It’s been nearly two years since oil prices began their historic collapse. Now that prices have stabilized, how have the hardest-hit areas held up? And what should investors consider when assessing a municipal bond’s oil risk?

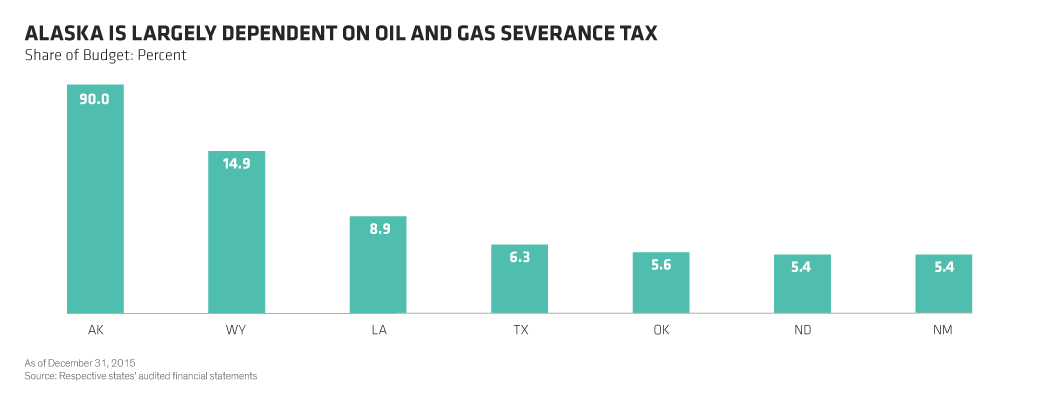

Among the 10 largest oil-producing states, some emerged from the plummet that began in 2014 worse off than did others. But overall, the effect has been limited. Only a small portion of state revenues come from oil and gas severance taxes. One key exception: Alaska (Display), where it’s no surprise that lower prices hurt.

Alaska aside, most states feel the pinch of an oil downturn as an aftershock. Reduced severance tax revenue has an immediate but limited impact on most states’ budgets, but over time, the layoffs and trimmed-down payrolls at oil and gas drilling and services companies dampen states’ primary revenue sources: income and sales taxes.

In cities, towns and counties, property taxes are the largest source of revenue—little, if any, comes from direct taxes on oil and gas. The effect is even further removed because the property tax levy is set annually, and it takes time for oil and gas sector weakness to manifest itself in lower real estate values—if that even occurs.

So how do we assess the risks, if they are indirect? We are most concerned about states and local governments with a high degree of exposure to the oil and gas industries—those with a large percentage of their GDP or labor force tied to these industries.

The majority of states have little to no exposure to the oil and gas industries, and most that do have very little debt outstanding (Display), making the opportunity for investment slim to nonexistent. But there are some exceptions. Texas and Louisiana are two oil-and-gas-dependent states that also present a large opportunity set for investors, with a combined US$18 billion in net tax-supported debt outstanding.

The story is similar at the local level. A number of cities, towns and counties have a high degree of exposure to the oil and gas industries, but most are sparsely populated and have very limited debt. The city of Houston, however, stands out as a large issuer with a labor force heavily dependent on oil and gas.

Let’s take a closer look at what’s going on in three affected areas.

Texas: Model Behavior

Texas’s economy is more diversified today than during the 1980s oil bust. Thanks to legislation specifically limiting the amount of oil and gas revenues that can be used to fund general operations, the state was well equipped to handle the 2014 oil crisis.

Texas reserves a portion of oil and natural gas production revenues and deposits half into a state highway fund and half into its rainy day fund—one that has flourished following several years of strong oil revenues. Conservative budgeting and a solid financial position also help the state withstand some volatility with little to no impact on its credit rating.

Louisiana: Rising to the Surface

Though Louisiana has slightly lower exposure than does Texas to the oil and gas industry, it’s not as conservatively managed. It’s therefore in a much worse financial (and credit) position.

Louisiana’s lack of fiscal conservatism has forced the state to deplete its liquidity sources over time, leaving it exposed to the negative effects of low oil prices. And its financial reserves are less than 5% of revenues compared with 27% for Texas. On the positive side, the new governor has moved quickly to raise taxes and stabilize the budget.

Houston: Between a Rock and a Hard Place

Since 2014, Houston has faced its fair share of challenges—but they’re not directly related to the oil collapse. Harris County has high exposure to the oil and gas sector, and many residents are employed in the industry, but Houston’s economy has performed better than expected.

This performance is mostly attributed to expansion on Houston’s east side, where a growing petrochemical and refining industry is benefiting from the lower cost of crude oil. The city’s port has also been a bright spot, and activity should continue to expand as the port benefits from the widening of the Panama Canal.

The city’s legacy costs and limited ability to raise revenues are troubling. Houston spends more than 30% of its annual revenue on retiree pensions, healthcare expenses and debt service (and, in fact, it would be spending more than 45% if it made the full actuarially determined contributions to its pension plans). These expenses represent the bill for services already consumed and can’t be cut through layoffs or efficiency measures. On the revenue-raising side, Houston is constrained by Proposition 1, which limits the annual growth of the property tax levy to 4.5%.

While we don’t think Houston is headed for default at this point, its financial flexibility is severely limited.

Booms and Busts Happen, but Legacy Costs Are the Boogeyman

Energy markets are subject to booms and busts, and most of the oil-affected communities have weathered the 2014 oil price drop. States and large cities generally have the authority to raise taxes or cut expenditures to offset a cyclical economy’s effects. As a result, their ability to ride out the economic cycle is not a significant concern.

But when financial flexibility is impaired because municipalities are required to spend a large sum on legacy costs, how they will fare during an economic downswing—due to oil or any other factor—is worrisome. For investors who can rely on research, extra income can be earned, but they will need to be ready to sell at the first sign of trouble.

By this measure, Texas appears in very good shape, and Louisiana can muddle along, but Houston has major work to do. It’s yet another reason why investors should value diversity when constructing portfolios.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.