Emerging-market (EM) equities have been overlooked by many investors as a wave of macroeconomic and geopolitical threats have drawn attention to the risks. Yet these concerns may be obscuring potential improvements in economic and earnings growth that could provide good reasons to shift capital toward developing-world stocks.

Stocks in emerging markets have behaved surprisingly well this year. Even though they declined along with global equities, the MSCI Emerging Markets Index outperformed the MSCI World Index of developed-market (DM) stocks in the first half of 2022. EM stocks fell by 17.6% in US-dollar terms, while the S&P 500 and the MSCI World Index declined by 20.2% and 20.5% respectively.

Uncertainty and volatility aren’t going away. Yet we believe EM stocks are well-placed to continue outperforming their DM counterparts and reverse a long pattern of underperformance for three main reasons:

1. Improving Economic Growth Should Support Business Fundamentals

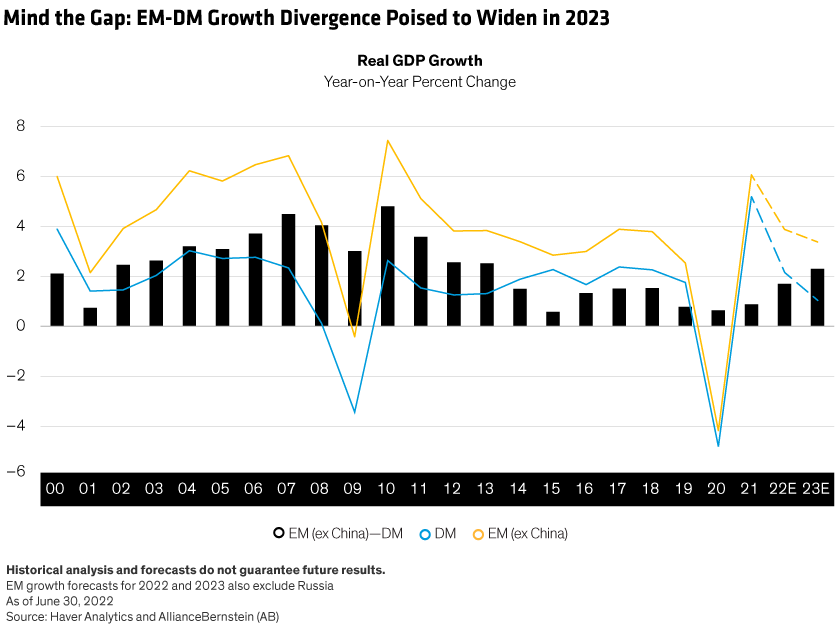

In DM countries, the prospects of recession loom large, as persistent inflation has put pressure on demand. But many EM economies are still recovering from the COVID-19 pandemic, particularly in Asia where domestic activity is improving. The boost from reopening economies will outweigh the drag from tighter financial conditions and, in our view, should help widen the growth gap between EM and DM economies next year (Display).

China is a prime example. After months of severe lockdowns, the likely reduction in COVID-related restrictions, along with economic stimulus programs, should help boost growth in the second half of the year. This, in turn, will increase corporate profits, in our view.

China is also on a different monetary and fiscal policy trajectory that should add to its recovery potential. Many developed and emerging countries have embarked on tighter monetary policies to combat inflation. Yet we believe that China, with lower inflation, has room to ease monetary conditions.

EM countries are well positioned to grow over the medium to longer term, in our view. Many should benefit from having avoided ultra-easy monetary policies over the past decade. Debt levels are generally lower, population growth is more robust than in most developed countries and productivity continues to improve, adding to the favorable fundamental backdrop for EM companies.

2. Inflationary Forces May Be Less Persistent

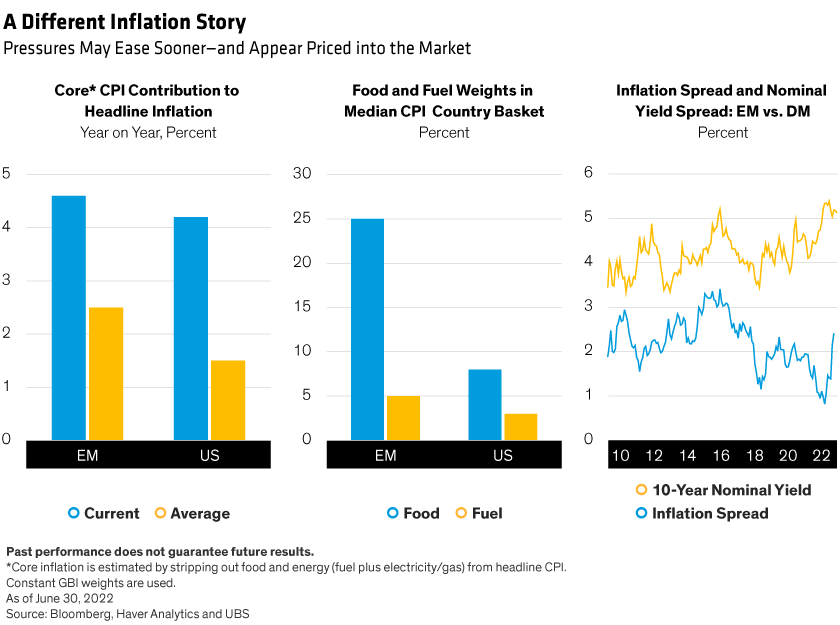

High global inflation is having different effects in different regions. EM countries may be better protected from some of the impact of commodity shocks, supply-chain disruptions and the post-COVID demand recovery.

That might sound counterintuitive. But in developed markets, the inflation problem seems more acute and more likely long lasting. For example, US core inflation—excluding food and energy—is contributing three times more to headline inflation than its historical average as a result of aggressive fiscal and monetary responses to the pandemic. In contrast, core CPI is only 1.8 times the historical average in EM (Display). That’s because in EM countries, food and energy contribute more to inflation, given its large weights in the CPI basket. This also means that when food and commodity prices stabilize and decline, EM inflation rates should come down faster than in DM countries.

What’s more, EM central banks have been more proactive in raising interest rates compared to their developed-market peers. And EM central banks generally didn’t implement quantitative easing during the pandemic, which should help keep inflation expectations from becoming entrenched.

Meanwhile, whereas the inflation spread between emerging and developed markets is in line with historical levels, EM offers one of the highest yield differentials to DM over the last decade. This suggests that markets have already priced in expectations that inflation will be less persistent in EM countries to a greater degree than in previous cycles.

Of course, there are real risks to consider. Food-price inflation threatens to fuel social unrest in some smaller EM countries. The war in Ukraine is grinding on. China-US tensions remain, though discussions are underway to resolve issues related to Chinese securities listed in US markets. And some countries such as Turkey and Argentina do face significant challenges.

But on balance, most large emerging countries are in a relatively strong position to face any upcoming challenges over the coming months, given solid fundamentals. External funding needs are lower, forex reserves are stronger, EM exchange rates are competitive and rate hikes by EM central banks drove up nominal and real interest-rate differentials with the US. As such, EM real yields are now mostly positive.

Positive real interest rates (bond yields minus the rate of inflation) in several emerging countries combined with faster economic growth should, over time, help attract investment flows to emerging markets, where investors have been under-allocated to equities in recent years.

3. EM Valuations Are Attractive and Corporate Earnings Should Improve

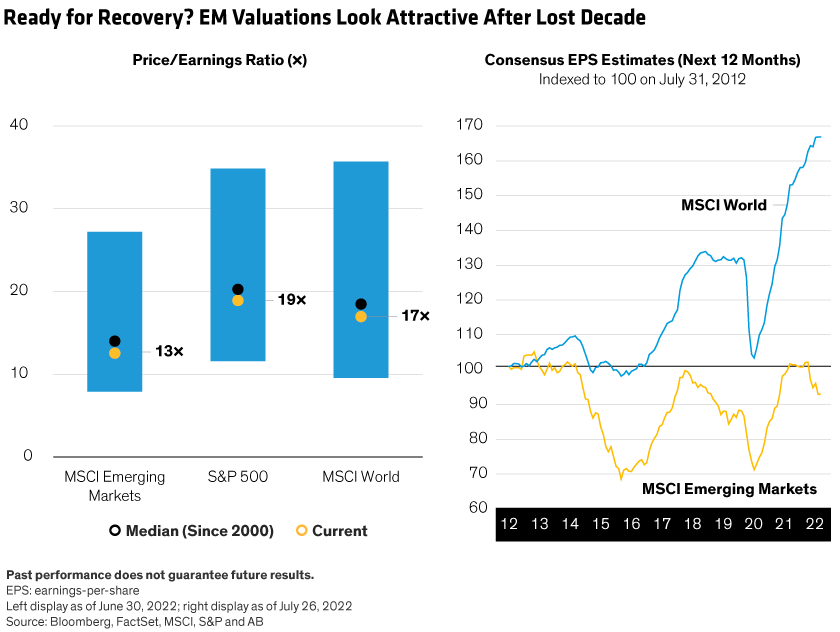

Following a lost decade, EM equity valuations are now very attractive compared to developed markets (Display). Further improvements in investor sentiment could pave the way for a recovery, especially if earnings improve.

The EM corporate earnings cycle is markedly different to the US and other developed countries. US equity markets benefited from stronger earnings growth over the past decade, but profits are widely expected to be challenged if the economy slows and as inflation weighs on margins. In contrast, many EM companies have not yet reached their profit potential, in sectors including domestic cyclicals and banking. We expect accelerating top-line revenue to foster an expansion of profit margins in EM countries, while in DM regions, profitability levels are already high.

Capturing this return potential requires a selective approach and rigorous risk management. By identifying companies with solid fundamentals and resilient business models, investors can find stocks across sectors that are well positioned to deliver long-term results through a challenging environment. And with a disciplined approach to stock selection, portfolios can be created that give investors confidence to increase exposure to EM equities—even in a very volatile world.

Sergey Davalchenko is Chief Investment Officer—Emerging Markets Growth Equities and Sammy Suzuki is Co-Chief Investment Officer—Strategic Core Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.