The move to confer reserve status on China’s currency is part of a process that could lead to nearly US$3 trillion being injected into the country’s bond and equity markets. We’ve taken a close look at where the money could come from.

On its own, the inclusion of the renminbi (RMB) in the International Monetary Fund’s (IMF’s) basket of reserve currencies, known as the Special Drawing Right (SDR), could lead to capital flows of US$30 billion into China within the next 12 months.

These will come from countries that receive IMF funding. IMF programs use SDR as a unit of account, and countries that benefit from these programs need to hedge their liabilities in the underlying SDR currencies. The SDR basket is equivalent to US$280 billion, and the IMF has announced that the RMB will account for 10.92% of the basket—hence the US$30 billion.

This is relatively small in the scheme of things, however. The significance of the RMB’s inclusion in the SDR is that it’s a measure of the progress China has made to date with key reforms, such as the internationalization of its currency and the liberalization of its capital account.

Our research shows that a continuation of these reforms will force a rebalancing of global portfolios that could result in inflows to China of nearly US$3 trillion by 2020.

To put these figures in perspective, and to gain a sense of the overall shape of the portfolio rebalancing, we have carried out an analysis of the likely sources of these flows and how they will be distributed across China’s capital markets.

We have analyzed expected flows by asset category based on index weightings, types of investors and what we know of investors’ typical asset-allocation patterns.

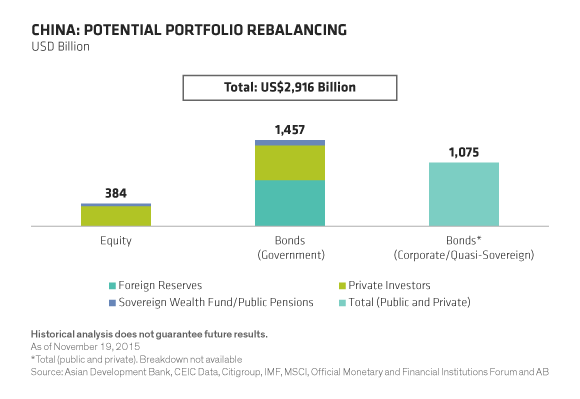

US$2.5 Trillion for China’s Bonds…

Given the size of China’s government bond market, we expect it to account for 6.8% of the Citi World Government Bond Index. The index will be capitalized at around US$21.3 trillion after the bonds inclusion, so flows into the sector will need to be about US$1.46 trillion just for portfolios to maintain index weight (Display).

Of these flows, we expect US$783 billion from global central banks, based on our assumption that they allocate about 7% of their US$11.18 trillion in foreign exchange reserve assets into RMB, and that they invest most of it in government bonds.

Another US$90 billion will come from other public sector investors, such as sovereign wealth funds and public pensions. Their assets under management (AUM), excluding foreign exchange reserves, total US$18.24 trillion (according to the Official Monetary and Financial Institutions Forum, as of June 10, 2015). There are no detailed breakdowns of portfolio allocations, however, so we assume that these institutions allocate a total 66% to bonds, of which 25% is allocated overseas and 60% is allocated to government bonds. From this, we estimate that 5%, or US$90 billion, will be allocated to Chinese government bonds. Private sector investors will account for US$584 billion (US$1.46 trillion minus US$783 billion minus US$90 billion).

China’s corporate and quasi-sovereign bond sectors could receive inflows of US$1.07 trillion. We estimate this on the fact that municipalities, policy banks and corporate bonds currently have about US$5.4 trillion on issue, and on the assumption that overseas investors in these sectors will hold 20% (which is similar to foreign investor holdings in comparable markets elsewhere).

In total, China’s government and corporate bond markets will soak up inflows of US$2.53 trillion (US$1.46 trillion plus $1.07 trillion).

…and US$384 Billion for Equities

Our research suggests that foreign capital inflows into China’s equity markets will total US$384 billion. This figure is based on a statement by index provider MSCI that China A shares will account for 10.2% of the MSCI Emerging Market Index and on our estimate that the index will be capitalized at US$3.76 trillion when China is included.

Of this US$384 billion, US$43 billion will come from sovereign wealth funds and public pensions. We arrived at this figure by assuming that these investors allocate 22% of their US$18.24 trillion AUM to equities and, of this, 10.6% to emerging markets and then 10.2% of that amount to China A shares. The balance of the US$341 billion (US$384 billion minus US$43 billion) will be held by private investors.

In light of these estimates, we believe that investors should maintain a balanced view of the risks and opportunities in China, weighing the country’s slowing economic growth against the long-term benefits—such as these inflows—which are likely to result from the government’s reforms.

This article previously appeared in the Financial Times.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.