In a changing world, multi-asset strategies need to evolve, especially when building inflation resilience, because tomorrow’s price pressures will likely look very different from today’s. Not only must inflation defenses be diversified, they should also be innovative.

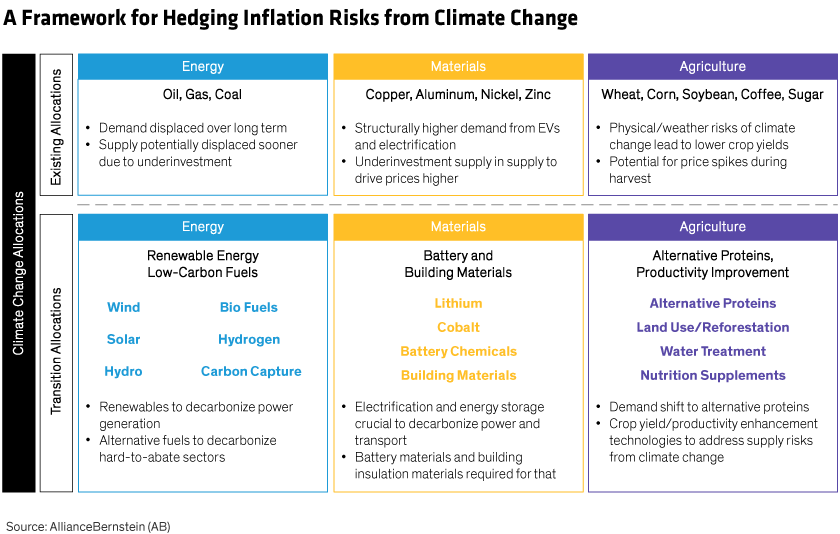

Classic inflation hedges—such as TIPS, commodities, natural resources and real estate—still play vital roles in inflation-protection strategies. But as the world evolves, so will the exposures needed to build an effective solution. We think the global transition to a low-carbon economy is likely to be inflationary, driven by a combination of increased spending on low-carbon capacity solutions and the risk that investment in existing sources of energy and materials declines too soon.

Eventually, the adoption of low-carbon solutions will reach equilibrium and prices will steady, but it could take years. In the meantime, multi-asset inflation strategies can benefit from these trends by incorporating stocks of businesses directly involved in solving for climate change—also known as future-resources stocks. Specifically, adding exposure to firms involved in the long value chains of wind and solar energy, battery materials, energy storage and agricultural productivity can bolster inflation resilience in a broader diversified strategy (Display).

Not All Future Resources Boost Inflation Resilience

Investing in future-resources equities requires balancing forward-looking optimism with pragmatism.

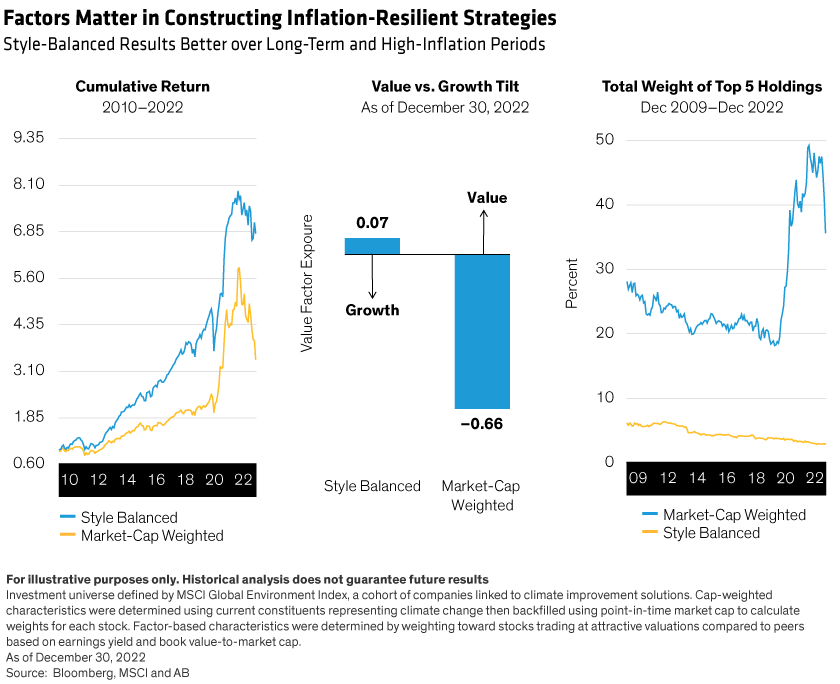

Deploying these stocks as part of an inflation-protection allocation within a multi-asset strategy makes sense for the long run. However, these firms tend to have a growth flavor and may come under pressure when inflation spikes and bond yields rise. In these conditions, particularly in 2022, passive approaches with a growth tilt and heavy concentration in a few names underperformed—generally not a good outcome when inflation bites.

On the other hand, the value style tends to do well in such environments and over longer periods. We can see this by comparing the returns of two strategies, both with the same collection of future-resources companies. One strategy weights holdings based on simple market capitalization; the other used a style-balanced approach, favoring stocks trading at attractive valuations versus industry peers based on current earnings and cash flow as well as longer-term factors like book value to market cap.

Based on cumulative returns since 2010, the cap-weighted portfolio lost 41.8% between November 2021 and December 2022—a period of rising interest rates and growth stock underperformance (Display, left). In contrast, the style-balanced portfolio fared much better for most of the period and its 2022 sell-off was more contained.

The Solution: Build More Inflation-Resilient Exposures

We think the style-balanced strategy’s stronger showing stems from a more effective balance between growth and value exposure as well as less stock concentration—an issue with the passive market-cap-weighted strategy.

The cap-weighted portfolio’s –0.66 value score (Display, center) signals its heavy growth exposure, making it much more susceptible to the underperformance typical in a high-inflation environment. In contrast, the style-balanced future-resources portfolio’s value score is close to zero, indicating no significant tilt to either growth or value—an attribute that drove its relative success–especially in rising-rate environments.

Also, the passive cap-weighted portfolio had 50% of its holdings concentrated in just five stocks, making it highly vulnerable to the fates of a very small cohort (Display, right). In contrast, the style-balanced portfolio was much more diversified in terms of stock weightings, with less than 5% of its holdings in the top five.

Note that style-balanced construction would require more trading and rebalancing than a simple cap-weighted approach. That’s the key to keeping the growth-value profile balanced by reducing exposure to stocks that have become expensive and increasing exposure to those that cheapen. But our simulation indicates the required trading activity would be in line with normal trading patterns of the average active stock portfolio.

The Big Picture

The style-balanced future-resources portfolio doesn’t win all the time. It may well trail the cap-weighted approach when yields fall sharply. But as we see it, future-resources investing is a marathon, not a sprint. That’s why we think applying style-based factors to construction can produce a diversified inflation-protection allocation that may provide a cushion for when inflation and yields rise while offering exposure to an important secular theme.

We think future-resources companies have a key role to play in the path to decarbonization. But given current inflation pressures, it’s important to embrace these growth-oriented companies thoughtfully rather than in a passive approach that carries sizable risks. Getting the calculus right can provide investors with yet another inflation-fighting tool in a real-return strategy.

Vinod Chathlani is Lead Portfolio Manager—Multi-Asset Solutions, Cherie Tian is Portfolio Manager—Systematic Equity and Hedge Fund Solutions and Mark Gleason is Managing Director—Multi-Asset Business Development at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams, and are subject to revision over time.