Markets had been unusually calm until risk surged in late August. Bigger portfolio shifts when volatility is rising may be magnifying the spikes, making markets harder to navigate. We think the answer is focusing on more than risk.

It’s true that volatility has moderated a bit but is still higher than it was before August, and policy makers have taken note of these sudden shifts in risk. In fact, it was one reason the US Federal Reserve decided to hold off on raising interest rates in September. To avoid being whipsawed, investors should take a holistic view of their portfolios. The focus should be on more than risk signals—return signals matter, too.

Reactions to Market Volatility Amplify It

Our research indicates that risk factors—and oversimplified asset-allocation decisions based largely on volatility measures—can create a painful cycle. The very trigger that prompts an allocation shift away from equities is itself influenced by the resulting sale. And volatility begins to feed on itself.

There’s evidence that more managers are making decisions based largely on changes in market volatility. We looked at allocation changes over time, based on the implied equity exposure across different mutual fund categories, examining both high-risk and low-risk environments. We found that reductions in equity exposure have become noticeably larger since the Global Financial Crisis of 2008 (Display 1).

In fact, the downward shifts for tactical allocation strategies have almost doubled in size. It’s not surprising that tactical strategies make adjustments, but the bigger moves today are notable. Even world allocation strategies, which largely left their equity allocations alone pre-crisis, have begun to make significant equity reductions.

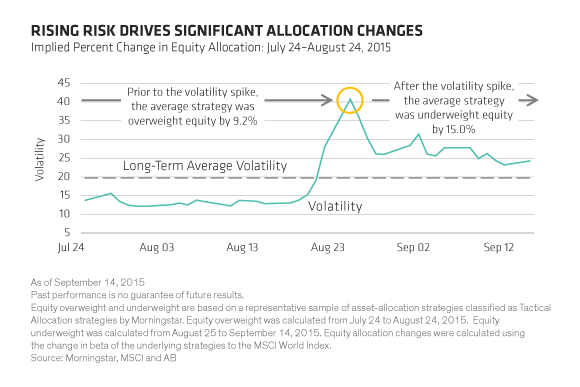

Our analysis also suggests that portfolio shifts aren’t just bigger than before, but they’re also happening faster when volatility rises. This helps make volatility spikes more pronounced. The August episode confirmed this: selling pressure due to a collective decision to de-risk likely made the first few days more severe. Before August 24, when risk was below average, the group of strategies we isolated for this analysis had an average overweight to equity of 9%.Shortly after the spike in risk they were significantly underweight, averaging 15% less equity exposure than is typical (Display 2).

The Problem of Volatility Tunnel Vision

One likely reason for the rush for the exits is that many risk-managed strategies exclusively use volatility gauges as a simplified trigger for making allocation changes.

Because this systematic approach is so common, it creates significant selling momentum in equities when risk starts to rise and the signal turns red. This risk “tunnel vision” can lead to even sharper moves in the very metrics used to determine portfolio positioning.

We don’t think these types of asset-allocation triggers are robust enough. It’s important to determine if a sudden change in the risk environment is temporary or long-lasting. That knowledge can make a portfolio manager less likely to make the classic mistake: trend-following and selling into distress at a market trough.

A Holistic Process Must Integrate More than Risk Signals

One way to tackle this problem is to include both expected risk and expected return across asset classes in quantitative analysis. It’s also important not to leave fundamental judgement behind, and to consider how technical factors in the market impact the asset allocation equation.

All things considered, we think it makes sense to be modestly underweight equities in the current environment. Volatility is above average, but we think the initial spike may have been exacerbated by indiscriminate selling from risk-managed strategies. Stalling growth in emerging markets and falling commodity demand may not be as much of a spillover risk for developed economies as some investors may think.

In turbulent times like these, the ability to be dynamic in shifting equity beta can be very helpful. And volatility is a valuable signal that helps inform that decision. The key is to make sure that the trigger for shifting beta isn’t overly sensitive to changes in volatility alone.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.