Central banks around the world, including the US Federal Reserve, have turned more hawkish lately—pivoting from supporting a COVID-ravaged economy to fighting stubbornly high inflation. The Bank of England (BoE) continued that trend at its February meeting.

The BoE not only raised rates following a December rate hike but also made clear that it strongly considered being even more aggressive. Four of the nine members of the Monetary Policy Committee (MPC) voted for a 50 basis point (b.p.) hike, rather than the 25 b.p. increase delivered.

Not a Simple Case for Raising Rates

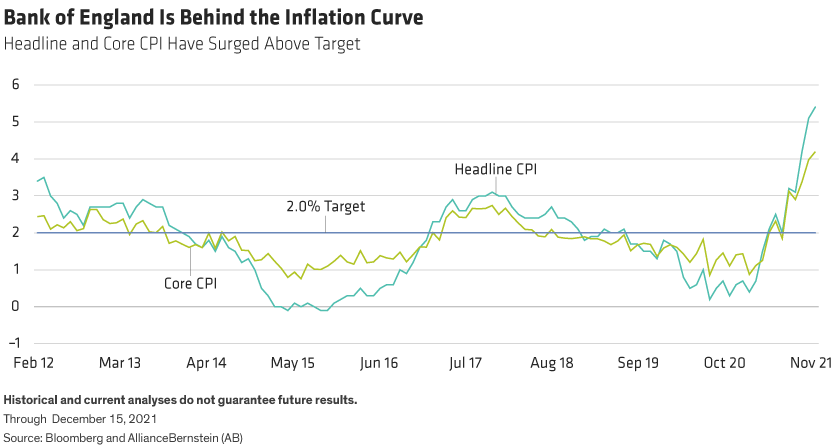

At first blush, this is a more hawkish turn from the BoE. Both headline and core inflation measures are well above the central bank’s 2% target and moving higher. And the regulated energy-price cap is set to rise sharply in the spring, at just about the same time that a 1.25% increase in the national insurance tax comes through. Both actions will push inflation still higher.

The nature of those prices increases, however, points out that the case to raise rates isn’t as simple as observing that inflation is high.

Tighter monetary policy can’t reduce the energy price cap or the tax increase. Indeed, monetary policy isn’t likely to be effective at addressing the underlying causes of inflation in the UK, which the MPC’s statement describes as “sharp rises in prices of global energy and tradable goods of which the United Kingdom is a net importer.” Rising rates in the UK won’t lower global energy prices; they won’t reduce import prices meaningfully, either.

Higher energy prices and taxes will also hurt household finances. In fact, the minutes of the BoE’s decision indicate that it expects consumption to slow “as households cut back on spending in the face of the material adverse effects on their real incomes from the sharp rises in global energy and tradable goods prices, and the planned increase in national insurance contributions.”

Raising the policy rate, and the mortgage rates associated with official rates, will squeeze household finances even more.

Rate Hikes Are an Exercise in Risk Management

If consumption is already expected to slow, which should bring inflation down over time, why is it necessary to raise rates if it will further drain household incomes?

The BoE’s struggle to answer that question at the post-meeting press conference illustrates a communication challenge for central bankers all over the world. Yes—inflation is too high. But raising rates today can’t influence inflation in the short term. It will slow growth over time, which should contribute to cooling inflation off, but most forecasts already expect inflation to fall.

The best way to think about rate hikes in the UK, and most other countries at this stage, is as a risk-management exercise. Central bankers failed to anticipate the sharp inflation climb of the past few months, and it’s too late to do anything about it now. But the recent run-up in prices raises the stakes going forward. If inflation expectations become unanchored, recent high inflation readings could become lasting. Once an inflationary mindset is entrenched, it can be hard—and painful—to break.

The BoE clearly hopes that hiking now will prevent an inflationary cycle from becoming established, and in so doing avoid the need for even more aggressive tightening later. That’s why, despite considering a larger rate hike this week, the BoE still says that it expects only “modest” further tightening. This is also why the MPC estimate of the policy-rate endpoint for this cycle is still under 1.5%.

The BoE seems to hope that by tightening modestly right now, it will avoid having to take much more aggressive action—the kind that typically causes a recession—later on.

Eric Winograd is Director of Developed Market Research at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.