Asian businesses are gradually rebooting after governments quelled the initial wave of the coronavirus pandemic, drawing attention to equity opportunities in the region. Equity investors should take a closer look at companies whose valuations absorbed unjustified blows before and during the pandemic.

Governments in the Far East have done a relatively effective job at coronavirus containment compared with Europe and North America. After having experienced the brunt of the SARS outbreak nearly two decades ago, they knew how to respond swiftly with aggressive lockdowns and virus tracking. With parts of the economy starting to come back online ahead of Western peers, certain companies and industries deserve attention.

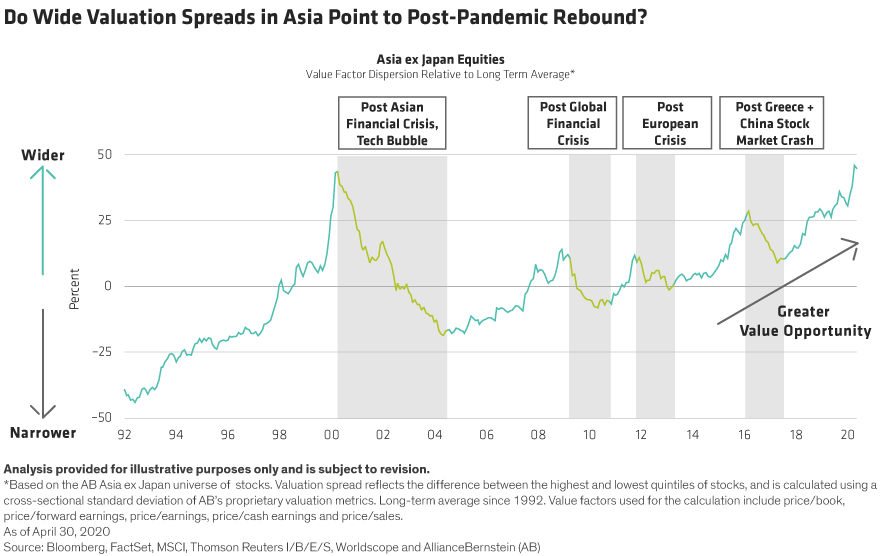

Even before the onset of COVID-19, Asian value stocks were trading at especially attractive levels. Now that the valuation dispersion has widened further (Display), we believe that value stocks—companies that are (arguably) inexpensive owing to a short-term controversy—are poised to outperform once markets stabilize this year. Indeed, there’s a precedent for such a move: value stocks in Asia ex Japan have outperformed in the initial stage of previous crisis-to-recovery cycles, such as after the global financial crisis in 2009–2010 and after the European debt crisis in 2012–2013. And the massive amounts of fiscal stimulus being pumped into regional economies could help support cyclical companies that are more dominant among value stocks.

Faster Out of the Block

In South Korea, Hong Kong and Taiwan, governments never completely shuttered swaths of their economies as they did in China, the US and Europe. In recent weeks, China’s government has allowed silenced factories, stores and restaurants to reopen as the lockdown of Wuhan, the original epicenter, has ended. That said, the coronavirus battle is uneven across Asia. Countries like India, Indonesia, Thailand and the Philippines are still coming to terms with the pandemic, with low testing rates, late stay-at-home directives and stressed healthcare systems.

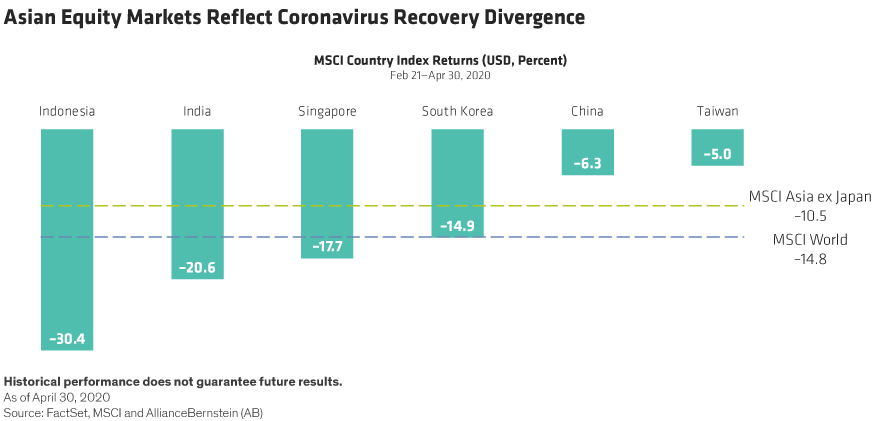

Equity benchmarks for the individual countries reflect that divergence. Indian and Indonesian stocks have fallen much more sharply than peers in Taiwan, China and South Korea, since markets began to tumble on February 21 and through the rebound in recent weeks (Display).

Still, there will be plenty of challenges, even for successful economies. As factories ramp up in China and South Korea, exporters will face slack demand because the US and major economies in Europe are still in a self-enforced lockdown. And these countries still must remain vigilant to guard against a potential second wave of outbreaks that could impact economic activity and markets.

Easing Pandemic Pain: Telecom, Memory Chips

Given that progress will be bumpy, investors need to be selective. That requires homing in on specific industries and companies addressing the challenges of the coronavirus crisis. For example, to accommodate social distancing and the demand for remote work, Asian memory-chip manufacturers and telecom networks are industries that will experience robust demand, in our view.

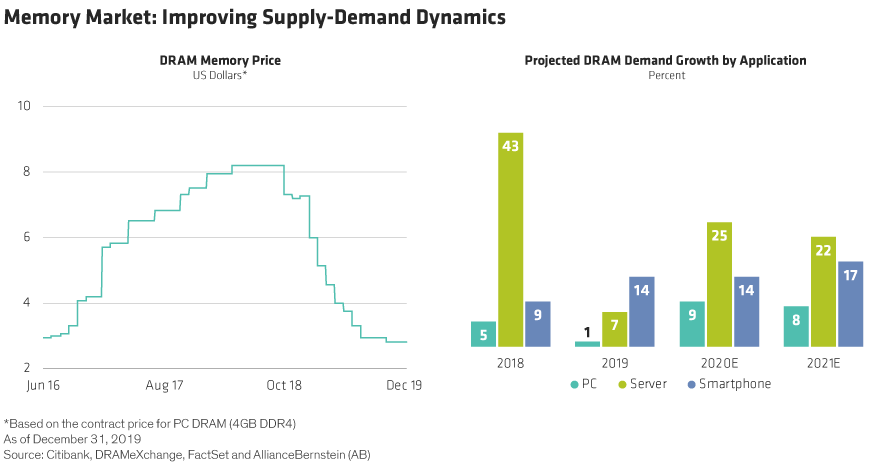

Hardware memory supply had thinned even before the COVID-19 crisis. Manufacturers had been scaling back output since 2018 (Display). Now that workforces around the world have been forced to shift to working from home, demand is skyrocketing for cloud-based data services. Even if smartphone sales growth slips from projections at the beginning of the year, we expect robust orders for servers that form the storage reservoir for cloud data centers. The shift beyond the office will also generate demand for extra PCs to outfit employees with remote workstations. Memory makers like South Korea’s Samsung Electronics and SK Hynix and Taiwan’s Nanya Technology should benefit from these trends, in our view.

In recent years, concerns about investment in 5G network upgrades weighed on network operators’ valuation, as did regulation and pressure on rates. Now, as the pandemic forces enterprises to embrace remote work, robust network connectivity and bandwidth for home offices are must-haves. That’s a blessing for network operators like China Mobile, especially given a relaxation of competition among Asian telcos. And although Indonesia’s economy is struggling with the initial brunt of the pandemic, the country’s national carrier, Telekomunikasi Indonesia, is also benefiting from industry changes.

Balance-Sheet Stress Test

There is still one critical unknown to keep in mind. Despite the optimistic outlook for those sectors insulated from the pandemic, value investors must not lose their bearings in the fog of earnings uncertainty. Companies are still trying to assess how their businesses will be affected, making it difficult to know exactly how cheap they really are. As earnings continue to decline, valuations could compress further before reaching extremes, in our view.

Given the extreme uncertainty about future earnings, value investors should scrutinize cash flows and balance-sheet resilience. Solvency will determine which companies survive and which perish in the economic shutdown. Balance sheets must be tested for resilience amid downturns of differing durations and revenue reductions of differing magnitudes.

Though global markets are daunting, Asian value stocks in countries ramping up economic activity have the potential to outperform, in our view. For those investors who can identify resilient industries and drill down to distill balance-sheet strength, we believe the region offers attractive opportunities in companies that are positioned to do well in the nascent pandemic recovery and over the longer term.

Stuart Rae is Chief Investment Officer of Asia-Pacific Value Equities at AllianceBernstein (AB)

Rajeev Eyunni is Portfolio Manager, Asia ex Japan Value Equities at AllianceBernstein (AB)

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.