Emerging market growth is faltering, volatility is spreading and many investors are on edge. But while risk has clearly increased, so has return potential. Investors need to keep a close eye on both.

Don’t get us wrong: the short-term risks are high. China and other formerly high-flying emerging economies are slowing sharply. The US Federal Reserve is expected to raise interest rates soon. And financial market liquidity isn’t what it once was.

All this calls for caution. We think a small underweight in equities, for example, makes sense in the current environment.

Don’t Write Off Developed-Market Equities

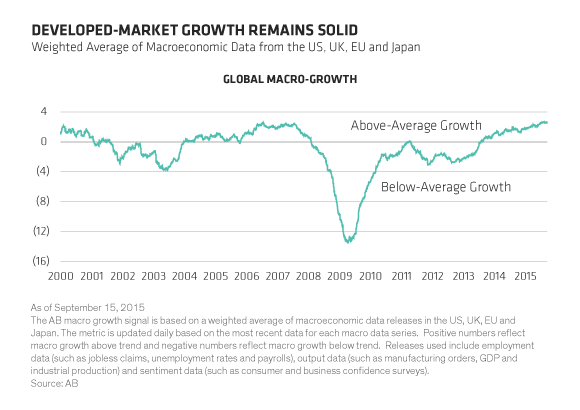

But it’s also important not to overreact. For instance, there’s no sign that a sharp slowdown in emerging markets is spilling over into the developed world, where economic fundamentals are still solid. Based on a group of key indicators, developed economy growth remains robust (Display). And it’s in line with economists’ forecasts. That should bode well for growth-sensitive assets such as developed-market equities.

What’s more, we think the recent sell-off has left valuations near average in many markets. That makes more big declines less likely. Our research also shows that falling commodity prices usually benefit economies and sectors that depend on consumption—that’s more good news for the developed world. Meanwhile, the decline in some currencies may provide another source of economic stimulus.

Overall company quality also stacks up well for equities. Corporations around the world are in pretty good shape these days. Stock buybacks, which increase shareholder value, have been on the rise, while new stock issuance, which dilutes value, has been low by historical standards. In our view, this is reason to be optimistic about the return potential of developed-market equities despite the economic slowdown.

Blinded By Risk

These and other opportunities may help boost returns, but an investment process that looks only at risk may miss them. That can be a hazard for some increasingly popular “risk-aware” strategies. Some of these approaches use volatility or value-at-risk techniques to measure the level of portfolio risk over a given time frame. If the risk level falls, managers buy more assets. If it rises above a certain level, they sell assets to bring it back into line.

When the summer began, volatility and market measures of risk were low, while valuations on a range of growth-sensitive assets were approaching their post-financial-crisis highs. As a result, investment approaches that focused purely on risk would likely have been heavily overweight equities when turbulence picked up in August.

Over the next week, the S&P 500 Index plunged nearly 13% and implied US equity market volatility, as measured by the VIX, more than doubled. A portfolio approach based on risk alone would likely have underperformed and reduced equity exposure substantially.

As it turns out, that was the worst time to reduce risk. Investors who did ended up underperforming, because the market recovered and risk fell. In fact, when markets started to rebound, some investors that use these strategies began to buy back the equity they had sold just a few weeks earlier.

The Risk of Disappointing Results

To put it another way, investors who base their decisions solely on risk and volatility would probably have been whipsawed by the rapid rise and fall in risk. We suspect their returns would have suffered, too—both when equities were on the way down and when the market started to recover.

This isn’t to say that risk-aware strategies were the main driver of the recent market turmoil. Real concerns about global growth—particularly in emerging markets—and liquidity played a big role. Still, our experience shows that investing based solely on risk can deliver disappointing results.

Striking the Right Balance

A better way, in our view, involves taking both risk and return into consideration when managing portfolios. That approach has helped this summer. Even when risk and volatility were near their lows, other indicators, including stretched equity valuations, worsening credit conditions and the potential for higher US interest rates, suggested lower returns.

Investors who paid attention to those “return” signals and dialed down their exposure to risk in July stood a good chance of delivering better returns during the late summer sell-off than those who navigated by risk alone. They also would have been in a better position to take advantage of the improvement in valuations that recent market turbulence has created.

Of course, weighing risk and return will always be a delicate exercise, and investors will behave differently based on how much risk they want to bear in their portfolios. But we think the best strategy involves striking a balance between the two. Focusing on risk alone could mean missing the big picture—and missing out on the chance to generate higher long-run returns.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.