With Brexit headlines dominating the European news, equity investors face an ongoing challenge. Building resilient portfolios requires a clear view of the long-term outlook for European companies that also reflects major short-term political uncertainties.

Political risk has been a feature in European markets for years. Lately, from Italy’s fiscal squabbles to turmoil in the streets of France, it feels like the volume of political noise has risen. Yet for equity investors, the Brexit saga is probably the number one political headache today.

So how can investors develop long-term conviction in European stocks even as political risk clouds the short-term outlook? We think the key is to understand how different political outcomes might affect the earnings of individual companies, and to use that analysis to help avoid excessive portfolio exposure to different political outcomes.

Three Major Brexit Risks

Brexit is creating three major risks for companies. The first is trade disruption: firms that must move parts or finished goods across the UK border could be vulnerable to severe, though probably temporary, disruption in the event of a no-deal Brexit.

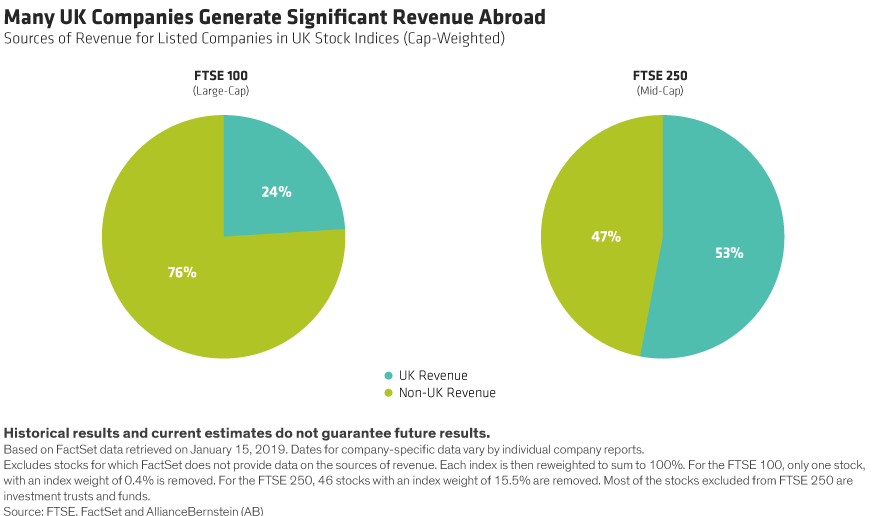

Currency risk is the second major concern. Many UK-domiciled companies are global, with relatively little business exposure to the British economy (Display). As a result, their earnings rise when the pound falls, as it did immediately after the referendum result in 2016, and their share prices can actually benefit from rising Brexit anxiety. But recently this dynamic has shifted, with some worrying signs that investors have marked down both sterling and shares in large-cap global UK companies when the perceived risk of a hard or chaotic Brexit has increased.

The third risk is to UK economic growth. In the worst-case scenario, many forecasters believe that a no-deal Brexit could tip Britain into recession. And even if the eventual outcome is more benign, continued uncertainty could lead to investments being postponed and consumer sentiment depressed. Banks and consumer companies operating primarily in the UK are most vulnerable to these risks.

Research Questions for Stock Pickers

When researching stocks in the UK and across Europe, we ask whether a company is exposed to the specific risks that we’ve identified. Then, we assess whether those risks are threatening its future cash flows and, if so, to what extent they’re adequately priced into the company’s stock.

Some of the companies that are potentially most exposed to Brexit may not even be listed in the UK. Peugeot of France, for example, both makes cars in the UK and sells more of its production to UK consumers than do its main European-listed rivals. So it’s important that portfolio-level risk analysis takes account of Brexit impacts on non-UK companies; you can’t judge a portfolio’s exposure to Brexit just by looking at its weight in UK stocks.

What About a Post-Brexit Bounce?

There are two sides to the Brexit risk coin. Investors also need to consider what will happen if a favourable Brexit deal is reached—or, conceivably, if the UK ends up not leaving the EU after all. These outcomes would likely benefit UK stocks that have traded at a Brexit discount, as well as cyclical European companies that have suffered amid recent risk aversion. Investors in European stocks need to ensure that they are neither overexposed to Brexit downsides or underexposed to possible Brexit-related market rallies.

In fact, we think many companies exposed to Brexit risks offer attractive return potential today. Take Johnson Matthey, for example, which makes materials for auto catalysts that are enjoying growing demand as emissions standards tighten. Or Marks & Spencer, the food, clothing and homeware retailer, where new management is taking the measures needed to turn around performance, in our view. And outside the UK, Peugeot is continuing to reduce costs both in its long-established units and the businesses it acquired essentially for free from General Motors last year.

European Challenges: Populism, Protests and Parliamentary Elections

Of course, Brexit is only one political risk hanging over European markets today. From street protests in France to governments in Hungary, Poland and elsewhere, the resurgence of populism in Europe is challenging EU norms. As the May European Parliamentary elections approach, investors may become concerned that further gains by antiestablishment parties could undermine the stability of the EU’s institutions.

In our view these fears are overdone. The Italian government’s recent decision to abide by eurozone fiscal rules, following the earlier example of Greece, suggests that populist rhetoric in the opposition often gives way to pragmatism in government: the overriding political imperative to remain in the euro retains strong popular support, as polls continue to show.

Still, investors need to be on the lookout for less well-publicized political risks that can have a real impact on companies’ earnings. In Spain, for example, recent tax changes introduced by the center-left coalition government have impacted some banks, and efforts to pass a budget this year will be complicated by the politics of Catalan separatism.

Political risk is not a reason to avoid European equities. Europe today offers plenty of opportunities for bottom-up stockpicking based on fundamental analysis, the key to investing success. But a thoughtful overlay of political risk analysis is essential to complete the picture and reinforce investing conviction in these tense times.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. AllianceBernstein Limited is authorized and regulated by the Financial Conduct Authority in the United Kingdom.