Markets have responded warmly to China’s easing of its zero-COVID policy, although it’s not clear yet how quickly or smoothly the country’s economy will recover. While some bumps in the road are likely, we expect China’s reopening could lead to further gains in Asian credit and currencies in 2023.

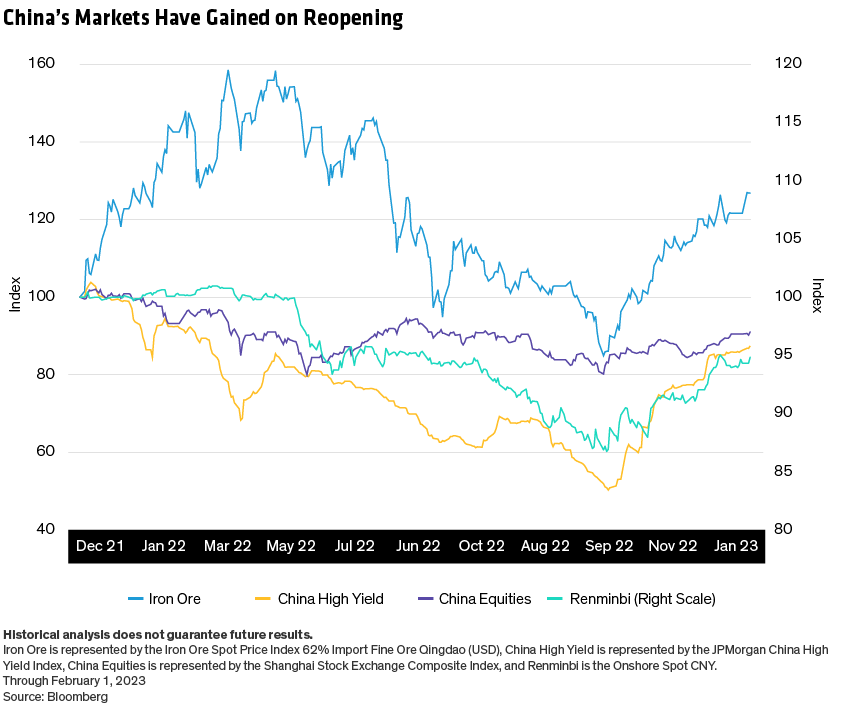

After a difficult 2022, global investors are looking for light at the end of the tunnel. China’s reopening and the related recovery in China-linked commodities, currencies and equities markets provide grounds for optimism (Display).

For fixed-income investors, too, the reopening theme has been the main driver of a recovery in broader Asian credit and currency markets. As often happens, markets are rallying in anticipation of better times ahead.

While the policy action of ending lockdowns is decisive, leading directly to increased economic activity and consumer demand, it’s not yet clear how quickly or how fully the economy will reopen, given the surge in COVID infection rates. And the hard data for China’s economic outlook continues to highlight how challenging the last few years have been. These factors suggest that recovery will be gradual and uneven.

Even allowing for this, however, the economy’s direction is clear, and the investment implications are positive. For fixed-income investors, we see opportunity in Asian credit and currency, where we expect further potential gains in 2023.

Reopening Could Unleash Suppressed Demand

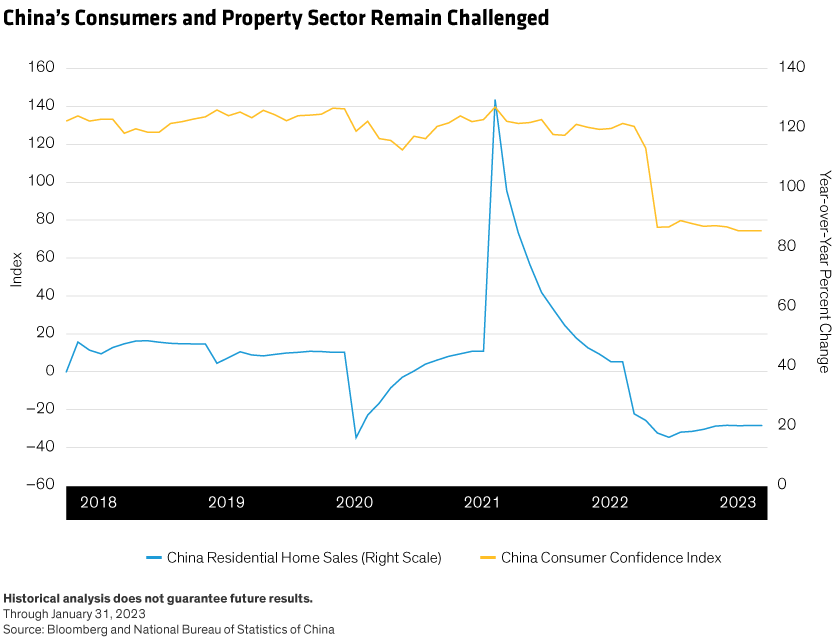

The economic challenges experienced by China in the last two years are clear from the downturns in consumer confidence and the property sector (Display).

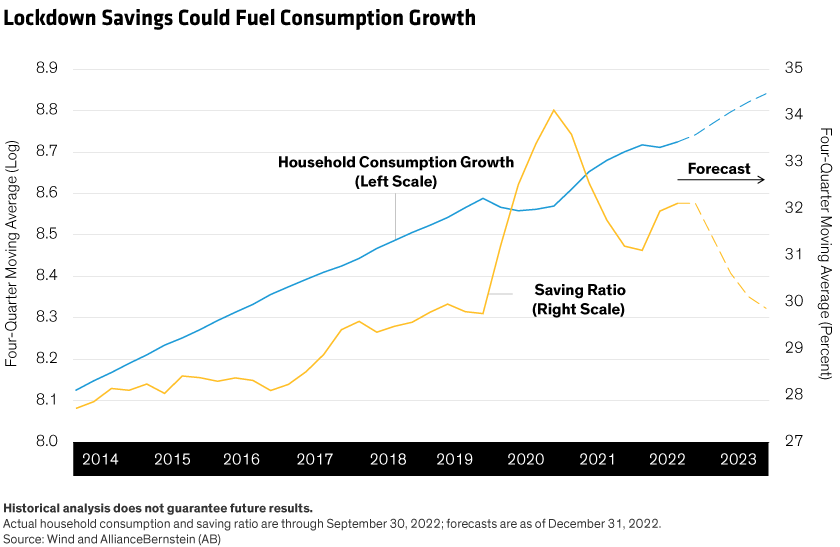

COVID wasn’t entirely to blame, as regulatory intervention played a key role in property’s decline. And the picture isn’t altogether bleak because the consumer cloud has a silver lining. Household savings increased during lockdown, pointing to pent-up demand, which—as the economy reopens and consumers become more confident—could support steady growth in consumption (Display).

A recovery in consumer demand would be positive for China’s financial markets, in our view.

Foreign investors, chastened by global volatility and the zero-COVID policy, have become underweight China and largely remain so. Consumer demand and other signs of strength and durability in the recovery would likely lead to a rebalancing of portfolios in China’s favor.

There are risks to this outlook, however, which are best understood in the context of China’s broad policy framework.

Monitor Property for Signs of Stability

The framework has been shaped by President Xi Jinping’s aim of achieving a balance between growth and equitable social outcomes. As a result, investors should expect more moderate and sustainable growth and a focus on supporting innovation and manufacturing, lifting income per capita, reducing wealth inequality, and pursuing further market reforms.

The policy framework can be seen as positive in the long term, but it may lead to some short-term uncertainties. As already mentioned, China’s property market suffered significantly during the last two years, mainly because of regulatory intervention. This intervention was in keeping with President Xi’s social equity objectives.

But growth remains a government priority. This was confirmed in the government’s recent Central Economic Work Conference and has been underlined by the faster-than-expected reopening. It’s also evident in the housing sector, where the People’s Bank of China and the China Banking and Insurance Regulatory Commission recently implemented measures to help the sector’s “stable and healthy development.”

For buyers and investors, these measures include lower mortgage rates, a lower down payment ratio on mortgages, relaxation of home-purchase eligibility, and cash subsidies for home purchases. For property developers, they include making it easier to comply with borrowing restrictions introduced during the crackdown.

While these actions are encouraging, we believe that investors should continue to look carefully for signs of stability in the housing sector when assessing the overall balance of risks and opportunities in the economy.

Inflation Should Be Benign

Another risk is that reopening will cause inflation to rise in China, as happened in other countries when they emerged from the pandemic. But, in our view, any inflationary effects are likely to be benign. While it’s possible that the Core Consumer Price Index will edge higher, we don’t think it will rise to the levels seen in developed markets.

One reason is that, while household savings in China have increased, the government support extended to individuals and business during lockdowns has been significantly lower than in the US and Australia, for example.

Another reason is that the dynamics of food inflation in Asia, including China, are different from those of other countries. For example, non-Asia emerging-market food inflation has risen dramatically during the last two years in response to the war in Ukraine and supply chain issues. The same is true for the prices of Western staple food crops wheat and maize. Asia food inflation and the price of rice have remained stable, however.

There is little likelihood, in our view, that inflation will rise sharply in China. Consequently, we expect policy settings to remain supportive for growth.

Asia’s Boats Are Likely to Rise on China’s Tide

For now, China’s government bond yields lag those of US Treasuries, because of the countries’ different inflation and interest-rate trajectories. Because of this, the near-term opportunity for fixed-income investors created by China’s reopening lies, in our view, not in China’s bond market so much as in the credit and currency markets of its Asian trading partners.

China’s biggest trading partner is the 10-member Association of Southeast Asian Nations (ASEAN), and four Asian countries that are not ASEAN members are among China’s top 13 trading partners. China in turn is the top trading partner for eight of these countries and either the second or third biggest trading partner for the rest.

We expect the country’s reopening to ease supply chain pressures across the region and provide a direct boost to some industry sectors. One area likely to benefit is tourism, as China’s outbound tourism recovers from the collapse it suffered because of COVID.

Increased trade with China would be positive for these countries’ corporate bond markets and their currencies should benefit, too. With the US dollar’s strength appearing to have run its course in the near term, the biggest headwind faced by Asian currencies during 2022 has dissipated, and emerging Asian currencies have appreciated significantly.

We regard this as positive for Asian currencies across the board. And, if the US dollar rebounds, we expect high-yield Asian currencies to outperform their regional peers on a total return basis.

Asian Markets Could Outperform in 2023

With China reopening and the rest of the global economy likely to be challenged during 2023, we believe there is ample room for both foreign and domestic investors to allocate to the region. Stronger growth in China should lead to stronger growth in Asia, creating conditions that, in our view, could lead to Asian markets outperforming in 2023 and beyond.

Brad Gibson is Head of Asia Pacific Fixed Income at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.