European markets have been turbulent because of the region’s proximity to the war in Ukraine and economic links with Russia. Yet sector and industry performance has varied in ways that may not be fully justified by changes to their fundamental outlook. A closer look can help guide investors through these uncertain times.

The MSCI Europe Index fell by 5.7% in local currency terms this year through March 18. In the UK, the MSCI United Kingdom rose by 2.7% over the same period, owing to heavy weights in energy stocks. Both indices rallied in the week ending March 18 to recover almost all their losses since Russia invaded Ukraine on February 24. In January and February, European stocks performed slightly better than US markets, which were hit by a sharp decline in their tech-heavy components as interest rates resumed their rise; this pattern reversed somewhat in March.

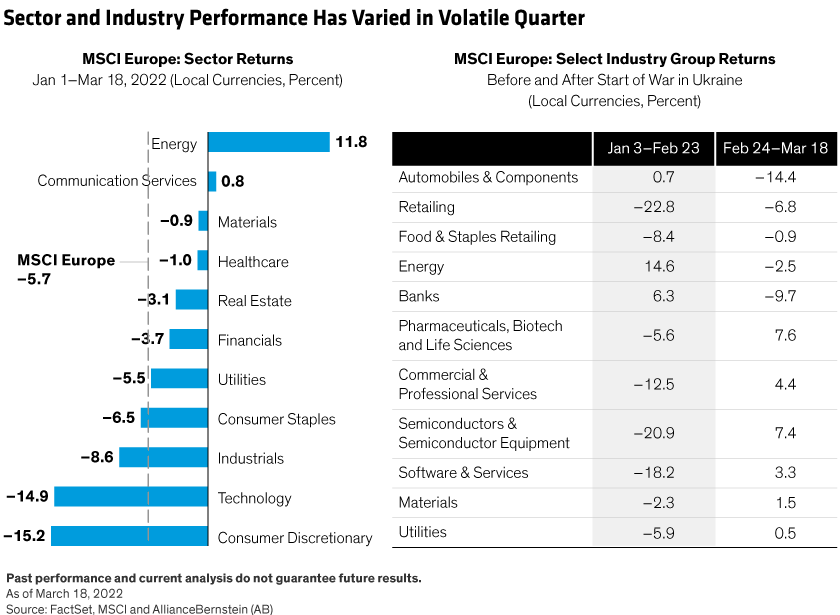

Sector performance has been mixed (Display). Europe’s energy sector has surged on rising oil and gas prices. Technology stocks have been hard hit, mostly before the war started amid a global sell-off in the sector. The healthcare sector has fallen more modestly, while communication services have risen slightly. Within some sectors, industry performance has diverged, too. For example, pharmaceutical stocks have been relatively resilient, while healthcare equipment and services shares tumbled. Food retailers have held up better than other consumer staples groups.

Several market trends help explain recent market performance. We believe these trends can provide investors with some direction for portfolios amid the volatility.

Recession Fears in Perspective

Macroeconomic growth worries are particularly acute in Europe. Since the region is reliant on Russian oil and gas supplies, the risks of inflation stemming from a potential loss of crucial supply are acute. Along with potential monetary policy missteps, Europe is especially vulnerable to stagflation—a painful combination of an economic slowdown and high inflation.

European banks are in the eye of the storm. Banks are hurt by stagflation, but benefit from rising interest rates, which widen net interest margins—the difference between income from loans and payments on deposits. Recession fears and concern about exposure to Russia and other risky markets are weighing on sentiment. Yet investors should remember that not all banks are the same. Well-capitalized lenders with little exposure to Eastern Europe, relatively resilient loan books and better balance sheets should be able to cope with a downturn.

Automakers have also been hit hard. Car manufacturers usually underperform in a recession, as consumers scale back purchases of big-ticket items. But before the war, expectations of auto sales volumes were already down to a near-30-year low of about 11 million a year. We believe sales are unlikely to fall much more from here, even in a recession. Shares of some carmakers may have dropped more than they deserve on overly negative expectations, in our view.

The industry also faces immediate disruptions related to the war. For example, a severe shortage of wiring harnesses for cars, of which Ukraine is a major supplier, is causing production delays. However, since manufacturers can shift to wiring harness suppliers in Eastern Europe and North Africa, we don’t expect these disruptions to persist more than a few weeks. Shares of European automakers and components suppliers are down by more than 16%, implying a much longer disruption and deeper sales slump than we think is likely.

Defensive Sectors Show Resilience

Some defensive sectors have performed better than the broader European market. The healthcare sector is down by 1.0% in the year through March 18, but has actually risen by 6.9% since the war began. Within the sector, the pharmaceuticals industry has performed well. In part, this is because drugmakers are allowed to continue selling products in Russia for humanitarian reasons, even under the sanctions that have prompted many European companies to leave the market.

The consumer staples sector has underperformed. Yet select food producers have held up relatively well, as their businesses are unlikely to be undermined by a slowdown. Utilities and real estate companies, which also tend to benefit from a rising rate environment, have fallen in the year to date but since the war began are down only slightly. Selective positioning in defensive pockets of the market can help cushion portfolios from some of the volatility.

Energy and Defense Companies Are Benefiting

Energy and defense companies have been beneficiaries of the turmoil. Even though European energy companies have been forced to withdraw from their Russian ventures, rising oil and gas prices are supporting share prices against a background of already high cash flows, which are largely being returned to shareholders. However, the impact on commodities isn’t uniform, and some companies that rely on Russian and Ukrainian imports of steel and other raw materials are suffering from disruptions.

Defense companies expect a huge boost in sales from Europe’s renewed commitment to bolstering its capabilities. For example, Germany’s commitment to double its 2022 defense budget to €100 billion will generate huge orders. Even as the defense impetus grows, we believe responsible investors must scrutinize companies to ensure that they aren’t producing prohibited munitions that kill indiscriminately or selling products to bad actors.

Investors watching the tragic events in Ukraine might conclude that European stock markets should be avoided for now. We believe that would be a mistake. While the war has indeed triggered extreme uncertainty and long-term changes for investors, it is also likely to lead to wide dispersions in sector, industry and company performance. By identifying companies with resilient business that are less exposed to the long-term threats, we believe a portfolio of European equities can be positioned to help investors traverse these tough times.

Andrew Birse is Portfolio Manager—European Value Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.