The United Nations climate accord signed in Paris last December committed 195 countries to the first universal agreement to dramatically rein in greenhouse gases. We think it’s reckoning time for investors.

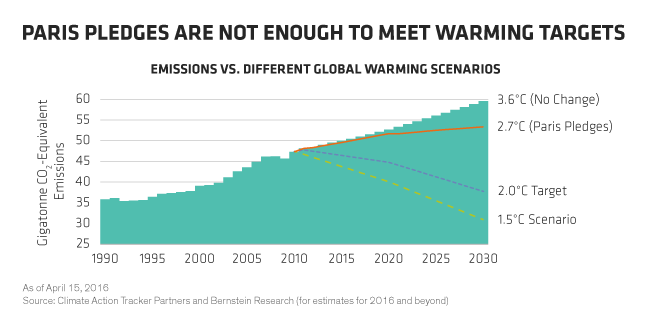

Reaching the treaty’s goals won’t be easy. Many climate scientists say that the gases already emitted into the atmosphere will lock us into warming of around 2°C—or precisely the agreed-upon threshold set at the Paris summit.* Heat-trapping atmospheric CO2 levels are already at 400 parts per million, widely considered a dangerous tipping point in the scientific community. The pledged reductions, if achieved, would still see temperatures rise by 2.7°C by 2030, according to a recent study (Display).

To make the Paris goals a reality, governments will need to put decarbonization at the heart of their fiscal and regulatory policies—a tall order, judging from history. Progress will also require broader and more aggressive private sector cooperation.

A Newfound Resolve

Even so, in the aftermath of the Paris talks, we sense a heightened resolve in the global response toward climate change. And it appears to have already begun to spur a virtuous cycle of international collaboration and action.

Indeed, companies around the globe and across sectors are realizing the competitive, public-perception and cost benefits of acting now rather than later. There’s been a dramatic rise in the number of businesses joining public-private and investor-led initiatives committed to specific climate-change goals. Increasingly, global brand giants like Google, Siemens and Coca-Cola are implementing programs to reduce carbon footprints and/or expand investments in renewable energy across their far-flung supply chains.

In its 2015 analysis of nearly 2,000 global companies totaling a market capitalization of US$35 billion, environmental-data nonprofit CDP reported, among other improvements, that corporate disclosures of projects and initiatives to reduce greenhouse gas emissions had climbed 15%. Private capital continues to pour into new clean-energy, low-carbon and infrastructure projects. A recent MSCI study found that an estimated one-third of the 2,400 companies in the MSCI ACWI equity index have already set carbon-reduction targets, which if met could lower greenhouse gases by 27% by 2030.

But these efforts are far from enough. Gains by the companies cited in the MSCI study would be largely offset by those without targets, leaving overall corporate emissions relatively flat and reductions far short of the collective country commitments. Among the index’s developing-world constituents, CO2 emissions are on track to rise nearly 25% by 2030; most of these companies lack carbon targets entirely.

Increasing Focus on Climate-Sensitized Portfolios

The warning signs are flashing for investors. Country-level CO2 reduction targets are likely to be ratcheted higher over the next decade, leaving many industries and companies vulnerable to even stiffer regulatory requirements and compliance costs later on—in addition to the growing operational costs of more frequent extreme-weather events and rising sea levels.

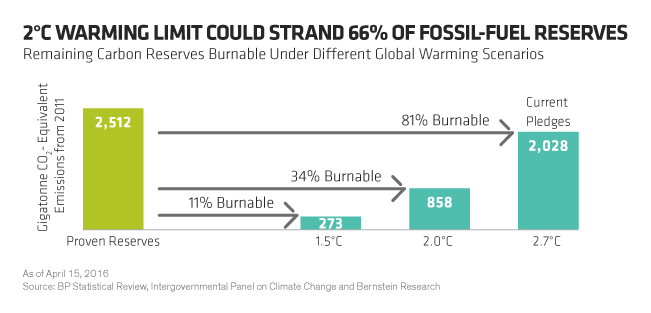

The growing decarbonizaton movement poses significant “stranded asset” balance-sheet risks for some commodities producers as declining demand for their resources leaves huge portions of reserves unused (Display). It’s also important for investors to monitor the possible impact of increasingly popular divestiture programs, which use vastly differing criteria, on the market values of portfolio holdings in targeted industries.

While investors typically focus on the obvious high-carbon sectors (commodities, utilities and air transport), the impact of global decarbonization is much broader, affecting even consumer-centric industries. For example, car-sales restrictions imposed by China’s largest cities are a threat to auto and related businesses, but the push to expand public transport systems and the surging demand for electric-vehicle batteries are creating new growth opportunities.

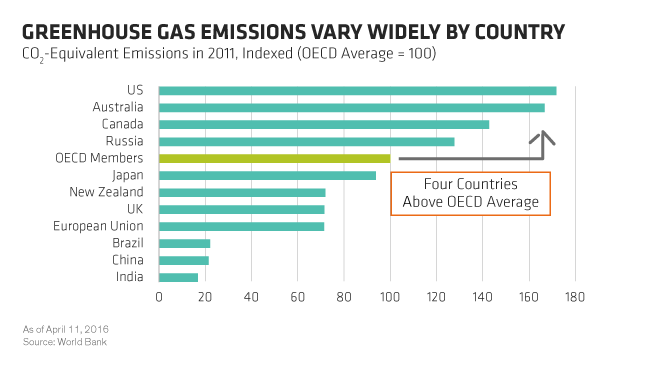

Evaluating these impacts is no easy task. A one-size-fits-all analytical approach won’t work, in our view. Carbon exposures and related risks vary widely across geographies (Display) and industries—and even among companies within the same industry. There are no set standards for measuring and tracking exposures or for shareholder disclosures, making comparisons difficult.

In our view, asset managers need to make climate-related issues a priority in their investment decision making. That means integrating the environmental, regulatory and social costs into their forecasting and selection models, as well as engaging with managements to get answers to questions about their companies’ transition strategies and long-term financial vulnerabilities to these risks. It also means seeking more exposure to the future winners of the low-carbon energy transition.

While third-party screening tools are helpful, analysts must do their own case-by-case research and develop their own measurement and tracking standards to get to the bottom of what’s really going on. The investment industry also needs to continue supporting shareholder proposals for greater data transparency and standardization of reporting of climate-related exposures.

We see the corporate response to global warming becoming a pivotal factor in separating future investment winners from losers. It’s time to heed the new climate-change calculus.

________________________________________

*The Paris accord aims to limit the planetary temperature rise to less than 2° Celsius (3.6° Fahrenheit) above preindustrial levels, which most scientists concur would mean keeping levels of heat-trapping carbon dioxide in the atmosphere below 450 parts per million. The Paris accord will come into force when countries representing at least 55% of total global greenhouse gas emissions join the agreement. To date, at least 34 countries representing 49% of greenhouse gas emissions have formally joined, or committed to joining, the agreement this year. Emission targets are not legally binding, but the nations have pledged to establish a framework for monitoring, measuring and verifying emissions reductions and to update their progress every five years.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

For more ways to pursue good returns and good values in your portfolio, explore Inspired Investing, a new podcast series where senior leaders at Bernstein share their thoughts on investing with purpose, first-hand and check out related blogs here.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.