Global equities rose through most of the third quarter but gave up most of their gains in a volatile September. As the forces driving stock returns rapidly change in our COVID-scarred world, we believe active managers can help investors effectively navigate the recovery’s uncertainties ahead.

The MSCI World Index was up by 0.6% in local currency terms in the third quarter, taking the year-to-date return to 14.9%. But investors’ concerns crystallized as stocks fell by 3.7% in September. With central bank policy plans and rising inflation at the center of macroeconomic unease, 10-year US Treasury yields moved up in September and hovered near the 1.5% mark at quarter end. Earlier in the quarter, regulatory action in China and the Evergrande crisis sent shockwaves around the world. In developed equity markets, style leadership shifted from value stocks toward growth through August, then back to value toward quarter end. While the global growth recovery continued, the coronavirus delta variant muddied the world’s escape route from the pandemic.

With so much in flux, how can investors position equity portfolios? We believe the key is to target companies with business models that can rise above uncertainty and to avoid those that are more exposed to the risks. While this principle is always essential, we believe the advantages of disciplined selectivity are even more pronounced as market currents shift.

Return Patterns Shift in 3Q

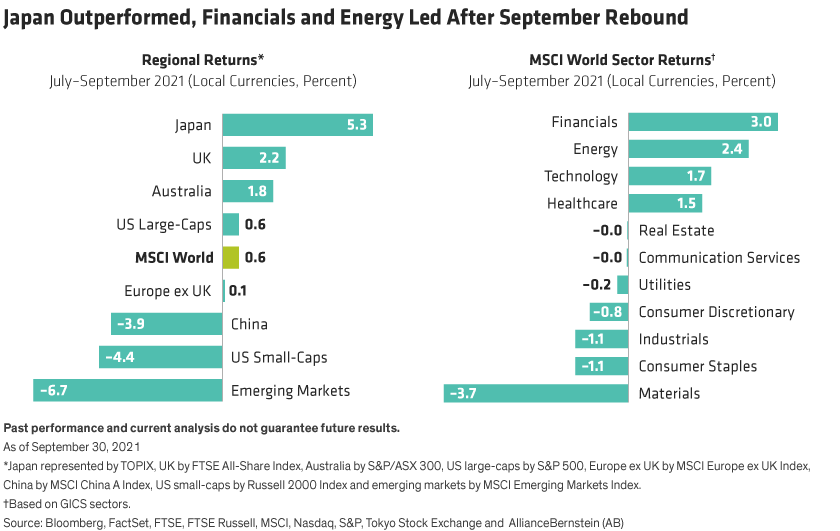

Japanese stocks led developed markets during the quarter, advancing by 5.3% in local currency terms (Display, left). US large caps ended the quarter up just 0.6% after falling 4.7% in September, their first monthly decline since January and their worst month since March 2020. Emerging-market equities fell by 6.7% amid declines in China.

Financials and energy led sector gains after rebounding late in the quarter (Display above, right). Technology stocks, which did well through most of the quarter, weakened in September. Style returns in developed markets shifted from growth dominance earlier in the quarter back toward value (Display below, left). However, value outperformed in emerging markets, where equities fell.

Monetary Policy and Inflation

September wobbles reflect, in part, unease about the changing monetary policy landscape. Central banks in South Korea, Hungary and Norway moved official rates up from historic lows, the first tangible signs of the changing monetary policy environment. The European Central Bank is preparing to retire its Pandemic Emergency Purchase Programme, while the Fed said it is likely to begin tapering asset purchases in November and signaled that rates may rise next year.

Yet, there has been no full-blown taper tantrum so far. While there have been some tough trading days, investors appear to be adjusting in fits and starts to the reality of the imminent end to extraordinary monetary policies that have prevailed through the pandemic.

Inflation, however, is a real threat, especially as the supply-chain squeeze pushes prices up in many industries. In Europe, inflation reached 3% in August, well above the European Central Bank’s 2% target. The Bank of England predicted UK inflation could breach 4% into the second quarter of 2022, while in the US, the Fed updated its 2021 inflation outlook to 4%. Companies around the world are taking note and talking about inflation more than they have in years on earnings calls.

Macroeconomic and policy trends matter, and they do drive stock prices and return patterns. For example, higher-growth stocks are generally more vulnerable to rising interest rates than lower-growth or value stocks. But we believe that predicting near-term macro trends, which have little bearing on longer-term company earnings, isn’t a prudent investing approach. Instead, we think investors should insulate portfolios against macro risks rather than taking a directional point of view. Active management can help by finding companies that are poised to thrive no matter what happens with policy, rates or inflation.

To be sure, if inflation stays over 4% for a long time, our research suggests that equity returns will suffer. However, in our view, investors shouldn’t avoid equities because of inflation, whether it turns out to be transitory or longer lasting. Either way, the inflation lens should now be applied systematically to company research. Companies that command real pricing power are likely to do much better in an inflationary environment than competitors who do not. Other companies might be hurt by rising prices of raw materials. Still others, such as commodity producers, real estate firms and banks, tend to benefit from inflation. Active managers can help ensure that equity holdings are prepared for the complexities created in an inflationary world.

China’s Twin Challenges: Is It Safe to Invest?

Risks emanating from China must also be proactively managed. Recent developments in China have rattled investor confidence in the world’s second-largest economy. In July, Chinese stocks tumbled amid a regulatory crackdown on education and technology companies. Then, in September, debt troubles at giant property developer Evergrande sparked concerns about the stability of the sector and China’s financial system.

Concerns about contagion from Evergrande are understandable. However, while a default would be painful for bondholders and will likely stoke volatility, we believe China’s banking system can probably withstand the pressure. Although the government is unlikely to rescue Evergrande, we expect it will take steps to prevent a collapse of the property sector. And over the medium to long term, cleaning up unsustainable businesses such as Evergrande is good for the financial health of the system, especially if a measure of risk-pricing discipline can be introduced in the process. This should lead to more transparency for stock pickers.

China’s regulatory moves during the summer also require context. Regulatory surprises in China are not new. Since China has grown so fast in recent decades, regulators often introduce changes to catch up with new industries that developed at lightning speed.

While regulatory action is unpredictable—even in developed countries—selective investors can identify companies that are less likely to be in the crosshairs of watchdogs, particularly in more mature Chinese industries such as consumer staples, industrials or materials. For attractive companies that are more vulnerable to regulation, investors can apply higher risk premiums to fundamental analysis and buy them at an appropriate price. And as the Chinese government pursues its common prosperity policy as well as policies to reduce carbon emissions, new regulation will also have a positive impact on some industries and companies, creating opportunities for investors.

Perspectives on Valuations and Concentration Risk

China might seem like a world away from developed markets, but there are parallels. Many concerns about the power of technology and consumer giants in China are shared by US regulators. During the recent sell-off in China, some of the largest names were hardest hit, perhaps providing a cautionary tale for some of the popular US mega-cap companies.

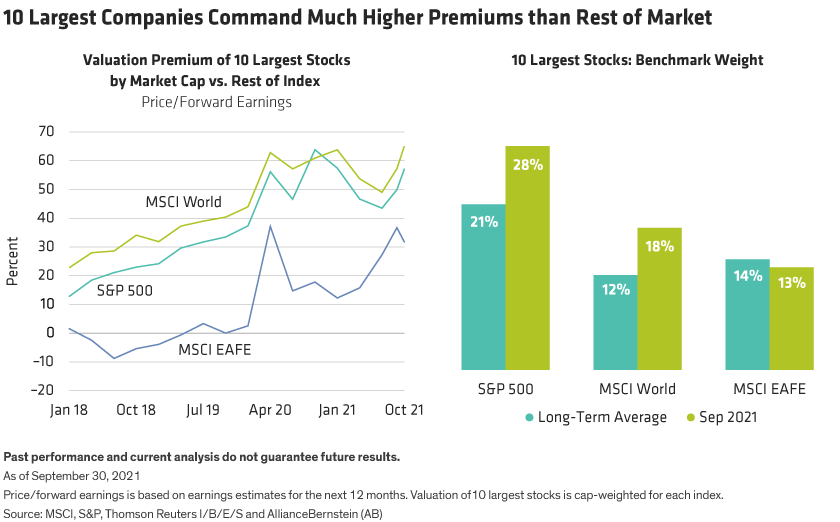

In the US, the retreat of high-growth mega-cap companies during September warrants a closer look at the risks of market concentration. By quarter end, the five largest companies—Apple, Microsoft, Amazon.com, Alphabet Inc. (Google) and Facebook—made up 22% of the S&P 500 Index and 37% of the Russell 1000 Growth Index. In the US, the 10 largest companies are now 57% more expensive than the rest of the S&P 500 companies, and the valuation premium has doubled since early 2019. For the MSCI World, the top-10 premium is 65% (Display, left).

Outside the US, the 10 largest stocks in the MSCI EAFE Index are less expensive and not as heavily weighted in the index. But market concentration in the US is extreme (Display above, right), so investors buying a passive index of global or US stocks will have a disproportionate weighting in the priciest names. While US mega-caps offer compelling growth stories, we believe each company should be researched and held based on a disciplined investing approach in diversified portfolios at measured weights. Allocating heavily to a small group of very large stocks could leave portfolios exposed if sentiment toward the mega-caps sours further, as we saw in China during the summer.

Active investors can position with these risks in mind. Portfolios can target sectors and companies with reasonable valuations and strong growth or recovery potential. Regional exposures can be calibrated to account for diverse valuations. Company research can be used to develop insight not only on business potential but also on capital management, for example, to identify companies that are likely to unlock value for investors via share buybacks and dividends. Integrating environmental, social and governance (ESG) issues into company research can yield insight on companies that are changing their behavior to benefit a broad group of stakeholders and to support sustainable growth.

Sourcing Sustainable Return Potential

Are equity market gains sustainable? After a strong run through the first three quarters of 2021, the risk of a correction should not be ignored. But compared with bonds, we believe stocks still offer attractive long-term return potential that can’t be sourced elsewhere and should prevail over time, even if a short-term downturn materializes.

Stocks and markets are not monolithic. Investors can deploy many strategies to tap the breadth of equity market potential today, from defensive companies to quality attributes that can provide advantages in growth and value-oriented portfolios alike. By using a full set of research tools, investors can develop conviction in the ability of a company to control its destiny over the long term, relying on investment insights that are resistant to macroeconomic and policy winds.

Chris Hogbin is Head of Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.