Sovereign bonds have long been the prime defensive asset for multi-asset portfolios. But in today’s extraordinary market conditions, should investors make more extensive use of other defensive choices?

Multi-asset investors have always been able to access a full toolkit of investment strategies to help reduce downside risk. Over the last four decades, though, they haven’t had to look any further than developed-market (DM) sovereign bonds, which have been the ideal portfolio diversifier, providing reliable protection, deep liquidity and meaningful income simultaneously. Even over the last decade of meagre yields, the defensiveness of sovereign bonds has been impressive. For multi-asset investors, using sovereign bonds was like buying insurance for the portfolio but getting paid a premium for it.

Going forward, however, this windfall from sovereign bonds is unlikely to be as bountiful. Multi-asset investors will likely have to make more flexible and comprehensive use of their defensive toolkit than they have in the past.

Sovereign Bond Returns May Be More Muted in a Policy-Constrained Era

Several factors have eroded the payoffs for investing in sovereign bonds and may moderate their defensive characteristics in the future.

First, record low or negative yields have limited income potential. Investing in longer-dated sovereign bonds might not do much to address this problem, as yield curves are no longer reliably steep. As developed-world governments become more indebted, they may increasingly resort to yield-curve control strategies to contain their borrowing costs. So the opportunities for investors to benefit from roll-down strategies to generate return will probably be more constrained, in our view.

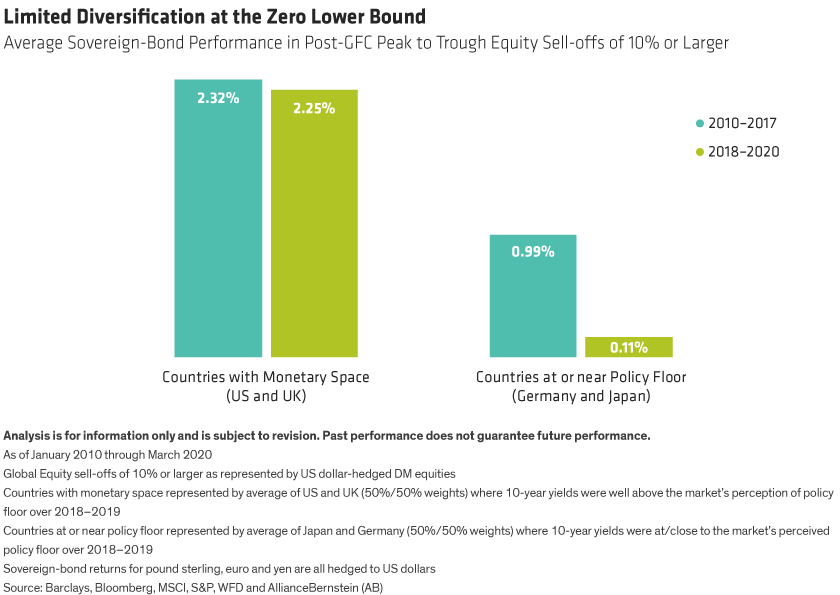

With yields already at such low levels, and as policymakers face constraints on their ability to cut rates further, we believe that sovereign bonds won’t protect so strongly when equity markets struggle. Although they may still be helpful in diversifying a multi-asset portfolio, the extent of their payoffs during market setbacks may be more modest.

In fact, this shift is already happening (Display, below). Sovereign bonds with yields close to zero and/or from policy-constrained issuers didn’t provide as much diversification benefit during the COVID-19 sell-off as in previous years.

Following the emergency measures sparked by the COVID-19 crisis, fewer sovereigns are likely to have headroom for significant rate cuts and/or major additional monetary stimulus. So the background for sovereign-bond performance may be even more challenging in the future. This reinforces our conviction that both the return and diversification properties of sovereign bonds are likely to be lower than they’ve been over the last four decades.

But that’s not all. Evidence of the reversal of globalization and the potential for monetization of elevated government debt levels threaten an end to secular disinflation trends. And the potential for a return to an inflationary regime reinforces the need for a diversifying set of defensive strategies over a longer-term horizon.

Wider Diversification Can Help

What can investors do to ensure their defense strategy remains robust in the future? We favor integrated multi-sector or multi-asset approaches that can use a wide array of defensive strategies, owing to their flexible mandates and ability to use a broad set of tools to manage unintended risks.

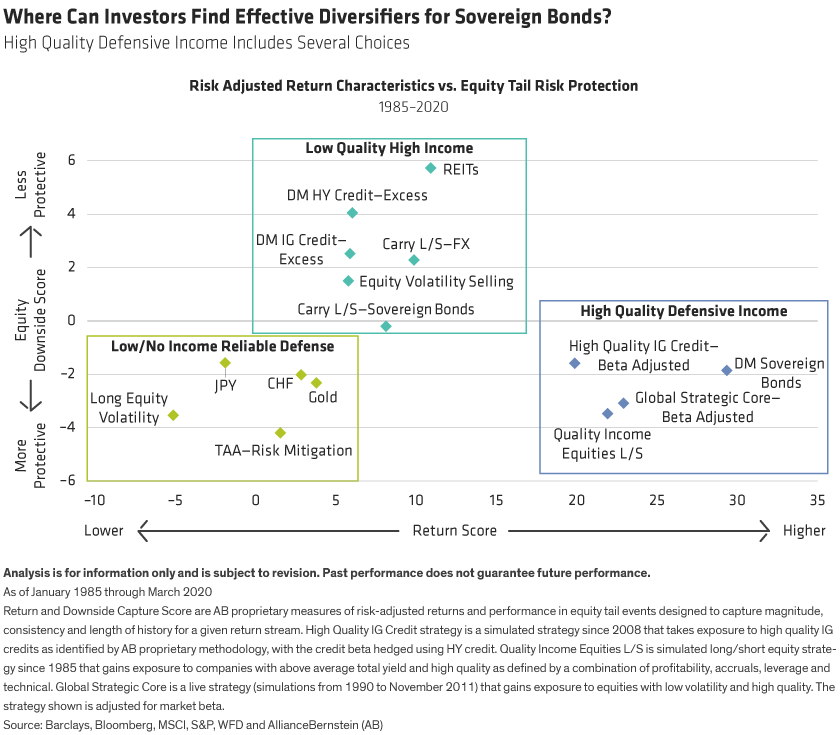

Although there are no direct substitutes for sovereign bonds, fortunately there are diversifiers with similar features. If investors can identify the desirable underlying characteristics of sovereign bonds, they can seek these characteristics in other investment strategies and then verify that these substitutes do indeed exhibit similar defensive behavior.

Sovereign bonds represent stable cash flows underwritten by high quality issuers as compensation for bearing rate and inflation risk (i.e., offering maximum payoff in negative-growth/inflation shocks when equity markets are selling off).

High quality companies may provide a viable alternative as an effective diversifier (Display, below). Stocks and bonds of high quality corporates with stable cash flows often provide similar characteristics for a multi-asset portfolio. Shares of these companies offer strong shareholder payouts and tend to be reliably defensive during equity sell-offs, while generating strong positive long-term returns with a meaningful income component. High-quality corporate bonds also tend to exhibit these characteristics relative to lower quality corporates. We believe stable, visible cash flows will continue to be attractive in most scenarios owing to interest rates being pinned at low levels by governments and their central banks. So in our view, high quality assets with attractive income generation will likely represent some of the most effective diversifiers in the future.

An unconstrained multi-asset approach makes it easier to benefit from the full range of diversifying assets and strategies. And our research suggests that balancing return streams with strong defensive characteristics alongside those that provide income can further improve portfolio characteristics.

How Sovereign Bonds Can Work in Future

It’s important to remember that sovereign bonds still have an important role to play for multi-asset investors. Carry is still positive in most cases and central banks could lower their policy floors, enabling lower rates and increased capital appreciation for sovereign bonds during crises. And the liquidity of DM sovereign bonds will stay unrivalled. Even so, return-generating efficacy and diversification potency is likely to be lower going forward. On that basis, investors should consider diversifying—not eliminating—sovereign-bond exposure in order to restore as much as feasible their income and protection benefits.

We believe multi-asset investors should consider reducing their strategic exposure to sovereign bonds and allocating to high quality stable cash flows across equities and credit to diversify their portfolios’ defensive allocation. And where possible they should adopt a more unconstrained multi-asset approach to add greater flexibility and create more robust portfolio characteristics.

Daniel Loewy is Chief Investment Officer and Head of Multi-Asset Solutions at AB.

Vinod Chathlani is Portfolio Manager—Multi-Asset Solutions at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.