From Russia’s invasion of Ukraine to China’s COVID-19 crackdown, investors in emerging-market (EM) equities have faced many new challenges this year. Yet through it all, value stocks have held up relatively well as changing conditions revive dormant recovery potential.

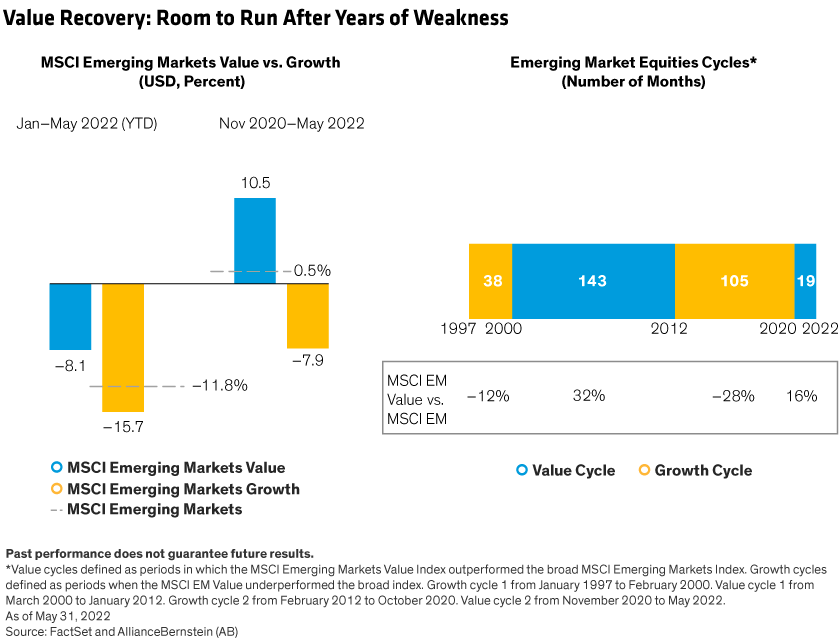

EM equities have tumbled this year amid the global sell-off. Developing-world stocks were hurt by the removal of Russia from EM indices, concerns about regulation and growth in China, global inflation fears, and rising risk aversion. The MSCI Emerging Markets Value Index has been more resilient, falling by 8.1% in US-dollar terms versus a 11.8% decline of the broader MSCI Emerging Markets Index and a 15.2% drop of the growth index (Display) this year through May 31. Despite these declines, EM value stocks have advanced by 10.5% since November 2020 through the end of May, outperforming both the broad market and growth benchmarks.

Is the Recovery Just Beginning?

It’s been a long time coming. Until November 2020, EM value stocks suffered nearly nine years of chronic underperformance, trailing the market by 28.1%. Throughout that period, extremely low interest rates encouraged investors to pay ever higher valuations for the fastest-growing companies, which fueled returns of EM growth stocks and portfolios.

But rewind further and the picture looks very different. Between 2000 and 2012, EM value stocks had outperformed the MSCI EM benchmark for 143 months. While past performance doesn’t guarantee future results, we believe that supportive macroeconomic and market conditions have potentially set the stage for a prolonged recovery.

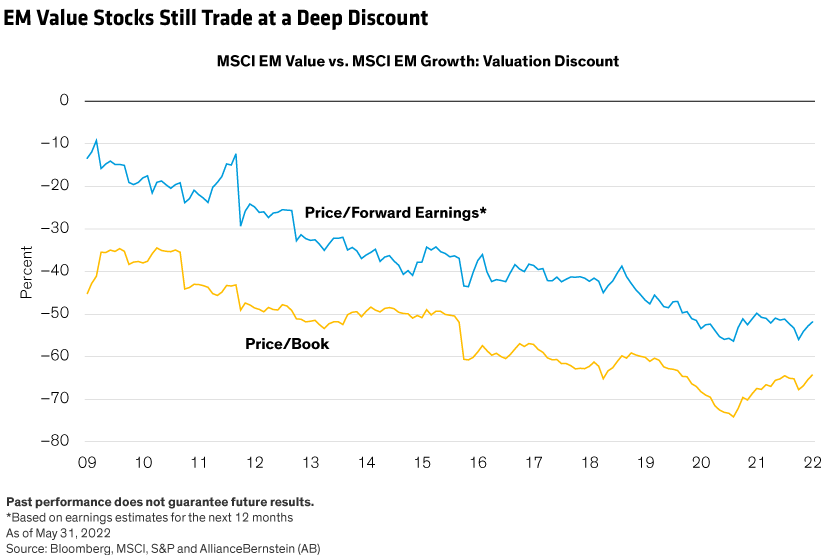

Current valuations are a good starting point. Even after the recent rebound in relative returns, EM value stocks trade at a near-record discount to growth stocks. Value companies have also delivered stronger earnings growth during this period. As a result, price/forward earnings multiples of value stocks are still very attractive (Display). EM stocks are also relatively cheap compared with their own history and other developed markets.

Rising Rates: A Recipe for Value Returns

Meanwhile, we expect macroeconomic conditions to spur the next stage of the recovery. Increasing inflation leads to higher interest rates, which in many cases leads to better business conditions and earnings for many of the companies held in value portfolios. Rising rates also push up the discount rate that investors use to price equities. A higher discount rate reduces the present value of future cash flows, putting downward pressure on valuations of higher-growth companies with cash flows further into the future. This dynamic is placing acute pressure on high-flying US growth stocks—particularly in the technology sector—and playing out similarly in EM equity markets.

Higher rates don’t compress value stock multiples as much because their cash flows tend to be nearer term. In other words, rising discount rates add hurdles for all stocks, but those with lower valuations and nearer-term cash flows should be advantaged.

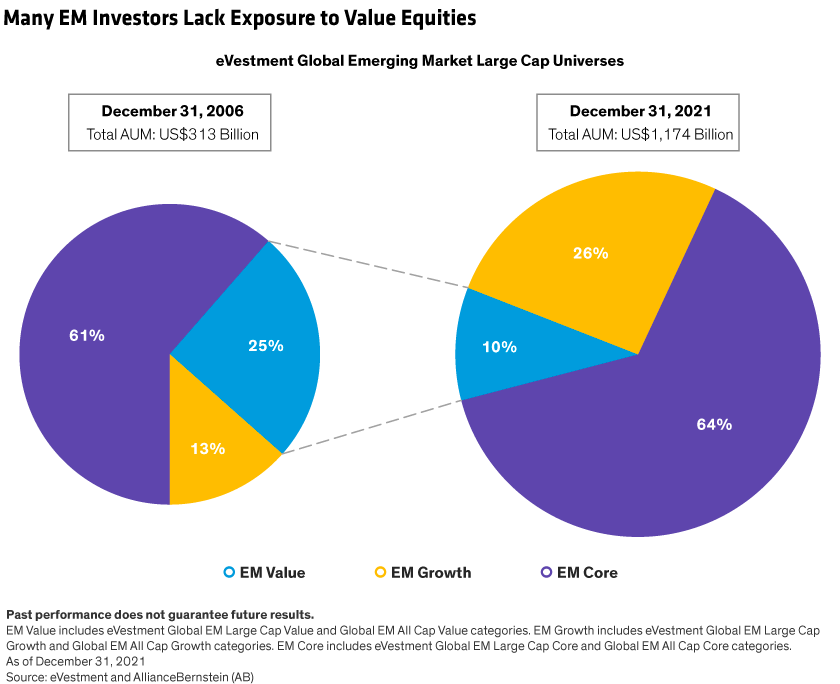

These dynamics are improving the outlook for EM value stocks, in our view. Yet many investors lack exposure to this segment of market, which has been out of favor since the global financial crisis in 2008. By the end of 2021, EM growth and core strategies dominated equity allocations, with value shrinking to just 10% of total global EM equity assets, according to eVestment (Display).

Growing awareness of the value recovery could spark a virtuous cycle. If more assets move back into value strategies, it would add another impetus for performance.

Diverse Companies with Catalysts for Recovery

To be sure, many investors are wary of emerging markets. Global volatility is stoking anxiety over EM equities, which are seen as a riskier asset class. Developing economies suffer from global macroeconomic stresses, while country-specific currency issues add another layer of vulnerability. It doesn’t help that pressure on global growth is emanating from two major EM countries today.

However, EM countries and companies are diverse. For example, South Korean automakers have impressive electric vehicle (EV) programs, which can help them take market share amid increasing demand for affordable green transportation. Copper producers—in countries such as India and Zambia—benefit from the shift to EVs, increasing electrification of economies and rising commodity prices. Financial firms in the Philippines and Vietnam enjoy a solid outlook driven by strong real economic growth.

Even some of the worst news coming out of EM can foster opportunities in stocks that have been unfairly punished. In eastern Europe, bank shares have been battered because of their proximity to the war, though some lenders have virtually no exposure to Russia or Ukraine and have solid loan books.

China’s growth concerns have created some opportunities. In our view, some real estate company valuations exaggerate the business risks and underestimate their recovery potential. And while predicting Chinese policy is difficult, the government’s net-zero commitment looks durable and has created select opportunities in utilities with renewable energy businesses. We believe that some Chinese auto company shares also look attractive, as their long-term earnings potential, which will partly be driven by substantial EV growth, is obscured by current COVID-19 policy restraints.

From Latin America to Asia, selective investors can find EM companies with unacknowledged business prospects that trade at a discount to developed-market peers. By identifying stocks with clear catalysts for a future rerating, EM equity portfolios can be positioned to withstand volatility and deliver long-term results. With a disciplined approach to valuation, investors can gain conviction to allocate or increase exposure to EM value stocks, with recovery potential powered by the same forces that are sowing uncertainty in markets today.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.