As the Chinese New Year begins, investors will welcome the year of China A-shares, soon to be included in the MSCI emerging-market (EM) benchmarks. But put careful consideration into determining which funds are actually ready to join the festivities.

Index provider MSCI plans a gradual integration for the vast onshore market, whose $8.3 trillion market capitalization is second only to that of the US. Though A-shares will initially account for just 0.7% of the MSCI Emerging Markets Index, it’s a major step toward assimilating China’s vast onshore equity universe into global capital markets. At full inclusion of 500 stocks, A-shares are likely to account for more than 20% of the benchmark, according to many sell-side estimates. Over the long term, the index revisions are expected to unleash $100 billion of investment in A-shares through EM vehicles.

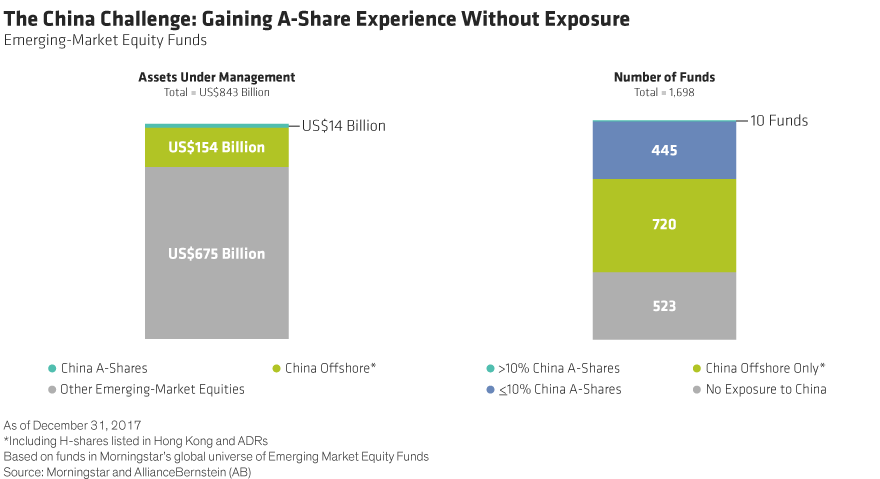

Increasing Exposure to Chinese Markets

But are EM funds ready for the change? Overseas investment funds have been increasing exposure to China, according to a recent Bloomberg report. Yet even though 87% of mutual and index funds invest in Chinese equities—and some A-shares are already accessible—their holdings remain concentrated in offshore H-shares, traded in Hong Kong, and US-listed American depositary receipts (ADRs).

Nearly three-quarters of the funds don’t hold any onshore shares. China A-shares account for only US$14 billion (or 1.7%) of assets under management in EM funds (Display, left). And only 10 EM funds hold more than 10% in onshore equities (Display, right).

There are good reasons to be cautious about A-shares. Investors need to navigate structural imbalances in China’s debt-laden economy, concerns about the government’s macroeconomic stewardship and the large contingent of state-owned enterprises in the market.

Ignoring A-shares, however, means missing the full potential of China’s expansion. For example, the onshore market is full of growing healthcare companies serving the country’s aging generation. Many technology firms from the Shenzhen market are inaccessible offshore. The market also provides access to China’s explosive consumer growth and local brands popular with the growing middle class; shares of Kweichow Moutai, the distiller of a popular grain liquor, more than doubled on the Shanghai Stock Exchange over the last 12 months due to swelling demand.

What Does It Take?

But what does it take to invest effectively in China A-shares? We think three key competences will determine success:

-

Boots on the ground—There’s no substitute for research heft. Funds must be armed with field research from professionals with deep experience on the ground in China. These teams need to be fully versed in the nuances of China’s growing economy, know the players inside and outside the companies, and be able to identify firms with good governance. It’s also important to make sure that an EM fund has enough analysts to cover the market effectively.

-

Quantitative capabilities—There are more stocks listed in the China A market than in either the Nasdaq Stock Market or New York Stock Exchange. MSCI’s inclusion of 222 A-shares into its EM benchmark increased the number of stocks in the index by more than 25%. Moreover, there are now more than 1,900 A-share stocks accessible to foreign investors through the Stock Connect scheme, more than doubling the universe of investible equities in China. This favors research teams already familiar with the onshore landscape, in our view. We also think funds that know how to combine quantitative tools with fundamental analysis will have an edge when combing the vast pool of A-shares to identify portfolio candidates.

-

Active advantages—Research shows that active investing strategies are especially effective in emerging markets, which are less efficient than developed markets. In China’s A-share market, which is dominated by retail investors, inefficiencies abound. These retail investors often lack critical information about company performance, and information dissemination is imperfect. For example, it can take months for the market to respond to sell-side analyst upgrades. This environment favors a hands-on approach that focuses on long-term fundamentals and investment themes.

A-Shares Are Different

Investing effectively requires a thorough understanding of how China’s top-down politics ripples through the economy. Though politicians’ rhetoric can be discounted in Western markets, China’s political class often sets the rules in the market.

For example, the government’s focus on reducing air pollution is creating winners and losers in the transportation industry. A curb on diesel trucks is benefiting Chinese rail operators and vehicle manufacturers that meet emissions standards.

Funds must be able to identify companies with interests that don’t align with minority shareholders. Many state-owned enterprises will prioritize public responsibilities over profit maximization. Meanwhile, professionals need to be familiar with tycoons who might siphon off profits for side projects.

To pilot a portfolio through these challenges, familiarity with the onshore landscape is indispensable. But we think many EM investors may not be equipped with what it takes to find stocks with the strongest return potential. Ask your fund manager the right questions to find out whether they are ready—or not—to fully participate in a new year of opportunities across all of China’s stock markets.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.