With COVID-19 still a top employer concern, protecting workers’ health and well-being naturally comes first. But the pandemic’s impact isn’t limited to only physical and mental health: financial wellness is also ailing. The crisis has exacerbated the problem, but it’s not exactly a sudden occurrence.

Participants’ confidence in their financial outlook has been relatively low for years. More recently, financial challenges from the COVID-19 crisis have made the situation for many even more uncertain. That’s why plan sponsors—and employers in general—now have an opportunity to connect with employees on financial topics that span more than just retirement planning.

Employees Are Uneasy About Financial Well-Being

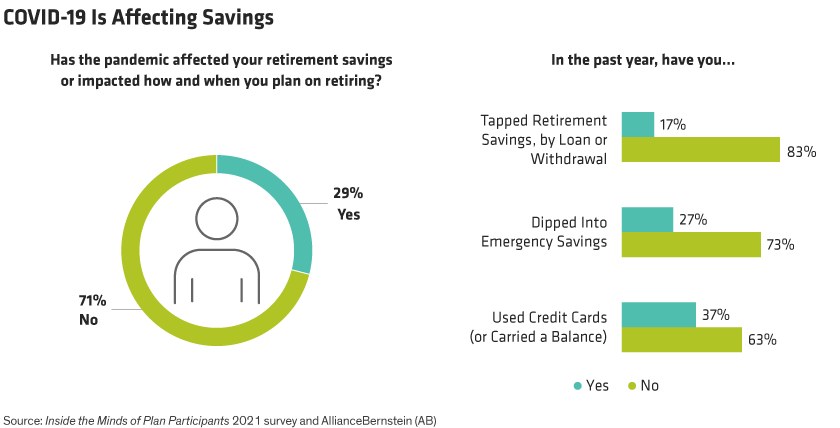

Before tackling engagement, plan sponsors should first revisit what they’re solving for. Although financial unwellness is a longstanding problem, COVID-19’s recent impact on financial well-being is especially telling in how it changed the retirement planning course for many. Nearly 30% of plan participants in our recent survey, Inside the Minds of Plan Participants, said the pandemic changed how and when they’ll retire (Display, left). And over the past year, 17% of those surveyed tapped into their retirement savings to pay for living expenses—many more turned to emergency funds or credit cards to make ends meet (Display, right). We believe our findings suggest that while people tapped credit cards and emergency savings as their first line of defense, if the pandemic drags on, more retirement savings could be leveraged as those other assets run dry.

Retirement Confidence Linked to Broader Financial Well-Being

Financial wellness challenges are weighing down participants’ confidence in their retirement outlook. Since AB began surveying participants in 2005, only about one in three (29%), on average, have felt either “confident” or “very confident” about their retirement prospects. This year’s survey found a 35% confidence level—better than the long-term average but a big step down from 2018, when nearly half (47%) seemed confident about retirement.

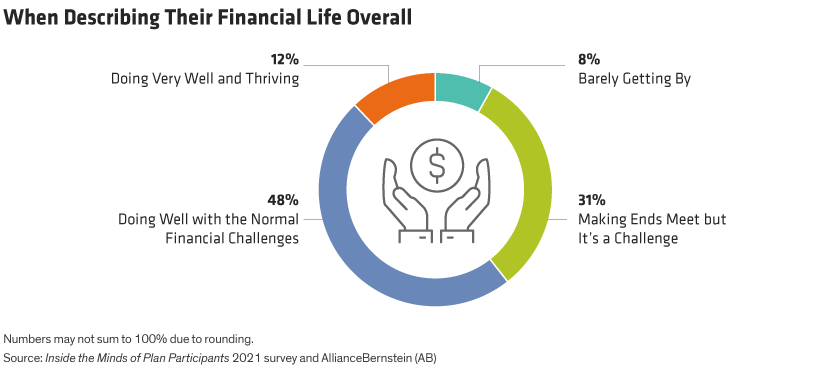

Looking more broadly, life clearly poses a sizable financial challenge for many people. When asked to describe their financial life overall, 31% said they can make ends meet, but still struggle, and about one in 10 said they’re barely getting by (Display).

With so many moving parts to financial wellness today, securing a comfortable retirement can no longer be pursued in a vacuum—it depends on too many other financial underpinnings in life. Credit card and college loan debt, insurance premiums, healthcare costs, taxes—even basics like budgeting—all come into play with individuals’ financial well-being. Participants increasingly want and need employers to help them connect those dots—and financial wellness programs may be just the tool for the job.

A Win-Win for Participants and Sponsors Alike

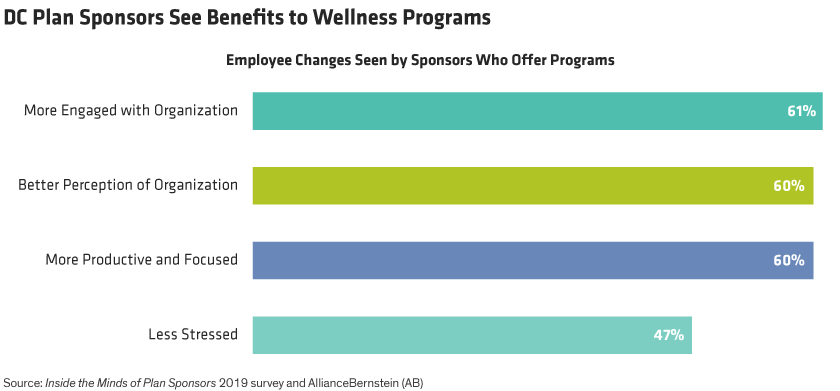

Although widely adopted by larger employers, financial wellness programs still haven’t reached most of the American workforce. But workplaces that do have them report a strong positive impact. In our recent survey of plan sponsors, employers with these programs report that their employees are more engaged and productive, which we believe helps improve their financial knowledge, confidence and the likelihood that they’ll retire when they want (Display).

Learning Your Way to a Better Financial Life

With all their advantages and ability to help, financial wellness programs are needed more than ever. While they’re considered supplemental offerings, there’s nothing supplemental about the positive influence they can have. The key is to offer a wide choice of subjects that reach a diverse employee base with varying financial acumen and different financial needs.

In choosing what programs to offer, it could be helpful to query employees on their topics of interest, which can improve engagement. Older employees, for example, may appreciate topics like how to take retirement income and understanding long-term health insurance, while younger workers are possibly more interested in deciphering credit scores, managing debt and budgeting. Saving for a child’s college costs and considering when to pick a financial advisor would likely spark wider interest.

On average, financial wellness program participants tend to skew white and male with higher incomes. This underscores the opportunity and need (i.e., lack of accessibility) among financially at-risk workers, who are mostly women, people of color and lower earners. These demographics tightly align with comfort and trust levels in the employers providing such programs, according to the Defined Contribution Institutional Investment Association. That is, the people who trust their employers the least are the ones who need financial wellness help the most. Based on this, financial wellness programs need to speak to a broader employee population, but also stay relevant to different and underserved segments within it.

Roadmap to Financial Wellness Starts at Solid Engagement

An employee’s interest in a topic and comfort with how the program is delivered—and who is offering it—can set the tone and engagement too. So, employers must appreciate even small nuances among their audiences.

Effective financial wellness programs identify and fill knowledge gaps across all employee segments. Knowing participants and what they want can really help, and workplace surveys are a good place to start.

Offering programs across different media helps drive engagement too, because not all employees like to learn the same way. For example, employees may be uncomfortable sharing their financial challenges, like reducing debt, openly in a group session, but they would more likely benefit from a virtual webinar watched in private or a one-on-one experience with a financial expert.

Over the many years we have surveyed plan participants, we’ve seen workers continue to struggle with financial wellness. Our findings this year are especially profound and shed even more light on those most affected and the topics most needed. But now it’s up to plan sponsors to take the next steps to build a higher level of financial savviness that workers can take all the way to retirement.

Jennifer DeLong is Managing Director, Head—Defined Contribution at AB.

Heather Balley is Director of Participant Communications—Defined Contribution at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.