Emerging-market (EM) stocks, often considered risky in a crisis, rebounded in 2020 even as the COVID-19 pandemic spread globally. As vaccines and other favorable conditions unfold, investors have good reasons to consider EM equities in 2021 while strategically considering their potential risks.

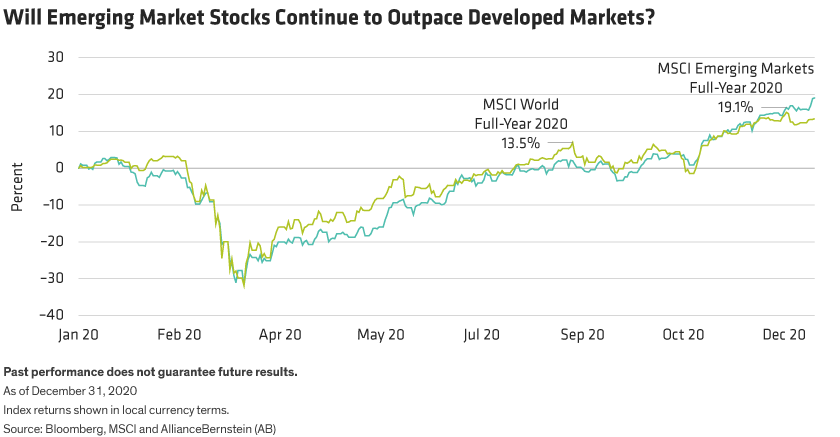

Emerging-market (EM) stocks were largely shunned as the COVID-19 crisis took hold, but they’re starting to attract more attention. After suffering since March, net flows into EM equity strategies have rebounded and turned positive in the fourth quarter. And in 2020, the MSCI Emerging Markets Index rose by 19.1% in local currency terms, outpacing developed-market (DM) stocks (Display).

Despite the recovery, many investors still aren’t convinced about EM stocks amid persistent uncertainty over the pandemic in key regions. But EM equity returns have held up well the last two years, reflecting solid fundamentals, valuations and economic factors. Add to this the promise of COVID-19 vaccines, and we think it’s easier for fence-sitters to see the merits of EM’s long-term potential.

EM’s Challenging Three-Year Journey Turns a Corner

EM stocks had been out of favor long before COVID-19. They rallied in 2016 and through most of 2017, only to suffer a triple blow from intensified US-China trade tensions, a costly technology war and the global pandemic. In 2020, all countries reeled, with India’s GDP estimated to have contracted by nearly 11%, making it one of the world’s worst-performing economies, according to AB’s economists. As conditions and economic outlooks improve, however, we expect these headwinds to wane—along with other positive developments—in 2021. In fact, we estimate that India GDP could grow 9%, and China 8%, in 2021—well above their averages over the last decade.

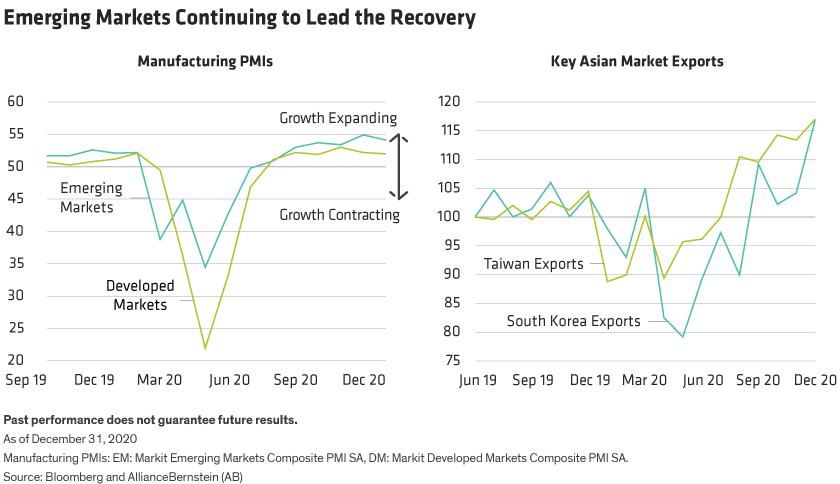

In fact, some EM countries, such as China and South Korea, may rebound faster than developed economies, because they were relatively well positioned to absorb the economic fallout from the COVID-19 crisis. And even though countries like India and Indonesia are struggling, EM nations in aggregate have experienced a much milder decline in the manufacturing purchasing managers’ index (PMI)—a key forward-looking economic indicator—which suggests they may have a head start in the upturn (Display left).

The potential for more-favorable trade policies also augurs well for EM equities, with new US policies under a Biden administration possibly helping thaw US-China trade tensions. A change in tone would certainly rebuild stability and predictability, benefiting trade, technology development and exports throughout Asia, where strong recoveries in key markets are underway (Display right).

Growing Signs of EM’s COVID-19 Recovery

There are also myriad signs that EM countries are managing the economic and health crises better than DM regions. China was a leader in the recovery, and the world’s second-largest economy quickly drew up big plans as growth picked up. Manufacturing output has already hit pre-crisis levels, and the new five-year plan (“The Fifth Plenum”) includes measures to reduce dependence on US technology. This will benefit China’s tech innovators and a swath of non-tech companies throughout the country and Taiwan, in our view.

New virus cases in Taiwan, Thailand, South Korea and Vietnam are now at very low levels, with lockdowns eased months ago. China, Taiwan and South Korea in particular, which account for 60% of the MSCI Emerging Markets benchmark, were especially efficient at containment. As a result, their economic activity is edging toward normal faster than some of their neighbors. And because EM populations skew younger, country death tolls were lower—just 0.23% versus 1.15% for developed countries, according to a recent study by Imperial College.

Finally, the global rollout of new COVID-19 vaccines is an additional catalyst for EM. The more affordable AstraZeneca dose is expected to reach more EM countries than others, and the company has said it intends to target more low-income countries. EM isn’t out of the woods, but the virus is noticeably receding as a dominant factor.

Economies, Currencies and Other Pivots Toward Progress

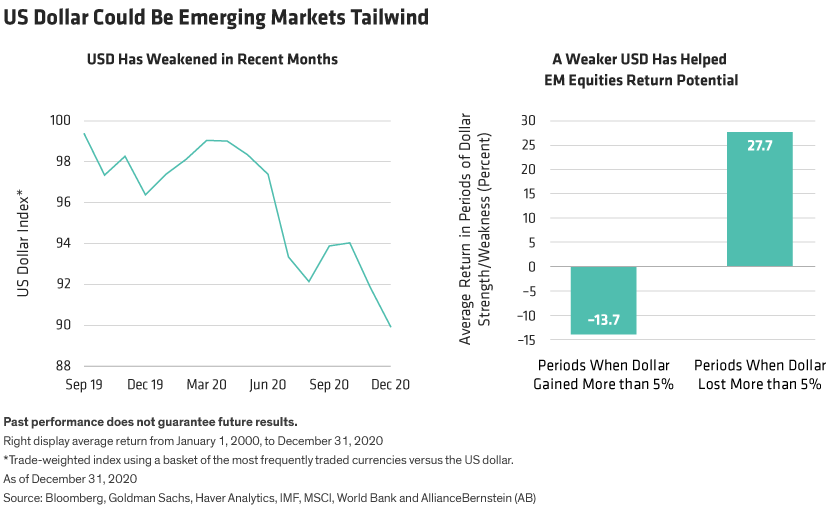

Lower relative debt levels give EM another fundamental leg up. Developed markets—led by the US—entered the pandemic with much higher debt than many EM countries. The US debt-to-GDP gap is expected to grow further relative to EM as it spends its way out of the economic crisis. This will likely help support EM currencies, which had been depressed but are starting to strengthen against the US dollar (Display left). If history is a guide, a weaker US dollar would benefit EM companies and bolster their return potential (Display right).

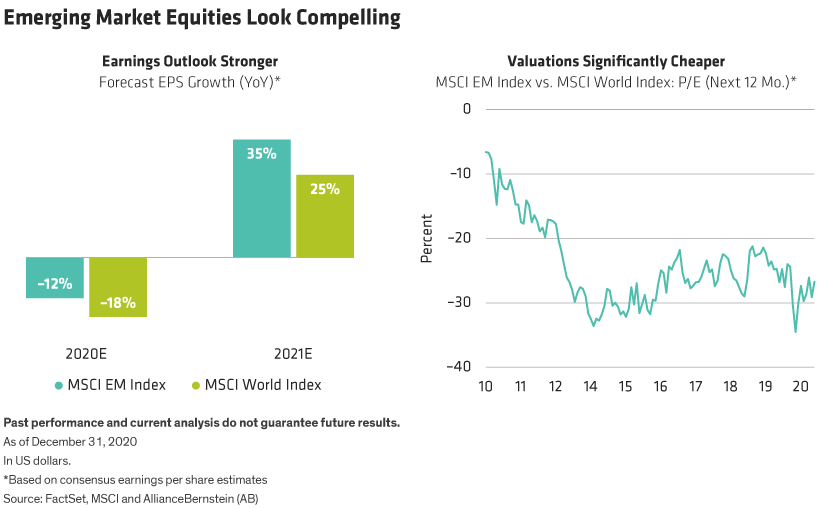

An extended low interest-rate climate is another catalyst for renewed EM potential. We think historically low rates in Brazil and India, for example, should boost key industries, like mortgages and autos, but the economic benefits should extend across the asset class. EM earnings estimates are stronger (Display left) and equity valuations—while still above historic lows—are considerably more attractive than developed markets (Display right).

Finding Opportunities—Even Within Pandemic-Pressured Industries

Clearly, many EM-based industries have been battered by the pandemic and will need time to recover. But even within struggling industries, we believe investors can find high-quality, attractively priced companies whose earnings potential in a post-pandemic world is widely underestimated.

With positive consumer sentiment making a comeback, for example, select cyclical stocks in the travel, banking and technology industries seem promising, as well as in the auto and retail industries. In our view, cyclical stocks will enjoy a strong earnings recovery as vaccine distribution gains traction.

Not all firms will rise from the pandemic unscathed. Many companies were already struggling to innovate and compete, and the crisis sealed their fate. Active stock selection is critical to discern laggards from leaders—those whose 2022 earnings potential exceeds 2019’s.

EM’s Potential Is Underutilized

Effective crisis responses, improving economies and strong fundamentals offer inroads to own high-quality EM companies at attractive valuations. Yet even after recent inflows, institutional and individual investors remain well under allocated compared with recent years.

Some reluctance is understandable. EM has a history of unexpected challenges and market volatility, and some EM companies today are unreasonably overpriced, in our view. But by identifying companies that can withstand uncertainty, investors can build portfolios that can persevere. And today, there are many ways to access EM equities for investors with different risk-tolerance levels. Progress toward a COVID-19 recovery can boost investor confidence by refocusing attention on the fundamental strengths and growth potential of select EM companies, which have been there all along.

Sammy Suzuki is Co-Chief Investment Officer—Strategic Core Equities.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.