Planning can be daunting when you’re young and have a very long time horizon to consider. If you’re 30—or even 45—you can’t know how your spending needs and income will develop in the decades ahead, or how the capital markets will perform.

But take heart: A long horizon also gives you flexibility. Young investors have more ways to improve or change their financial outcomes than older investors do. Young investors also have an often unrecognized asset in their human capital—their ability to generate financial capital that they can invest, which has significant implications for how they should invest.

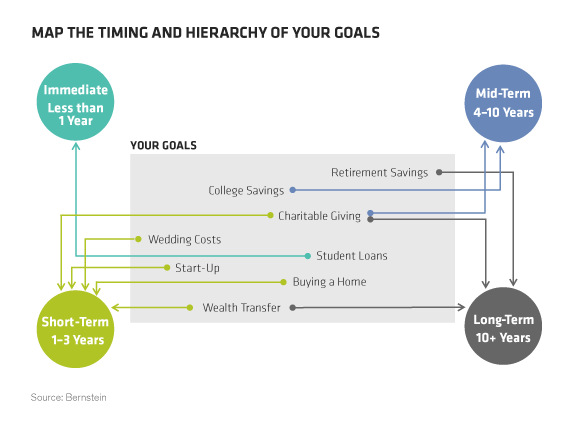

Identify Your Goals

You can’t devise a financial plan if you don’t know what you’re aiming for. Just as you need a way to search and organize everything you store in the cloud, you need to map your goals.

This Display provides a simple guide to mapping out the timing and hierarchy of the broad range of goals that may matter to you.

Take the time to consider carefully your priorities and where they fall on your time line, at least for now. How soon you plan to buy a house and the age you’d like to retire, for example, can have a big impact on the asset allocation most likely to achieve your goals.

Then, rank your priorities by their importance to you, and divide them into must-haves and nice-to-haves. For many people, buying a home and funding their children’s college education and their own retirement are primary goals; charitable giving comes second.

Chances are, your spending priorities will change over time, as your life evolves. That’s okay. Your income will probably change, too. You’ll probably need to revise your time line in the years ahead, perhaps repeatedly.

Understand Your Balance Sheet

Next, take stock of your assets and liabilities (or debt). Your assets may well be greater than you think—even if you’ve recently graduated from college with significant student debt.

Most recent graduates think their most important assets are their checking accounts, or perhaps their cars. That’s wrong. In the absence of a sizable early inheritance or financial help from parents, most recent graduates’ greatest asset is their human capital. A 25-year-old typically has 40 years or more of potential employment and saving ahead. That may be worth a lot—and it will affect your ability to take investment risk.

For more information about your human capital, click here.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.