European equity markets are still struggling to overcome the effects of the pandemic. But diligent investors who look beyond the crisis can find surprising investment candidates among the wreckage, even in sectors such as aerospace and retail, which were hit particularly hard.

European stocks are lagging their global peers for the current year. The MSCI Europe Index fell by 12.2% through September 24, 2020, in local currency terms, while the MSCI World Index declined by only 1.7% and the S&P 500 advanced by 1.9%. We believe this is partly due to the perception early in the crisis that Europe would struggle more than other regions to contain the spread of the virus. But despite encouraging successes in many European countries, decisive lockdown measures and surprising cooperation throughout the region, Europe’s recovery path has not yet been fully reflected in stock prices.

Sharper Questions for Tougher Markets

Of course, this crisis in unlike any other. So, on top of their usual due diligence, investors should ask the following questions when analyzing a company: How exactly has demand been impacted, and for how long? Is the demand destruction due to behavioral or structural changes? Have the competitive dynamics of a sector changed? Does a company have the balance-sheet strength to survive these trying times? And finally, how much confidence can investors have in any of the answers to those questions, given the uncertainty about the pandemic and macroeconomic growth?

When asking these questions, investors should not automatically rule out distressed sectors. Indeed, two areas that might seem to be unlikely spots for investment deserve attention: retail and aerospace.

Aerospace: Finding Companies That Can Withstand Stress

Europe´s aerospace industry is facing unprecedented distress. Companies are facing significant demand destruction caused by governments’ near-total shutdown of commercial aviation. And behavioral changes also are taking their toll: tourists are still reluctant to fly, preferring to spend their holidays close to home, while business travel has been largely replaced by video conferences.

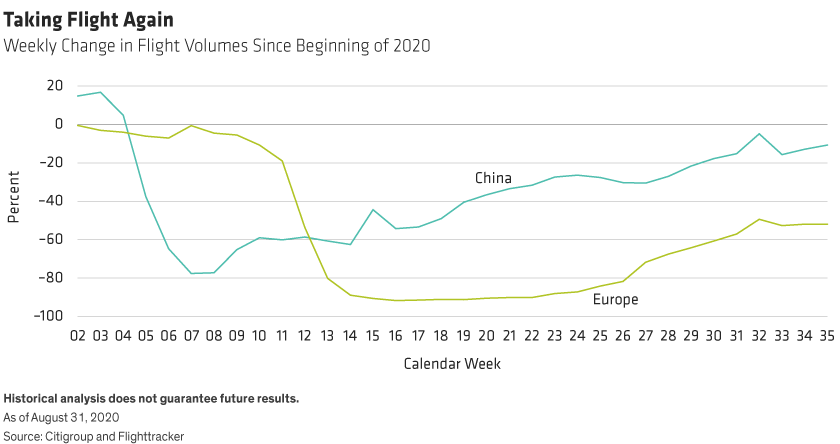

Are package holidays and business trips a thing of the past then? Probably not. People love to travel. China, which was the first country to emerge from lockdown measures, has seen passenger volumes recover to about 80% of pre-pandemic levels. Europe should follow a similar path, in our view, once the pandemic subsides (Display).

In this environment, some legacy carriers may not survive. However, more nimble companies directly exposed to the short-term disruption may be better positioned for long-term recovery. For example, Ireland-based AerCap rents out planes to airlines. At a time when large carriers are reluctant to buy new planes, AerCap may benefit from the lack of planning visibility, and it gets paid even when its planes are half-empty or sit on the ground. Hungarian discount carrier Wizz Air is another example. The company boasts a low-cost base and doesn´t rely on business travel for its revenue.

Retail: Online Surge Fuels Digital Transition

The retail industry in Europe presents a different picture. There is a stark contrast between the economic winners and losers of the lockdown. Companies that are either fully online or that already had a strong e-commerce presence are thriving. Meanwhile, legacy chains that rely heavily on brick-and-mortar shops are struggling even more than before the onset of the pandemic.

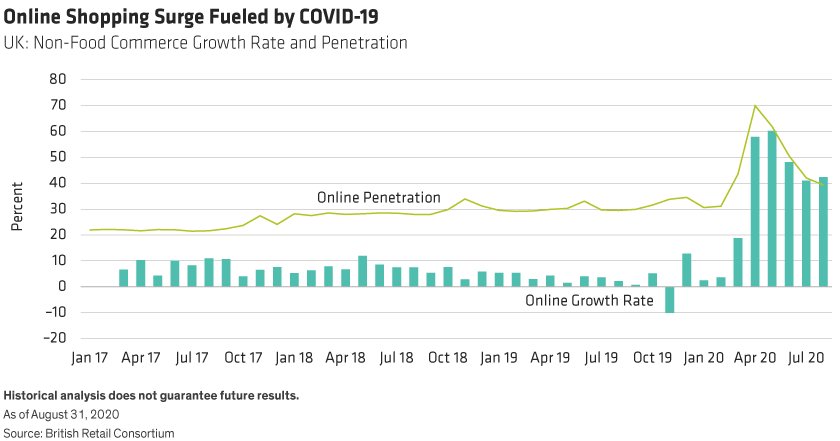

Before COVID-19, Europeans hadn’t embraced online shopping as much as American or Asian consumers. Certain market segments, such as elderly customers, were skeptical of buying online. The lockdown has virtually forced them to give it a try and has now generated a source of sustainable demand for the online retail industry. In the UK, for example, monthly online shopping growth has surged from below 10% in early 2020 to above 40% in recent months, boosting the penetration rate of digital retail (Display).

These trends distinguish between companies that are better equipped to negotiate the transition to online shopping. Clothing retailer Next Retail and fashion jewelry-maker PANDORA both fit the bill. UK-based Next, with its historical roots in its mail-order catalog business, has always had a strong online presence. PANDORA’s products are tailor-made for online sales, and the Danish company had already embarked on a program to increase its online presence prior to the crisis. Both companies have relatively outperformed expectations recently. Companies that have been less successful at modernizing their business models are just beginning to reduce their reliance on physical stores, and it will take time for them to catch up.

European equity markets are still far behind their US peers. Yet this underperformance has also created opportunities for investors who take a selective, research-driven approach to European companies. In battered sectors such as aerospace and retail, we believe investors can find misunderstood companies with surprisingly strong business dynamics that can underpin attractive long-term return potential as a recovery takes root across the region.

Tawhid Ali is Chief Investment Officer—European Value Equities at AllianceBernstein (AB)

Andrew Birse is Portfolio Manager—European Value Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.