Capital markets have rebounded from their COVID-19-induced lows, but impacted industries have lagged substantially. That pessimism may be overdone in some cases, creating opportunities for multi-asset investors to exploit dislocations.

A massive post-March rally boosted the MSCI All-Country World Index roughly 50% from its trough on March 23, returning it near its pre-pandemic highs. But a closer look at the patterns of equity valuations suggest the market is pricing in a “new normal” of economic activity that’s largely virtual, with service and travel-related businesses never fully recovering.

We certainly agree that the new normal will be very different, but we also see excessive pessimism toward some of the sectors hit harder by COVID-19 social distancing and shutdowns. Even in these segments, businesses have continued to adapt—often in ways that foster greater operating efficiency and lower labor input, which help profitability.

Longer-Term Outlook Suggests More Solid Ground

There’s no doubt that prominent risks still loom. The potential for a second virus wave and possible further lockdowns is ever-present, especially with fall and winter around the corner in many parts of the world. Geopolitical risks include US elections in November and ongoing trade tensions with China. However, the tremendous global innovation effort in the race for vaccines and treatments could eventually offer a path forward, and in our view the longer-term outlook is on more solid ground.

For one thing, COVID-19 adaptation is accelerating the pace of digitization, which will most likely benefit scalable, capital-light technology business models disproportionately—and is also a positive for corporate earnings. The valuations discounted for the perceived winners aren’t anywhere close to the levels we saw during the tech bubble: unlike 2000’s loss leaders, these firms possess substantial cash flows and market share.

Massive central bank stimulus should keep yields in check for a while, giving the global economy time to heal. This environment should be particularly friendly to growth stocks: their cash flows are farther in the future, so their valuations should benefit from persistently low interest rates. Positive economic surprises as well as improvements in high-frequency data on spending and transactions suggest a gradually healing global economy.

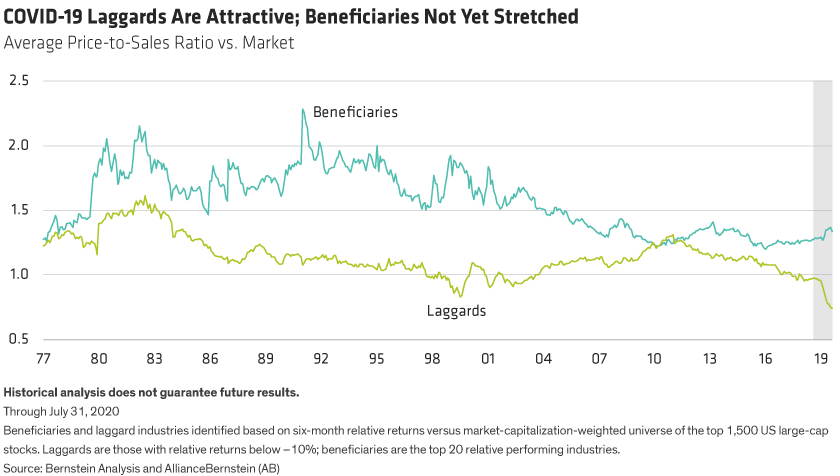

Some COVID-19 Laggards Suffering from Overreaction

That being said, the expected returns for risk assets are lower, given the run-up in valuations from the market rebound. For multi-asset investors, it’s important to be able to allocate flexibly across many markets and factors in order to uncover and capture opportunities.

In a longer-term secular shift, it’s not unusual for pessimism on negatively impacted businesses to overshoot and create opportunity. We’re starting to see evidence of this overreaction in industries the market has deemed to be losers in the time of COVID-19. They’re trading at historical valuation extremes, as measured by the price-to-sales ratio relative to the market (Display).

But affected businesses have been adapting. For example, many restaurants are now offering curbside pickup of meal orders accompanied by contactless payment. Retailers are accelerating the shift to online channels—and in some cases offering shopping by appointment. Hotels are doing away with traditional daily housekeeping service as a preventive measure against the spread of COVID-19.

In fact, the earnings expectations of impacted companies are starting to show signs of improvement. The last time laggards traded at such a deep discount versus the market was in the late 1990s. Given this valuation disparity, we believe they’re likely to provide attractive tactical exposure to the next leg of the economic recovery.

On the other side of the coin, valuations for COVID-19 beneficiaries remain moderate relative to the market—despite substantial outperformance so far in 2020. Because we expect the shift to digitalization will be lasting, we think it makes sense to consider barbell exposure to these two equity segments. From a geographic standpoint, that idea can be expressed as exposure to secular growth through US equities, which are overweight technology, while accessing procyclical exposure through Asian economies.

Could Bond-Proxy Equities Come Back into Favor?

Another legacy of COVID-19 appears to be another leg down in already historically low sovereign bond yields, with the US joining countries that have reached the zero-rate lower bound. Given central-bank accommodation and a low inflation backdrop, government bonds are still likely to be effective diversifiers to risk assets, and exposure to other fixed-income sectors offers additional income.

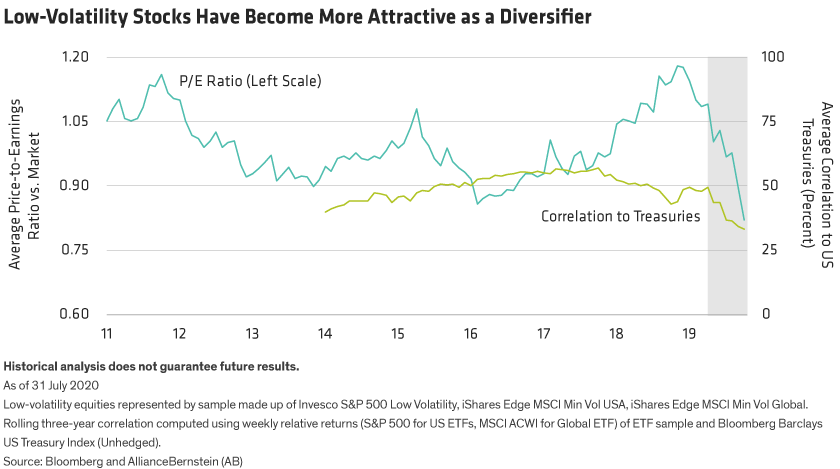

But given low yield levels, it makes sense for multi-asset investors to explore a wide range of income enhancers. Equities that trade as bond proxies, such as low-volatility stocks , which tend to have stable cash flows and high dividend yields, are one source. They suffered as the pandemic strained cash flows and investors became worried about dividend sustainability. As this happened, the historically positive correlation between these stocks and US Treasury bonds decoupled—and valuations took a hit (Display).

That leaves valuations attractive, and if, as we expect, the economy continues to gradually normalize and liquidity concerns abate, these stocks could once again find favor with investors seeking sources of stable income with some potential for upside from valuation recovery. This scenario isn’t unlike the experience of the slow-growth, low-rate environment following the GFC. Of course, a new illiquidity event from another round of broad-based COVID-19 lockdowns poses a significant risk factor.

To sum things up, markets seem on better footing today, but the road ahead isn’t likely to be smooth. For multi-asset investors, there’s a premium on flexibility—both in capitalizing on dislocations from COVID-19 and in bolstering portfolios against inevitable periods of unsettled markets.

Daniel Loewy is Chief Investment Officer and Head of Multi-Asset Solutions at AB. Caglasu Altunkopru is Head of Macro Strategy in the Multi-Asset Solutions Group at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.