In the aftermath of the Volkswagen scandal, the auto sector looks like a scary place to invest. But we think suppliers that can solve critical problems may come out ahead from the episode.

Few corporate scandals have been quite as shocking. In mid-September, Volkswagen was charged by the US environmental protection agency of using sophisticated software to cheat on emissions tests. VW’s brand was severely damaged and its shares dropped sharply. Shares of automakers and suppliers alike tumbled in the following days, amid concern that fraudulent behavior might be entrenched across the industry.

Seismic Changes in Auto Industry

But even before the VW earthquake, seismic changes were shaking the industry. Carmakers were struggling to meet stricter emission-reduction standards without undermining fuel efficiency. Efforts to improve the driver experience—from better technology to navigation and entertainment systems—demanded creativity and investment. And autonomous-driving technology was threatening to revolutionize road travel and leave laggards behind.

Auto suppliers are at the heart of all of these changes. Traditional car-part suppliers like Valeo in France or Magna International of Canada are racing to deliver an array of products that address the unfolding changes. Technology companies like Google and Apple smell an opportunity to play a big role in the driverless revolution. And relatively new players like Mobileye, which makes driver safety software, are in fierce competition for new and lucrative market niches.

Who Really Makes Your Car?

Against this backdrop, the relationship between suppliers and automakers is being redefined. In the past, automakers manufactured a large portion of each car. Today, while they still do some manufacturing, their role is really to design, assemble and market the product. Suppliers actually manufacture and part-assemble about 80% of a typical car.

This changing relationship is illustrated by efforts to solve the emissions challenge. Across the developed world, emission testing is getting tougher—and standards are likely to further tighten after the VW affair. Carmakers are desperate for more effective emission-reducing technology. Whether in the US, where the focus has been on nitrous oxide (NOx) emissions, or in Europe, where carbon dioxide (CO2) has been the priority, car manufacturers all need the same thing: a product that helps them pass the tests and cut emissions while minimizing fuel consumption.

For automakers, this challenge is a burden. They must spend lots of money to invest in solutions. It doesn’t add to the customer experience or increase earnings. And it creates a much more challenging investment case.

Suppliers can profit from cracking the conundrum. This makes sense. Instead of 30 carmakers trying to figure out the solution, a few suppliers are working on products that can be sold to 30 companies.

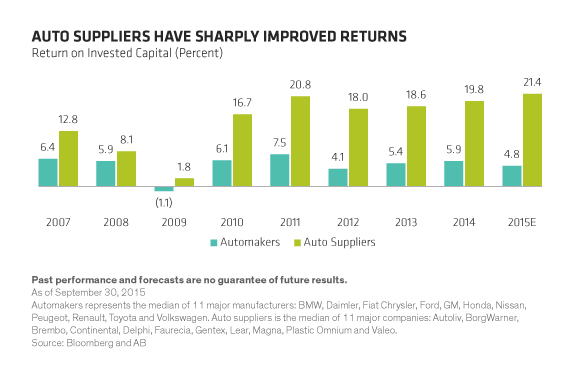

Suppliers Are Highly Profitable

Auto suppliers are already much better businesses than perceived. Many of these companies streamlined dramatically after the 2008 global financial crisis because they weren’t propped up by governments like the carmakers. There was a wave of mergers and acquisitions in Europe and the US, along with drastic cost cuts and consolidation of production.

Today, the supply base is brimming with technology. This gives suppliers more pricing power than in the past because their products are more sophisticated. Combined with industry restructuring and investment in new products, suppliers have improved returns on invested capital to levels well above those of the automakers (Display)—which adds resilience to downturns.

Barriers to entry are high. Since quality standards for car parts are very stringent, it’s not easy for an upstart with a sharp product to challenge an incumbent and win support from big auto manufacturers.

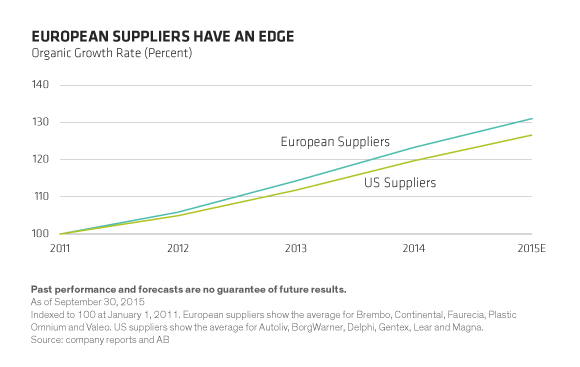

European suppliers may have a slight edge on their US peers, in our view. Shares of European suppliers trade at attractive valuations, while their balance sheets are generally strong. And their growth rates are slightly faster than US rivals (Display), even though auto demand in Europe has been slower than in other regions. Their advantage stems from their position as the dominant global companies developing products for the premium German car brands. Often, the cutting-edge technology starts at BMW, Mercedes and Audi and then filters down to the rest of the industry.

The Volkswagen debacle is still unfolding and sentiment toward the sector remains shaky. Yet we think the uncertainty makes it an excellent time for investors to hunt for companies that are positioned to thrive when the dust settles.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. AllianceBernstein Limited is authorized and regulated by the Financial Conduct Authority in the United Kingdom.