifying quality-defining traits such as strong business models, dominant competitive positions, innovation edges and strong management teams. Quality, effectively identified, has been durable over time within both growth and value. And given current economic and market conditions—with substantial stimulus still waiting to be deployed—it’s possible that value’s recent strength could have more legs.

Identifying True Quality Can Be Worth the Effort

Our research suggests that it may not be easy to find these winners, but the reward can be worth the effort. From a portfolio of the 1,000 biggest US stocks, reassembled at the beginning of each year from 1979 through 2020, 353 stocks would have produced growth of 10% or more over one-year periods, beating the S&P 500 Index by 0.6% annualized. We’ve seen a similar quality benefit globally, with plenty of strong performers available beyond the US.

In fact, since 2011, despite US stocks outperforming international stocks in aggregate, 76% of the top 50 performing stocks were ex US on average—and much higher in some years. So, better equity betas like quality are available in international stocks, an arena where active managers have demonstrated an edge. That’s important, because one of the most talked-about elements of the return-to-normal trade from COVID-19 dislocations is that of US stocks versus the rest of the world.

Investors can also target a more favorable sequence of returns with alpha-friendly equity segments. The US small-cap market, for example, is generally less traveled by analysts, creating openings for strong research and active management to boost returns. Small-cap stocks have tended to thrive in economic recoveries, and we’ve found that exploiting growth and value opportunities in the style “tails” has historically fared better than a core small-cap approach.

Deploying High-Yield Bonds as an Equity De-Risker

Investors can also consider pursuing better equity beta by looking beyond stocks—allocating some equity exposure to US high-yield bonds, which have historically produced returns approaching those of equities with roughly half the volatility.

And high-yield sell-offs haven’t been as deep as equity sell-offs: since 1998, the average high-yield market drawdown has been –6.0% versus –11.5% for stocks. Also, high yield has rebounded relatively quickly. All of this evidence, in our view, makes high-yield an effective equity de-risking tool—and an excellent place for investors to spend the active part of their active/passive budget.

Investors’ pursuit of stable growth can be bolstered by diversifying equity exposure across both broad exposures and those that act as downside cushions. It’s critical to identify the characteristics of equity exposures, whether it’s quality, style, cap size, low volatility or thematic. We also believe that high-yield bonds—and even alternatives—can help de-risk equity exposure.

Want to learn more about post-pandemic portfolio construction? Download a copy of AB’s white paper, A Guide to Investing in the Time of COVID-19…and Beyond.

Richard Brink is a Market Strategist in the Client Group at AB, Walt Czaicki is a Senior Investment Strategist for Equities at AB, and Brian Resnick, CFA, is a Director and Senior Investment Strategist for Alternatives and Multi-Asset at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.