Japanese equities have long been overlooked by many global investors. But they may be on the verge of a comeback as the worldwide economic recovery gathers pace and the high-flying stocks that drove the global market rally in 2020 show signs of fatigue.

Even as the COVID-19 vaccine rollout has improved the outlook for the global economy, many investors remain reluctant about putting more money into equities. For some, there’s a nagging concern that the market may have already priced in good times ahead. Yet there are still laggards that are well positioned to benefit from a broadening in the market’s recovery. Japanese companies, particularly value stocks, offer just such characteristics after underperforming for most of the past decade (Display).

After years of underperformance, Japanese stocks are attractively priced versus global peers, with the MSCI Japan Index trading at a forward-earnings multiple of 16.1x at the end of May, a 22.0% discount to the MSCI World Index. And in a sign of the pent-up energy in the more undervalued parts of the Japanese market, the MSCI Japan Value Index has been off to a roaring start in 2021, gaining 15.6% through May 31, compared with 0.2% for its growth counterpart.

Broadening Equity Rally to Support Japanese Market

Why have Japanese stocks—and value stocks globally—fallen behind so much? The main reasons, in our view, are twofold. Prior to the pandemic, Japanese stocks were shunned, mainly over concerns about an economic downturn after one of the longest periods of expansion in the post-World War II era. Japanese companies are perceived to be vulnerable to slowdowns in their export markets, and many value stocks are in cyclical industries.

Then, when the pandemic began, the Japanese market and value stocks worldwide fell further behind due to investors’ focus on a narrow set of “quality growth” stocks—such as the global internet giants—whose gains accounted for a lion’s share of the global market rally in 2020.

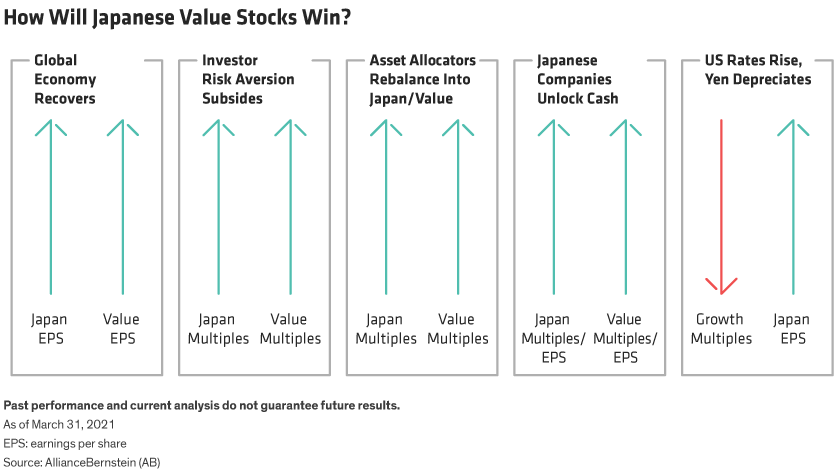

The tide has begun to turn in 2021, but what will it take for Japanese value stocks to make a more sustained recovery? In our view, several trends that are supporting value stocks globally could make an especially powerful impact in Japan. Our optimism centers on five main elements (Display).

First and foremost is the global economic recovery, which is already driving an earnings rebound at Japanese companies, particularly for the more cyclically sensitive value companies. Second, the economic upturn is likely to alleviate investors’ risk aversion, which in turn should help to re-inflate valuation multiples of Japanese stocks and value stocks. While Japan’s vaccination program got off to a relatively slow start, we expect it to speed up swiftly after a mass-vaccination process was launched in mid-May.

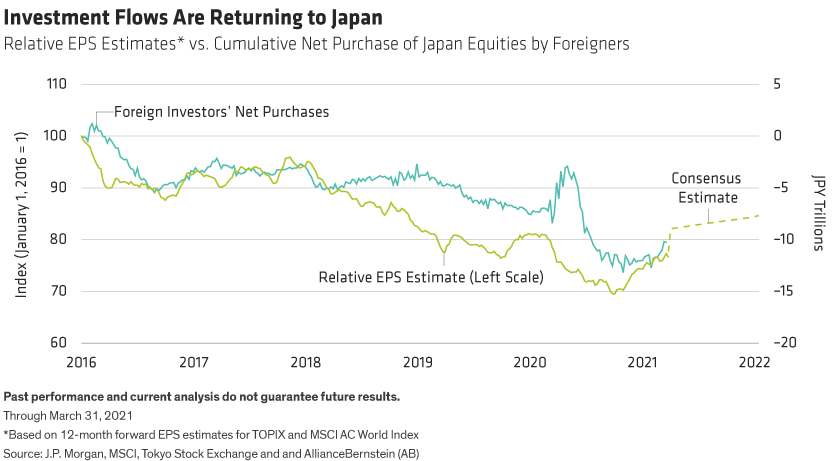

The third potential catalyst is a nascent reversal in investment flows. Global investors, who have been net sellers of Japanese equities over the past several years, are beginning to reduce their underweights as Japanese companies’ earnings growth is expected to outpace their global counterparts’. Relative earnings-per-share growth estimates, vis-a-vis global trends, have generally had a high correlation with foreign fund inflows (Display).

Balance-Sheet Reform to Boost Shareholder Returns

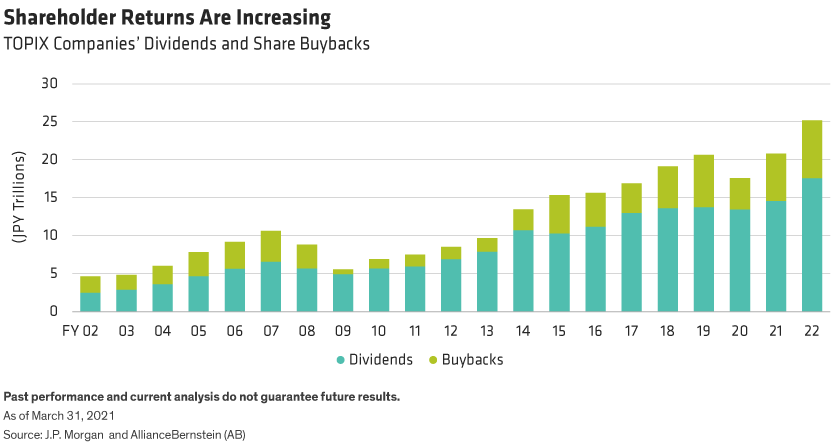

Balance-sheet reform should provide further impetus to Japanese stocks, particularly value names, in our view. This structural reform, sidetracked in 2020 due to the pandemic, should in turn boost shareholder returns. Japanese companies tend to have a large pile of cash on their balance sheets, with nearly half of the 1,000 largest companies in “net cash” positions—with cash and cash-like securities holdings exceeding their debt. In contrast, less than 25% of large-cap companies in the US and Europe have net cash positions.

The tendency to hoard cash, stemming from fear of a credit crunch, has negatively affected Japanese companies’ return on equity. But growing awareness of the need to either reinvest cash in profitable businesses or return cash to investors has prompted more companies to increase dividends and/or share buybacks in recent years (Display). With corporate governance becoming an increasingly critical issue for corporate decision-makers, balance-sheet reform is likely to continue, in our view.

Inflation? What Inflation?

The fifth factor that may aid Japanese companies’ comeback is upward pressure on inflation and interest rates, particularly in the US. In early 2021, a pick-up in inflation and a surge in US long-term interest rates triggered a correction in some high-flying growth stocks.

Growth stocks are more vulnerable to higher interest rates than value stocks because the premium on their valuation multiples reflects their expected future earnings. Higher interest rates would result in a steeper rate of discount in calculating the present value of that future income. And value stocks tend to be more heavily represented in industries that benefit from higher rates—such as banking—or higher inflation—such as materials.

Mild inflation is not necessarily bad for stocks. It certainly beats deflation, which has been a bigger concern for the Japanese economy for many years. Most economists expect prices in Japan to remain stable and yen interest rates to stay near their current low levels. In addition, an expansion in US-Japan interest-rate differentials could fuel a rise in the US dollar against the yen, which would help Japanese exporters.

Bumpy Road to Recovery

Japanese value stocks have been off to a strong start to the year. Although the pace of their recovery has slowed in the second quarter, the comeback is only beginning, in our view. We believe that Japanese value stocks stand to benefit from a broadening in the global market recovery—which in 2020 was centered on a narrow set of super-high growth stocks, mainly in the US and China.

The road ahead may not be smooth, as the pace of exit from the pandemic varies by country. But from a long-term perspective, macroeconomic trends should help release the pent-up energy of Japanese value stocks, which offer strong return potential for selective investors amid the challenges of the post-pandemic recovery.

Atsushi Horikawa is Chief Investment Officer—Japan Value Equities at AllianceBernstein (AB)

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.