Smart beta strategies are growing in popularity, and investors have a lot of forms to choose from. One key question to ask is: How proactive should smart beta be in avoiding unintended risks?

At its core, smart beta is a portfolio that’s built differently from capitalization-weighted market indices. Smart beta creates exposure by allocating to certain risk premiums, including value, momentum and defensive. Value, for example, means owning cheap securities that should generate strong returns.

Smart beta has been around for a long time, but interest has grown since 2008, because the demand for transparency and lower cost has increased—so has the desire for exposures with low correlation to broad markets. Interest in smart beta has also extended beyond equities into fixed income.

There are a number of approaches to smart beta, ranging from simple rules-based index construction using an index provider (used for most passive smart beta) to fully customized, actively managed combinations of risk premiums that complement a core portfolio.

Be Aware of Unintended Risks

Ideally, investors would choose an approach that balances their considerations of cost, liquidity, transparency, unintended risks and effectiveness. But it’s not easy to answer some of these questions. How would you choose a version of smart beta without knowing whether it could magnify existing exposures and increase portfolio risk?

How much impact do these trade-offs have? Let’s compare three types of equity smart beta drawn from the MSCI World stock universe—each built to exploit value and momentum premiums. A basic smart beta version simply takes the most attractive stocks based on value and momentum measures. A second version, MSCI style indices, uses a proprietary approach to tilt to value and momentum. And a pure factor smart beta portfolio uses risk modeling to minimize risk exposure to sectors, styles, market betas and other characteristics.

Since 2008, the three smart beta versions had relatively high correlation but produced different outcomes—mainly because of sector biases in their design. In terms of value, the simple and index versions have been overweight financials and underweight technology—exposures that currently account for more than two-thirds of their underperformance versus the pure smart beta portfolio.

If technology underperforms while financials rebound, the pure portfolio would probably underperform the index version. So, the pure smart beta portfolio sacrifices some intensity in value exposure in order to reduce unintended risks. Index-based funds that pursued momentum can be underexposed to value and have very large sector and/or country biases. Smart-beta biases evolve, and it takes careful management to keep common risk exposures from building up.

Make Smart Beta Work Smarter

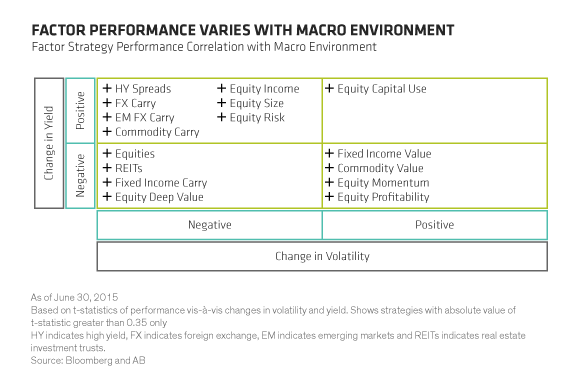

One way to keep common risk exposures from building up, and to protect against drawdowns, is to be aware of how the performance of different factors changes as the macro environment evolves (Display).

Take an environment with falling yields and rising volatility. This situation would be consistent with a flight-to-safety scenario with economic turmoil. We’d expect strategies linked to duration (like value in fixed income), defense (such as equity profitability) or rapid adaptability to changing market leadership (equity momentum factor) to perform well.

Because the effectiveness of risk premiums changes with the macro environment, tactically allocating among them has the potential to enhance smart beta results. Because risk premiums have somewhat similar risk-adjusted returns over time but behave differently, it’s possible to build a portfolio that allocates risk equally to each factor. Then risk can be actively tilted toward more attractive factors as valuations and the business cycle evolve.

Putting It All Together: Assessing Opportunities

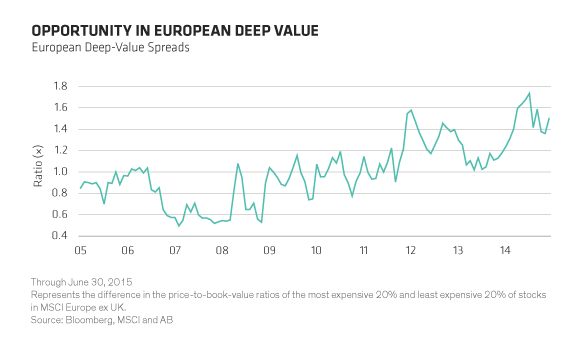

In our view, a holistic assessment is the best approach to identifying which factors are attractive and which aren’t. This analysis should include a quantitative assessment of potential upside, an evaluation of the macro environment and, finally, judgment. Using this lens, one opportunity we see is in European distress, which has driven the valuation spread for deep-value stocks wider (Display).

Of course, valuation spreads have been widening since 2009, so investors need to agree with a certain investment thesis: quantitative easing and a willingness to promote credit creation will drive investors toward value stocks, given the greater opportunity.

Smart beta strategies offer low-cost, improved transparency and access to return sources that complement the rest of a portfolio. But there are trade-offs to consider in choosing an approach, and the ability to avoid unintended risk exposures is a key consideration. In other words, investors need to decide how smart they want their smart beta to be.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.