Despite uncertainty about global politics and policy, stock markets are soaring and volatility is low. Does this mean it’s time for investors to double down on growth-oriented assets? Not necessarily.

For many risk-managed strategies, a multi-month rally like the recent one in US equities, coupled with low volatility, is an unambiguous signal to lean in. But here’s the problem: it’s just one signal. To be effective, risk management should take its cues from multiple market signals.

Don’t get us wrong: With the US economy strengthening and global growth gaining traction, equities definitely belong in investors’ portfolios. But high stock valuations and policy uncertainty in the US and elevated political risk in Europe suggest that now isn’t the time to ramp up your existing equity exposure.

Too Much of a Good Thing?

The current market environment is a case in point. Yes, risk signals based on the volatility implied by the pricing of stock options, credit spreads and other indicators are declining. And most of the time falling risk leads to market rallies and higher returns. But not always.

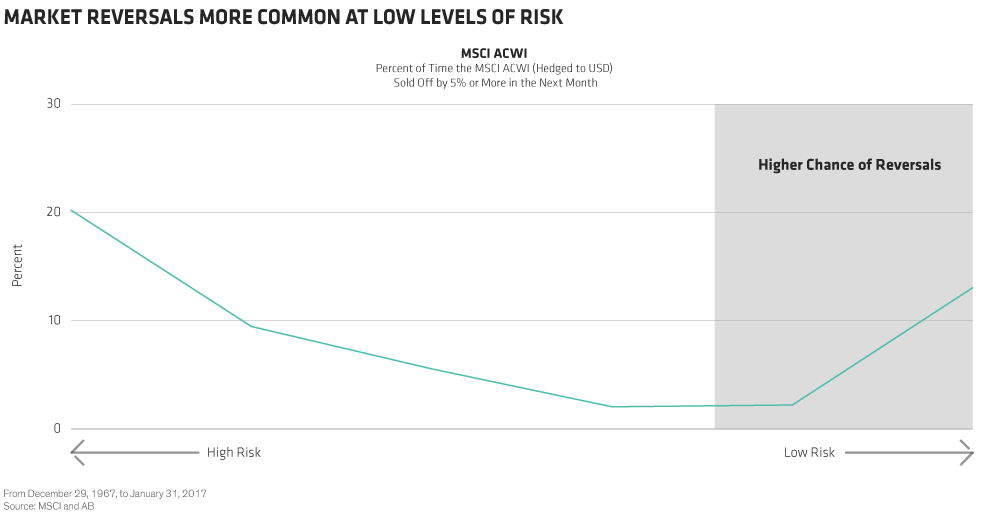

Looking back over the past five decades, we found that when risk metrics fell below a certain point, the probability of a monthly decline of 5% or more in the MSCI ACWI increased dramatically (Display).

In early 2006, for example, global stock markets were rising steadily. But in May, the rally turned into an extended sell-off. The reason: fear that central banks’ attempt to quell inflation with higher interest rates would choke off growth. The move caught many off guard because risk indicators and volatility were low at the time.

A Broader View: Looking Beyond Risk and Volatility

This is why it’s critical for risk-aware strategies to pay attention to an array of signals. For instance, risk isn’t the only signal that’s been on the decline recently. The outlook for equity returns, based in part on valuations, fundamentals and macroeconomic conditions, has also been trending lower.

What’s weighing down these forward-looking return signals?

To start with, valuations are already high—particularly in the US—and it’s not clear that the White House will be able to deliver on tax reform, deregulation and other pro-growth policies as quickly as markets had expected.

Political risk is elevated as well. The outcome of the French presidential election this spring could have major implications for the stability of the European Union and the future of the euro. In the US, there’s lingering concern about the administration’s trade policies.

There’s also the Fed and interest rates. Much as it did in 2006, the Fed is reacting to faster growth and rising inflation expectations by raising interest rates—though the level of inflation is considerably lower today than it was then. Still, rising rates means higher borrowing costs for companies. And a firmer US dollar could hurt the revenues of firms with large foreign sales.

Keeping Your Investment Odyssey on Track

Again, none of this means that investors should give up trying to generate high returns. For instance, investors looking to generate additional returns through equity exposure while reducing their potential downside risk might want to consider tilting toward European and UK stocks, where valuations aren’t as stretched and exchange rates are more supportive.

But it does mean that investors should maintain flexibility. While US stocks are still up comfortably since November, a pullback over the last few days shows how quickly sentiment can shift.

In the odyssey to achieve your investment goals, it’s important to strike a balance between risk and return, and avoid drifting too far in one direction. Market conditions are calm now, but there may be rougher waters ahead. There’s no need to turn the boat around. But like Odysseus, investors should resist the siren song of low risk and open their ears to other market signals—even if that means strapping themselves to the mast.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.