Rising inflation is troubling bond investors worldwide, but European bond markets will likely experience comparatively weaker inflation pressures and stronger central bank support. Even so, investors in euro markets will need to stay alert and active as 2022 unfolds.

Global economic dislocations and inflation pressures are set to continue into 2022, making for tighter monetary conditions. In the US, where prices have risen at the fastest rate since the 1990s, the US Federal Reserve is accelerating tapering its bond-buying program and will likely begin hiking rates in March and will continue through 2023.

In contrast, euro-area inflation should remain more subdued than the US, with no rate hikes likely by the ECB before 2023. This would leave euro-area bond markets in 2022 with ultra-low rates but probably also low volatility. We expect a mostly supportive background for investors in euro fixed income, with some notable opportunities but also some potential threats.

Europe Leads in Sustainable Investing

Responsible investing continues to grow in importance. In 2022, we will likely see even greater investor interest in environmental, social and governance (ESG) factors and a further increase in issuance of green and other sustainability-linked bonds.

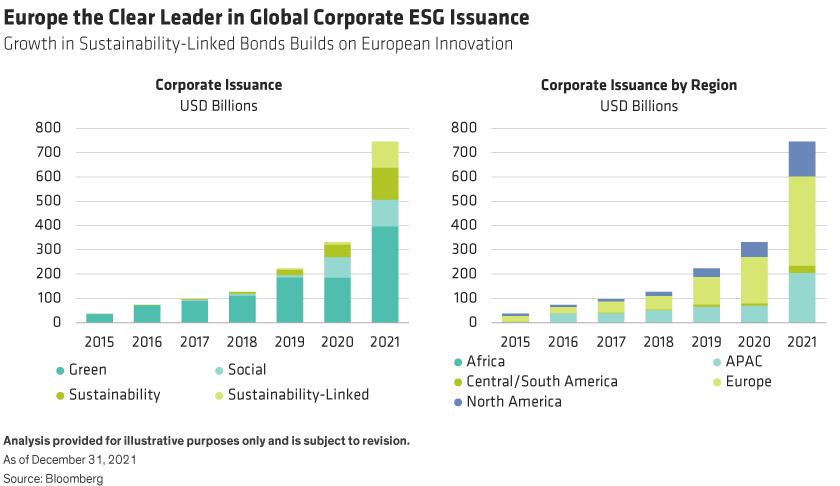

Europe has been and remains the global leader in this area (Display, below), in terms of both innovation and volume. In fact, 44% of new issuance in Europe for November 2021 was in ESG structures. We expect this dynamism will attract more capital into European fixed-income markets in 2022. That in turn will likely compress spreads in the European ESG-linked bond markets.

Cost of Hedging May Keep European Investors at Home

With US and European interest-rate cycles set to diverge further, US dollar-denominated bond yields may look tempting relative to similar euro-denominated bonds. But investors should consider currency risk. The cost of hedging US dollar-denominated bonds back into euros fluctuates over time (Display, below). Although hedging costs currently sit at the lower end of the recent range—about 0.8%—they will increase as US rates rise.

A sharp increase in hedging costs would make US bonds relatively less attractive for European investors during 2022 and so tend to keep them invested in their home markets. Conversely, euro markets may offer attractive opportunities for US dollar investors on a currency-hedged basis, as negative hedging costs could compensate them for lower euro yields.

ECB Support for Bond Markets Still High

Whereas high US inflation will keep pressure on the Fed to accelerate their taper, conditions in Europe should stay favorable for bond investors. The ECB has a range of programs in place to support the euro-area bond markets and banking system. And the bank’s commitment to maintain accommodative monetary conditions remains strong. In a keynote speech in November, ECB president Christine Lagarde repeatedly stressed the importance of persistence in monetary policy and the dangers to the euro-area economy from premature tightening.

Although the bank is set to halt (but not end) its Pandemic Emergency Purchase Programme in March, it is using the similar Asset Purchase Programme to step up bond-buying as needed. Crucially, the size of the ECB’s corporate purchases remains substantial relative to the size of euro corporate bond markets and is much larger than the equivalent Fed program.

Meanwhile, the ECB’s scheme to provide cheap money to the banking system and to stimulate loans to the euro-area economy through targeted longer-term refinancing operations has been extended through June 2022 and will likely be renewed thereafter. After all, the continuation of these support programs is vital not just for European economic recovery but for the European integration project too.

Corporate Credit Is Well Supported

As European economies have started to recover from the COVID-19 pandemic, corporate earnings and cash flows are rebounding. Fundamentals are improving for European issuers across a range of metrics—notably, net leverage, interest cover and profit margins. This trend strengthens corporate balance sheets and increases issuers’ resilience. Default rates have fallen sharply since February, and we believe they will continue to trend down.

The availability of ample cheap credit may, though, have a downside for bondholders. We think leveraged buy-out activity will be very strong in 2022 and that, with capital so readily available, bidders will be able to raise previously unthinkable amounts of debt. The recent €10.8 billion offer by KKR for Telecom Italia—and the rumored bid for BT—will likely presage more mega-deals in 2022. Typically, a successful takeover bid for a stable, well-regarded business by a highly leveraged raider can transform the credit rating of the target company’s bonds from a solid BB to a much riskier low single B or CCC—with a commensurate fall in price for the bondholders.

Of course, corporate mega-deals will not be unique to Europe. But after the featherbed of years of ultra-low interest rates, many big-name European corporates may be particularly vulnerable to takeover bids aimed at modernization and restructuring. Bond investors will need to stay alert in 2022.

Politics and Populism May Threaten the Status Quo

Elections open the way to change. After a long period of relative calm, 2022 will feature potentially significant polls across a range of European countries. These include presidential elections in France and Austria. After a decade of low economic growth and beset by COVID-19-related problems, incumbents may face difficult contests this time round.

Populist challengers—intent on radical new policies that would shake up the European political and economic consensus—may command unusually high support. Their success could in turn weaken the solidarity of the European Union (EU) member states and undermine support for the ECB’s policy stance.

Regime change in France could lead to a sharp setback for holders of French and European periphery sovereign debt. This development could be particularly problematic given current ultra-low yields and high levels of indebtedness. We think an active, dynamically managed approach will be important throughout 2022—particularly ahead of the key poll dates, when investor anxiety will likely ratchet up.

Balanced Portfolio Construction Improves Risk-Adjusted Returns

The new year promises a better background for world economies and companies as COVID-19 dangers and constraints gradually fade. Even so, markets will still face several risks including continuing geopolitical tensions and populist pressures. In this environment, investors will need good risk management.

A balanced portfolio that dynamically manages interest-rate and credit risk can improve risk-adjusted returns. This approach combines sovereign and other higher-rated debt with non-investment-grade credits in a single, risk-managed portfolio. Such a portfolio captures the majority of potential return provided by high-yield markets, but with much smaller drawdowns than a dedicated high-yield portfolio. It can also ensure liquidity in times of market stress. This means that investors can readily rebalance back from safer investment-grade securities into high-yield credits when attractive entry points arise.

In 2022, skilled country and individual credit selection will continue to be critical in Europe’s complex credit markets. With disparate rates of recovery across sectors and across the region, European fixed-income markets offer good prospects for active investors. A dynamic approach will remain key, as volatility-driven gains and setbacks can reverse quickly. And the ability to invest tactically may add considerable value in markets that stand out from global trends.

Vivek Bommi is Head of UK and European Fixed Income at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.