The battle for Brexit has undermined traditional political affiliations and triggered changes in the UK’s constitutional order that could affect future governability. We may now be approaching the end game, though the outcome might not be the one markets are counting on.

Cutting through the Parliamentary bluster, let’s look more closely at where things stand at this point in the lengthy Brexit tug of war.

The Current State of Play

Boris Johnson remains the UK prime minister, and (in theory at least) remains committed to leaving the EU on October 31—with or without a transitional deal. Unfortunately for him, there is little realistic prospect of the UK and EU reaching a deal in the short time available. Moreover, Parliament has passed the Benn Act compelling the government to ask for an extension of the Article 50 withdrawal date if a deal can’t be reached by mid-October.

Faced with these roadblocks, Johnson has tried to trigger an early election but has so far been unsuccessful: the prime minister no longer has constitutional authority to dissolve Parliament, and opposition parties have refused to support a no-confidence vote until after an extension agreement with the EU. If Johnson can’t reach a deal with the EU and doesn’t want to defy Parliament, he has only two options: He can comply with the Benn Act, seek an Article 50 extension and hope Brexit supporters recognize he has acted under duress. Or he can resign.

There is also speculation that Johnson might take the highly controversial step of trying to circumvent the Benn Act. Opposition parties might therefore consider toppling the government and replacing it with an interim government, or forcing Johnson to seek an earlier extension of Article 50.

Laying Out a Brexit Roadmap

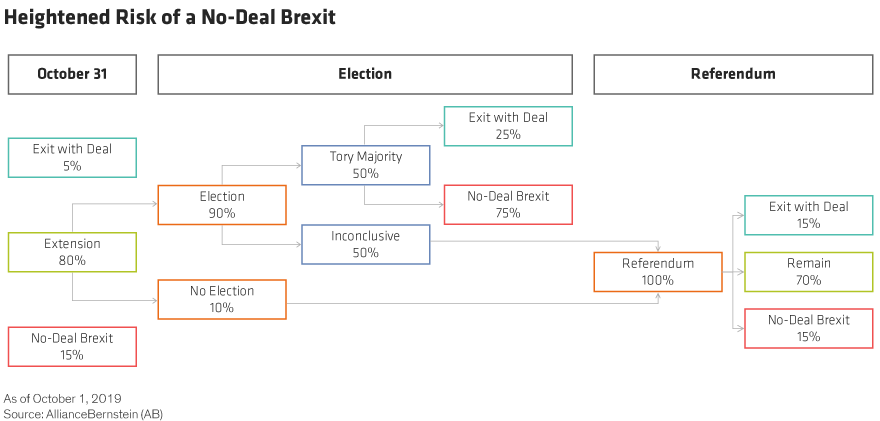

With the UK venturing deeper and deeper into uncharted political and constitutional territory, it’s impossible to know exactly how things will play out in coming weeks. In broad terms, though, the Brexit roadmap now looks something like this (Display):

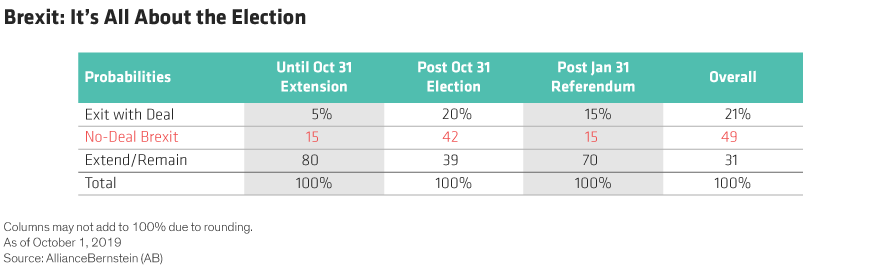

With Parliament in control of the Brexit process, a further extension of Article 50 is by far the most likely outcome. We now put the probability of an extension at 80% (up from 50% at the end of July). We’ve also lowered the probability of a deal by October 31 from 15% to 5%, and reduced the probability of a no-deal Brexit from 35% to 15%.

Assuming the EU agrees to extend Article 50, the UK is likely to move quickly towards a general election (this may well be a precondition for an extension). The outcome of that election is likely to fall one of two ways: If the Conservative Party wins, the UK will almost certainly leave the EU early next year, probably without a transitional deal. But if the Conservative Party loses, a second Brexit referendum looks inevitable.

The odds of a second referendum would be heavily stacked in favor of either remain or an exit with a deal (soft Brexit). That’s not because of a radical shift in public opinion since June 2016, but because a pro-remain Parliament would find it hard to resist changes that would bias the result in that direction—including lowering the voting age and allowing EU nationals living in the UK to vote.

Focus on the Inevitable Election

The key event to focus on is therefore not the October 31 deadline but the election that will surely follow. According to recent opinion polls, the Conservative Party has an average lead of almost 10 points over the Labour Party. In normal times, that would translate into a healthy majority for Boris Johnson.

But these are not normal times: several factors make an early election too close to call. For one thing, it’s difficult to translate current vote shares into seats in the UK’s heavily distorted first-past-the-post system. In addition, not all polls give the Conservatives a commanding lead (it varies between zero and 15%, depending on the poll) and tactical voting by pro-remain parties could have an important impact. Finally, Conservative support could collapse if Johnson fails to deliver on his promise to deliver Brexit on October 31.

The probability of a no-deal Brexit is likely to fluctuate wildly in coming months. In the run up to October 31, we think it remains low at just 15% (Display).

But when a general election comes onto the horizon after October 31, the probability of a no-deal Brexit is likely to rise significantly (to 42%, according to our estimates) before receding again if the election results in a hung Parliament and second referendum. Overall, though, the probability of a no-deal Brexit is close to 50% right now, which is far higher than markets are pricing in.

Darren Williams is Director—Global Economic Research at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.