For China, the year ahead holds special political and economic significance. From the Winter Olympics in February to the Chinese Communist Party’s 20th national congress, slated for the fourth quarter, “the world,” as President Xi Jinping has noted, “is turning its eyes to China.” That means China’s financial, environmental and economic policy aspirations, which have been complicated by the pandemic, will be closely scrutinized. Here’s what we see when we look in the eye of the tiger.

Zero-COVID Policy Comes Face to Face with Omicron

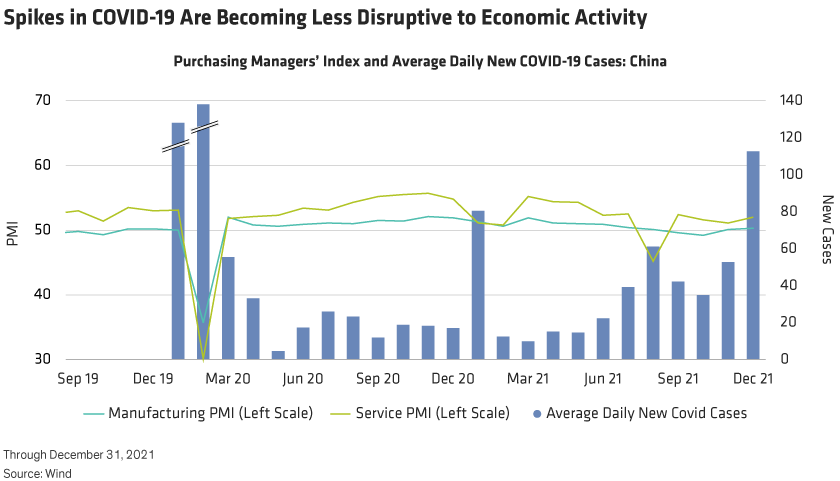

Since mid-December, a spike in COVID-19 cases in China has raised concerns that another coronavirus surge could disrupt the country’s economy, with ripple effects around the globe. Though China’s current outbreak pales in comparison to outbreaks in the US and UK, mass testing is under way and affected districts are being locked down under China’s zero-COVID policy. Since its inception in 2020, this policy has effectively limited the size and duration of outbreaks and helped to contain the virus’s spread, including the import of omicron. Nonetheless, the Lunar New Year travel crush—traditionally the largest annual human migration in the world—and the Winter Olympics in Beijing may pose challenges.

To make sense of the implications for China’s economy, we compared China’s coronavirus outbreaks to indicators of economic activity since the pandemic began. The winter 2020 and summer 2021 outbreaks weighed significantly on activity, particularly in the service sector (Display). But more recently, the impact has been smaller, though the number of cases is comparable. Why?

Vaccines may be one reason. With vaccination rates approaching 90%—compared to 60% in July—household risk aversion could be decreasing. Additionally, thanks to high vaccination rates and increased experience with the pandemic, local governments may have been able to deploy less Draconian measures to contain outbreaks, thus reducing disruption to consumption.

That said, the current coronavirus outbreak could weigh on consumption in the near term and represents a potential downside risk for the Chinese economy. But we don’t expect the government to initiate a nationwide lockdown as we saw in early 2020, which leads us to believe that the impact will be manageable.

Where There’s a Will, There’s a Way: Don’t Underestimate Beijing

What’s more, Beijing has sent a clear message: Growth stability is essential in 2022. This means policymakers will boost public investment to support growth and stabilize the economy, as a countermeasure to downward pressures from the pandemic.

We can’t stress this enough: We think it’s a mistake to assume that Beijing has deemphasized GDP growth in its new policy paradigm. While China’s policy paradigm has shifted from growth as its single objective to multiple objectives—including financial stability and the environment—growth stability remains critical.

Thus, market participants may be underestimating Beijing’s resolve to keep China’s economy on course—which in turn has led many observers to forecast that China’s GDP growth will run well below potential in 2022. We disagree. Our own forecast calls for 5.3% growth, with modestly higher, but still mild, headline inflation.

In other words, we anticipate a Goldilocks economy. But that doesn’t mean our expectations are based on a fairy tale. Beijing has demonstrated in past years that it has the ability to achieve faster or slower growth, as policymakers wish. And they have no reason to want growth to run either hot or below potential today.

While growth targets could become more flexible in coming years, healthy growth remains critical to China’s plan for common prosperity. Higher income per capita is one of two preconditions (the other being reduced income inequality) for achieving common prosperity. Accordingly, President Xi has set a target for doubling income by 2035. And comfortable GDP growth—on the order of 5.0% to 5.5%, on average, during the period of the 14th Five-Year Plan—allows income to rise. All this makes growth below 5.0% in 2022 very unlikely.

Our growth outlook for 2022 depends on three groups of factors:

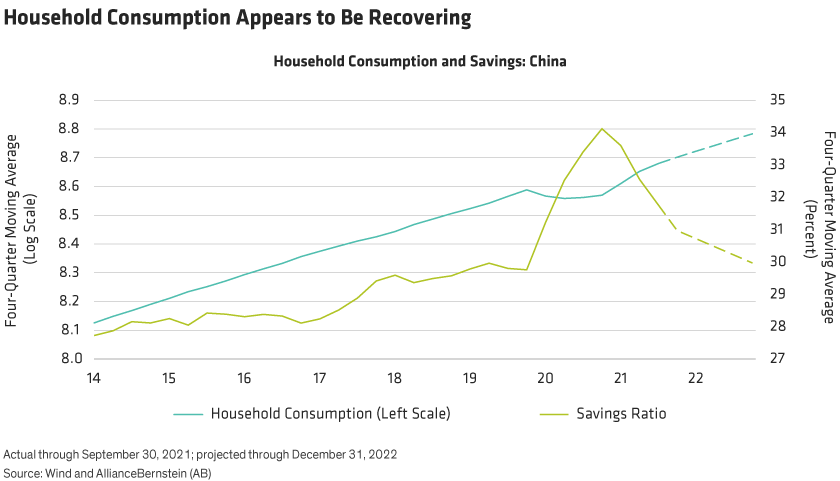

1) Export momentum and domestic organic drivers, such as private investment and household consumption. Slower-than-expected recovery in these areas represents the biggest downside risk to our outlook. Moderating global growth may limit export momentum in 2022, and there may not be much incentive for companies to meaningfully increase private investment, given only mild growth in industrial demand. Further, the current coronavirus outbreak makes it less likely that the household savings ratio (Display) will normalize in 2022, which is prerequisite to consumption growth returning to pre-pandemic trends.

2) Policy shocks. Recently, government actions linked to Beijing’s policy goals of financial stability and the environment have constrained the property and manufacturing sectors. While we’ve seen some early signs of stabilization in housing sales, we expect the property sector to remain weak in 2022. Thankfully, the contribution of housing to growth has been structurally lower in recent years, decreasing the need for a strong rebound in the property sector.

More importantly, if the central government’s balancing of policy goals has unintended short-term effects on China’s growth, Beijing will likely calibrate the recovery of these sectors in line with the overall policy balance (as it has in recent months), rather than sticking to one goal while sacrificing another. In a year in which growth stability has assumed special importance, the government will be cautious about implementing policies that have contractionary effects.

3) Policy room, particularly on broad fiscal policy, which is China’s biggest policy lever.

Engaging Policy to Ensure Growth Stability

To promote growth stability in 2022, we expect Beijing to deploy broad fiscal policy support, accompanied by supportive monetary policy and housing policy that focuses on stability. Here’s how we see that playing out.

To begin, we expect the pace of public investment to accelerate rapidly and early in the year. Already, the central government has allocated a 1.46 trillion yuan (US$229.2 billion) share of the 2022 quota for local-government special bond issuance—a major financing source for public investment—to provincial governments to jumpstart spending on ambitious infrastructure projects.

Such expansionary fiscal policy requires supportive monetary policy. This includes robust credit growth and mild policy rates. Following its likely one-off cut on January 17, we expect the People’s Bank of China (PBOC) to keep policy rates unchanged for the rest of the year at moderately low levels to anchor borrowing costs in the real economy.

(In the transition to a rate-based monetary policy framework, policy rates have become key to gauging the monetary policy stance in China. Policy rates’ role as anchors for market rates has strengthened, as has transmission from policy rates to bank lending rates.)

We expect credit growth to remain strong—roughly in line with nominal GDP growth, an intermediate target of the PBOC. To this end, the central bank can avail itself of several structural monetary policy tools to support small to midsized enterprises, manufacturing upgrades and decarbonization. Overall, we expect the debt-to-GDP ratio to increase in 2022 at a pace comparable to the three years prior to the pandemic.

In our view, housing policy in 2022 will stress stabilizing, not boosting, the sector. This points to stabilization of the volume of mortgage loans (Display) to meet reasonable housing demand and recovery in bank lending to developers.

The Chinese government has taken a dual-track approach to housing regulation in recent years: a combination of short-term regulations to squeeze the housing bubble and maintain stability in prices, and building long-term mechanisms such as development of a rental market, land system reform, fiscal regime reform, property tax and prudent policies on housing financing. The goal is a healthy and less speculative housing sector.

We see nationwide housing policy continuing in this direction—making broad and significant easing unlikely. However, some lower-tier cities that have experienced a drop in housing prices may tweak policy at a local level. This should release suppressed demand from first-home buyers (as well as from those buying second homes to improve their living conditions), prevent a collapse in the property market and reduce drag on China’s overall GDP growth in the Year of the Tiger.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.