As bond yields rose in 2022, investors sought refuge in high-yield bank loans, whose floating coupons are often heralded as an antidote to rising rates. But with conditions shaping up differently in 2023, bank loans may face challenges. We think income-seeking investors should instead consider a more diversified approach that balances rate and credit risks. Here’s why.

Bank Loans Are Vulnerable When the Credit Cycle Turns

Floating-rate bank loans tend to do well when conditions are just right: the Federal Reserve is raising rates and the economy is growing. But such conditions typically don’t last long. In fact, we think the tide may soon turn: the banking crisis is tightening financial conditions, the Fed’s May rate hike may be its last, and US GDP growth is poised to slow in the second half of the year.

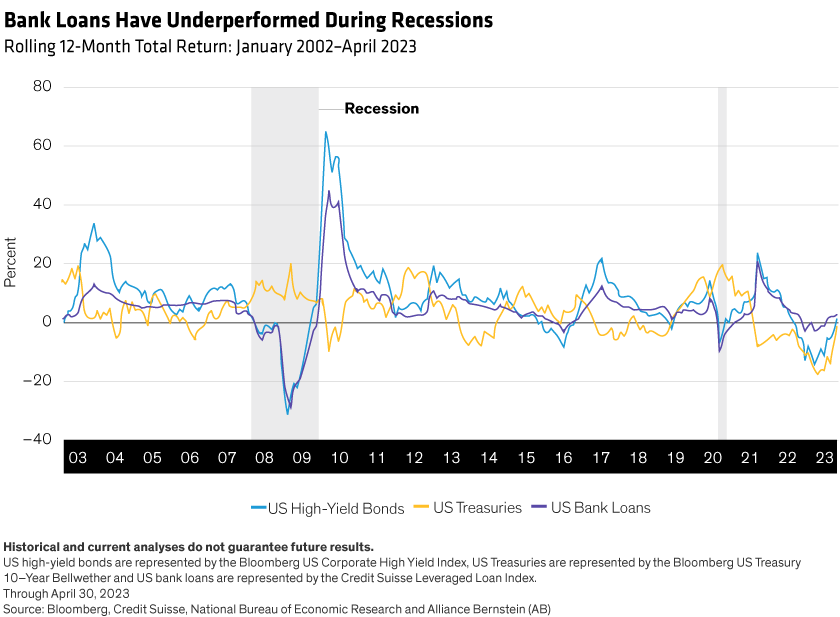

Exposure to bank loans at this late stage of the credit cycle is risky. Bank loans have historically underperformed during economic downturns (Display).

That’s partly because of the exaggerated cyclical effect of investors rushing into the market when rates begin to climb and rushing out when rates begin to fall. But it’s also because bank loans can carry meaningful credit risk. And that seems to be especially true today.

For one thing, as bank-loan coupons floated higher in 2022, the businesses that issued the bank loans saw their cost of capital ratcheting up, creating financial strain. In other words, the borrowing companies took on the interest-rate risk that investors sought to avoid.

Issuers should have at least partly hedged this interest-rate exposure with interest-rate swaps, but many did not. As a result, our analysis suggests that the average B3-rated bank-loan issuer is likely to experience negative free cash flow in 2023 because of underfunded floating-rate debt liabilities. According to S&P, roughly half of B-rated loans today are at risk of credit distress and downgrade.

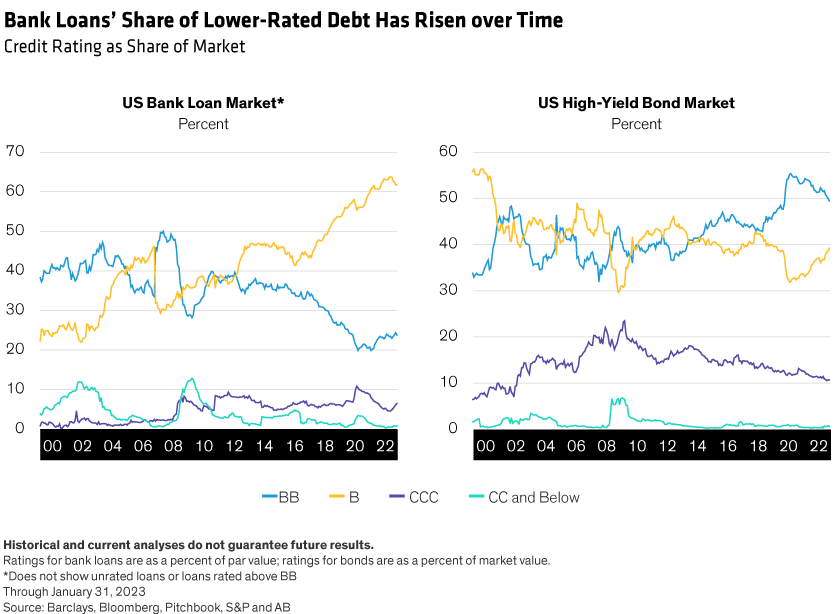

But that’s not all. Because bank loans tend to be a cheaper financing option for weak credits, the high-yield bank-loan market comprises more lower-rated debt than the high-yield bond market to begin with. Indeed, since 2009, bank-loan credit quality has deteriorated, while high-yield bond quality has improved (Display).

Thus, as the US economy heads into a low-growth phase, bank loans are at greater risk of default than high-yield bonds. Further, the share of the high-yield bond market that is secured—31% as of December 31, 2022—is relatively high, which may translate into higher recovery rates for high-yield bonds in the event of default.

Three Reasons to Strike a Better Balance

The way we see it, investors should consider ditching bank loans in favor of a balanced approach to income investing. Among the most effective active strategies are those that pair government bonds and other high-quality, interest-rate–sensitive assets with growth-oriented credit assets in a single, dynamically managed portfolio.

This barbell approach can help investors get a handle on the interplay between rate and credit risks and make better decisions about which way to lean at a given moment. The ability to rebalance negatively correlated assets helps generate income and potential return while limiting the scope of drawdowns when risk assets sell off.

In today’s environment, lifting a barbell strategy provides three key benefits:

1) Income generation. Yields across risk assets are higher today than they’ve been in years, giving income-seeking investors a long-awaited opportunity to fill their tanks. Investors should aim to diversify not only globally but also by sector. Sectors such as high-yield corporates, emerging-market debt and securitized assets—including commercial mortgage-backed securities and credit risk-transfer securities—can also serve as a buffer against inflation by providing a bigger current income stream. In our view, investors should favor higher-quality credit, be selective and pay attention to liquidity. Lower-rated credits in any sector are most vulnerable in an economic downturn.

2) Duration. While high-yield bank loans typically have little to no duration—a measure of sensitivity to changes in interest-rate levels—government bonds can be an excellent source of duration. And we think a moderate amount of duration from high-quality government debt could be an especially good thing in portfolios today. As inflation ebbs and the economy slows, duration tends to perform well, acting as an offset to the volatility of growth assets.

3) Negative correlations. In 2022, equity and fixed-income markets broke with convention and fell in tandem, leaving almost nowhere for investors to hide. Some market observers wondered whether the days of negative correlations between US Treasuries and risk assets were behind us. But recent market events have proved that thesis wrong. As risk assets sold off in March, US Treasuries enjoyed a strong rally, reestablishing the negative correlation between the asset classes in a risk-off environment. We expect this restored relationship to persist.

Take Care as the Cycle Turns

As the credit cycle enters its twilight stage, income-seeking investors should carefully weigh their options. In our view, a barbell strategy that balances rate and credit risks may succeed where bank loans will not. Above all, we think this is an ill-advised time to bank on bank loans. As the tide advances, investors may just find that floating-rate bank loans are castles in the sand.

AJ Rivers is Head—US Retail Fixed Income Business Development, and Matt Sheridan is Portfolio Manager—Income Strategies at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.