Global equities surged in 2021 during a year full of surprises. As the new year begins, perhaps the only sure thing is that there will be more surprises to come in 2022. So how can investors prepare for unexpected developments driven by macroeconomic forces, the pandemic and geopolitical risk?

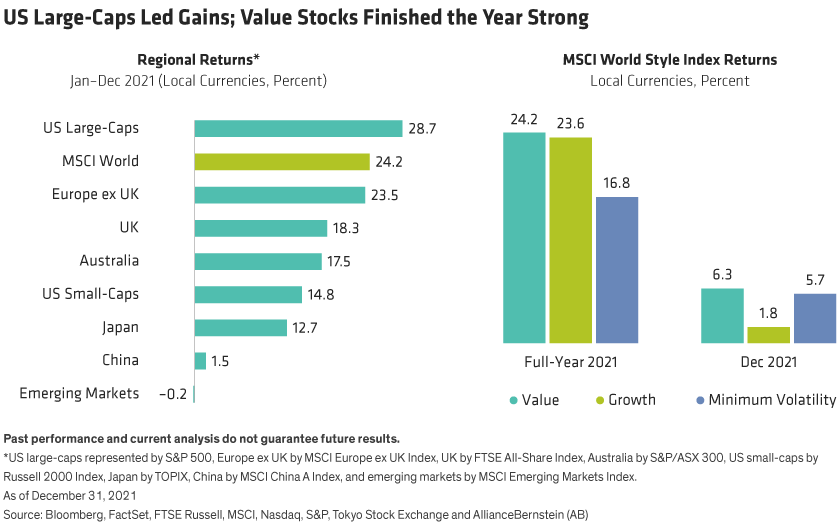

Despite bouts of volatility, the MSCI World Index advanced by 24.2% in 2021, in local currency terms. US large-caps (Display below, left) led the gains and weren’t derailed in late December after the Federal Reserve unveiled plans to accelerate monetary policy tightening in 2022. Developed markets outperformed emerging markets, as Chinese stocks struggled. Energy, technology and financial stocks outperformed, while defensive sectors such as utilities lagged.

Style returns flipped repeatedly. Value stocks rallied through May, but growth stocks regained leadership until December. As a result, global value and growth stocks delivered similar full-year returns (Display above, right). In the US, however, small-cap value stocks outperformed smaller-cap growth stocks by a wide margin. The MSCI World Minimum Volatility Index underperformed as investors shunned defensive stocks.

Many Predictions Missed the Mark in 2021

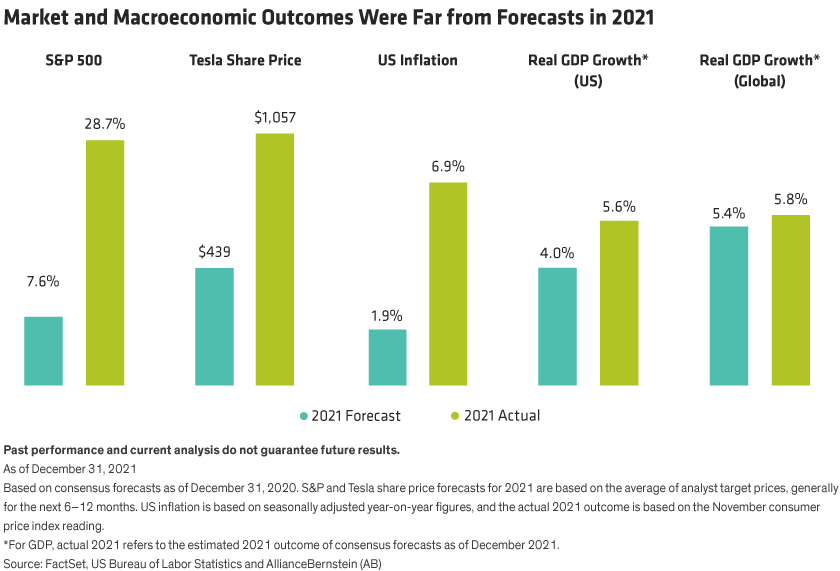

At the start of 2021, few predicted that US stocks would post another year of resounding gains, or that Tesla shares would soar to join the ranks of the megacaps. Supply-chain bottlenecks that fueled inflationary pressures were unexpected. Hopes that vaccines would quash COVID-19 were premature, with the recent surge of the Omicron variant pushing the world into a third pandemic year. Consensus forecasts were far off macroeconomic and market outcomes (Display).

Perhaps the extreme divergence of forecasts from reality reflects the times we live in. No living investor has experienced a global pandemic or the extraordinary monetary and fiscal policies that have been deployed to keep economies afloat. Without a playbook in hand, investors should beware of assuming that trends in recent years will repeat in the future. For long-term investors, we believe it’s much more effective to focus on the business forces that drive individual stocks and to assess how they could be affected by macroeconomic developments, rather than fickle market forecasts.

Earnings Gains and Economic Distortions

So why did stocks do so well in 2021? The simple answer is because earnings were even stronger than expected across the board as the world emerged from the lockdowns and deep recession induced by COVID-19 in 2020. This was good news for investors, because robust earnings provide fundamental support for valuations.

But don’t be dazzled by last year’s earnings. In some cases, unusually strong profits reflect economic distortions created by extreme policy responses during the 2020 recession. For example, in parts of the retail sector, supply-chain constraints have meant fewer discounts for consumers and higher profits than normal; recent earnings may be unsustainably high over the long term, when conditions normalize. For credit-sensitive companies, investors must ask: What will be a normal level of earnings in more normal credit conditions, when consumers aren’t paying down debts with cheap money? Prices for raw materials and key inputs like semiconductors should fall as supply constraints ease, reducing profits for producers.

Perspectives on Inflation and Monetary Policy

For many companies, inflation looms large. US consumer prices surged by a seasonally adjusted, year-on-year rate of 6.9% in November, a pace not seen for four decades. Inflation is soaring in many other developed countries.

But rising inflation isn’t necessarily bad for stocks. Moderate inflation fueled by a rebound in demand is usually a sign of a healthy economic recovery. And we don’t expect inflation to stay stuck at the especially high levels seen in late 2021. While wage-driven inflation could be sticky, some price pressures are likely to ease as supply chains are unclogged. Our research shows that over the past 50 years, stocks have done well during periods of moderate inflation between 2% and 4% (Display). In inflationary environments above 4%, US stocks have historically underperformed other regions.

The inflation conundrum will shape central bank policies. Stocks may suffer if sticky inflation provokes a more aggressive monetary policy response than expected. But markets are already gradually adjusting to the prospect of rising rates in the US. There was no taper tantrum in December when US Fed Chairman Jerome Powell announced plans for an accelerated reduction of asset purchases and three rate hikes in 2022. And the policy outlook differs by region. The Bank of England has already started raising interest rates, while the European Central Bank is moving much more gradually and has signaled it will refrain from raising rates amid less severe inflation pressures.

As fundamental stockpickers, it’s not our job to predict monetary policy. Yet we do need to understand how different types of companies, business models and stocks may be affected by changes.

What Could Go Wrong?

Market bears point to several ominous forces. If high inflation endures, central banks are likely to tighten monetary policy sooner than had been expected just a couple of months ago—just as GDP growth is slowing from the initial sharp rebound after the 2020 pandemic-induced recession. Efforts to contain COVID-19 have been jeopardized by the rapid spread of Omicron, which could slow the release of pent-up consumer and business spending to support the next stage of the recovery. Geopolitical friction, from potential Russia-Ukraine hostilities to Iran’s nuclear program and tensions between China and Taiwan, could flare up and sour market sentiment.

These are all real risks, but we think a bear market is unlikely in 2022. Historically, a peak-to-trough decline of at least 20% happens when economies are in recession. Even if inflation reduces the rate of real economic growth, the world economy is on course to keep expanding during 2022. AB economists forecast real global GDP growth at 5.9% for 2021, slowing to 4.2% in 2022. That should provide sturdy support for company earnings, in our view.

Valuations and Concentration Risk

Still, the rapidly changing dynamics of growth, inflation and interest rates could affect returns for different types of stocks.

Rising rates push up the discount rate used by investors to evaluate company cash flows. This often leads to multiple compression, particularly for higher-growth stocks, whose cash flows are further out in the future. As a result, the relative performance of different styles will be affected by inflation and monetary policy trends. Higher inflation and faster rate hikes will probably benefit value stocks, while easing inflation and more moderate hikes could favor growth stocks. This pattern was evident during most of 2021.

Either way, we believe the dominance of the largest US growth stocks could be challenged. In 2021, five megacap stocks outperformed again. As a result, US markets—and particularly the growth index—remain heavily concentrated in the largest names (Display). While each company has its merits, significant exposure to the entire cohort could leave investors vulnerable if sentiment turns. Instead, we believe companies with strong profitability and earnings, trading at relatively attractive valuations, offer more resilient return potential, particularly if rising rates compress valuations dramatically at the more expensive end of the market.

Outside the US, valuations are diverse (Display). European and Japanese stocks trade at relatively attractive valuations and offer exposure to a greater proportion of cyclical stocks, which may perform well if the regional economic recovery picks up. Companies in Europe also have record amounts of cash and may embrace buybacks more broadly to reward shareholders, in our view.

In emerging markets, Chinese stocks were hit in 2021 by a wave of regulation, debt troubles in the property sector and growth concerns. Yet policymakers continue to seek a balance between supporting near-term growth and pressing ahead with structural reforms underpinning the common prosperity initiative, which could add a recovery catalyst for select shares. Stocks in other emerging and frontier markets countries did well last year and attractive long-term opportunities can still be found across the developing world.

As the new year begins, we believe investors should check their allocations. Given the uncertainties, we believe a balance of exposures to different regions and styles, with a focus on high-quality stocks and reasonable valuations, will underpin a successful strategy in 2022. For all equity portfolios, integrating analysis of environmental, social and governance issues in fundamental research will play an increasingly vital role in developing investment insights to drive returns.

Strategic Antidotes to the Element of Surprise

Big data tools can also provide advantages. For example, our data science team has developed a tool to identify supply-chain hot spots in real time. We’ve also deployed an application to alert when a stock is getting hot on Reddit, so portfolio teams can prepare for potential speculative activity.

One principle can guide investors through uncertain times: develop insight into what a company’s normal earnings trajectory will look like after temporary effects fade. By forecasting how businesses and cash flows will evolve over three to five years, investors can gain conviction in a stock’s ability to deliver on return expectations when faced with macroeconomic or market curve balls. Sticking to a disciplined process—based on company fundamentals—is the best strategic antidote to short-term surprises.

Chris Hogbin is Head of Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.