Even as global stocks climbed in 2019, market volatility persisted. By some measures, lower-volatility stocks now look quite expensive. But in fact, high-quality stocks that can help protect portfolios can be found at reasonable prices, if you know where to look.

Equity investors had a wild ride in 2019. The MSCI World Index surged by 27% in 2019 in local-currency terms, defying headlines about US-China trade tensions, global political risk and macroeconomic concerns. The gains, however, have been anything but steady. Over the past two years, the market rose or fell by more than 1% on 71 days—a huge increase from 2017, when such sharp gains or losses happened only five times.

Strong Demand for Smoother Return Patterns

Sticking with equities sometimes requires nerves of steel. And not everyone can handle the pressure. That’s why many investors have turned to lower-volatility stocks, which aim to capture equity return potential with smoother trading patterns. Exchange-traded funds with “low volatility” or “minimum volatility” in their names had assets of US$106.8 billion as of December 31, driven by strong inflows of US$28.2 billion through the year, according to Morningstar data.

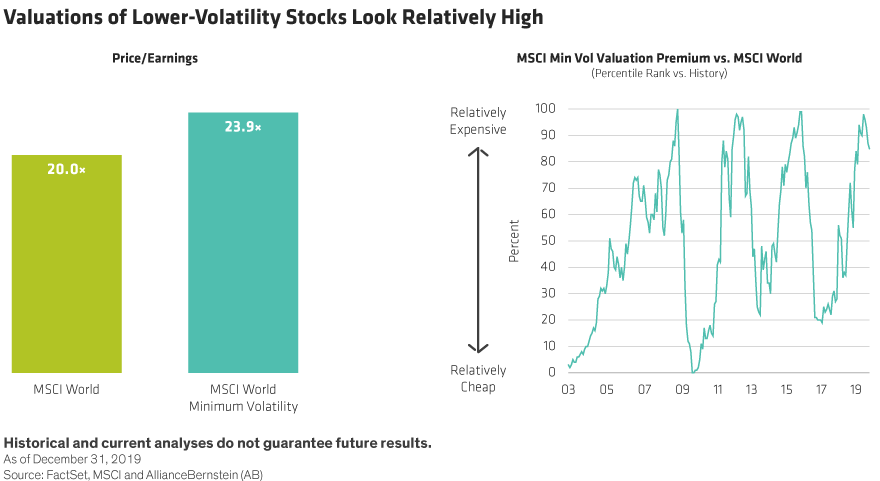

Their popularity has created a challenge—low-volatility stocks look expensive. By the end of December, the MSCI World Minimum Volatility (Min Vol) Index traded at a price/earnings ratio of 23.9, a 20% premium to the MSCI World (Display, left). In historical terms, the Min Vol is toward the top of its valuation range versus the MSCI World since 2003 (Display, right). For many, that looks like a high price to pay for stability.

But benchmarks can be misleading. Since they focus on a narrowly defined set of lower-volatility characteristics and do not consider valuation, indices can be easily skewed toward more expensive stocks and sectors.

Buying Quality at the Right Price

What’s more, some of these sectors don’t offer the quality you might expect in a lower-volatility allocation. For example, profitability in the utilities, telecom and consumer-staples sectors is very low compared to their history since 2003 (Display). Yet the Min Vol has a large overweight in each of these sectors versus the broader MSCI World. Meanwhile, the profitability of technology stocks is very high in historical perspective, yet the Min Vol is underweight the sector.

In a global allocation, regional differences matter too. For example, our research shows that stocks offering quality and stability are relatively expensive in Europe today.

The moral of this story is that valuations can’t be viewed in a vacuum. Investors must scrutinize individual stocks to gauge whether they have quality cash flows to support stable return patterns. Sometimes it’s worth paying a bit more for especially high-quality businesses. And some expensive stocks that belong to a traditionally defensive sector don’t have the underlying quality to justify the price tag.

Low-Vol Portfolios Aren’t Created Equal

Low-volatility portfolios aren’t all the same. To be effective, we believe a low-volatility portfolio should target reasonably priced stocks of high-quality businesses that can produce robust cash flows through changing market environments.

Investors are right to be concerned about valuations. If stock markets correct after a strong year, expensive names may get hit.

But it’s not a good reason to shun stocks, in our view. Since it’s almost impossible to time market inflection points, a low-volatility equities allocation with a clear focus on attractive valuations can be an antidote to future volatility and allow investors to stay in the market and benefit from the stronger long-term return potential of equities.

Passive strategies aren’t sensitive to valuations when allocating to low-volatility stocks. Some relatively expensive sectors, such as utilities, are among the largest overweights in the Min Vol. And the index or passive portfolios can’t sift out or adjust weights of individual stocks with high valuations. By emphasizing attractive valuations in holdings, we believe active investors can create portfolios with stable return patterns that can withstand more pressure in stormy weather than their passive peers.

Kent Hargis is Co-Chief Investment Officer—Strategic Core Equities at AllianceBernstein (AB)

Sammy Suzuki is Co-Chief Investment Officer—Strategic Core Equities at AB

Chris Marx is Senior Investment Strategist—Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.