After a tumultuous 2022, investors are hoping for an eventual end to monetary tightening, and with it, a reprieve from brutal market volatility. But since corporate earnings are still adjusting to a new regime, the road will be bumpy. What can equity investors do to reduce risk?

Last year’s market volatility was driven primarily by uncertainty over inflation and interest rates. Federal Reserve Chair Jerome Powell hasn’t said when the Fed will stop raising interest rates, but he has signaled the Fed’s intention to moderate the pace of rate hikes in the months ahead.

Once we see a terminal fed funds rate, it’s full steam ahead for equities, right?

Not necessarily.

Ongoing Risks Could Upend Markets

Markets are still adjusting to the loss of the key stabilizing forces that dominated the pre-COVID era. This doesn’t necessarily spell a repeat of 2022, but in our view, investors would be well-served paying heed to potential catalysts for continued market volatility—ongoing inflation, rising interest rates and a maturing information technology sector that isn’t guaranteed to keep growing at a breakneck pace.

Let’s start with inflation.

Despite evidence that inflation is cooling, including lower prices at the gas pump and decelerating consumer prices, inflation is far from extinguished. The US Consumer Price Index rose 6.5% on a year-over-year basis in December—in line with expectations but not enough to assuage inflation concerns. The Fed’s preferred gauge of inflation, the PCE Price Index, also shows that price increases are moderating but persistent. In the euro area and the UK, consumer price inflation still exceeds an uncomfortably high 10%.

Even if we reach the end of the monetary tightening cycle in 2023, central banks around the world are still increasing rates at the fastest rate of the past couple of decades. In our view, the Fed is in the second phase of its tightening cycle, with a couple of 25-basis-point hikes still likely in 2023. When inflation eventually moderates, it will take time for companies and markets to adjust to the new reality of higher rates and slower economic growth. Investors should expect more volatility as this process plays out.

Tech Stocks Are No Longer Harbingers of Growth

In last year’s downturn, technology stocks were at the epicenter of market volatility. After years of steady gains, investors now acknowledge that technology stocks will not all grow forever. But we believe wholesale concerns about the sector are off the mark.

Twenty years ago, tech was marked by explosive growth but little in the way of maturity or profitability. Today, profitability has improved measurably alongside expansion within software, semiconductors and payment services.

Hypergrowth companies, which include many high-flying technology firms, surged during the pandemic but were shunned in the 2022 shakeout. The key driver of tech’s underperformance was a de-rating of companies that lacked profitability. In both 2020 and 2021, many growth-oriented tech companies that did not have a track record of profitability saw their stocks reach lofty valuations. As the market pivoted its focus from growth to profitability in 2022, these stocks came crashing back down to earth.

Profitable Tech Names Have Experienced Less Volatility

But many high-quality, profitable technology companies that operate behind the scenes don’t face the same risks as the consumer-facing giants. Often overlooked, for example, are lower-profile technology enablers and payment services firms that have sustainable business models and large, recurring revenue streams. While it might sound counterintuitive, we believe that select technology stocks with these attributes exhibit defensive characteristics, which can help buffer against spikes in market volatility.

Software is an interesting case study. Many high-profile software companies that were growing quickly but had no prospects for achieving intermediate-term profitability achieved incredibly lofty heights in 2021. As the market focused more on profitability last year, these stocks fell from grace in striking fashion. However, a number of stable, high-quality names that fell beneath the radar avoided this roller-coaster ride. It’s these types of companies that we believe can still compound at attractive rates, with less overall volatility.

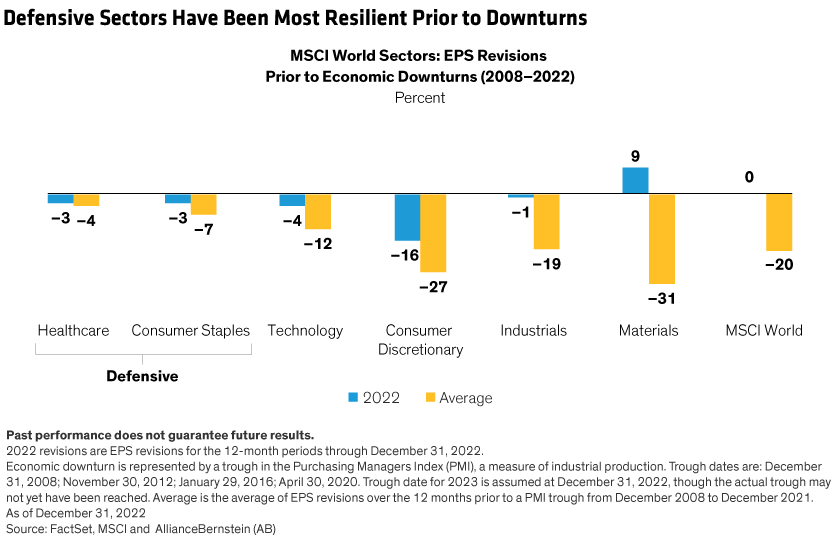

In addition, traditional defensive sectors such as healthcare and consumer staples have generally provided less earnings risk during economic downturns (Display).

Quality, Stability, Price: Keys to Navigating Uncertain Times

So how can investors identify stocks with the potential to weather bouts of market volatility? We believe that a disciplined, low-volatility approach to buying high-quality, stable companies at the right price (QSP) provides investors with multiple ways to mitigate risk while still participating in market gains.

First off, investors can take a bite out of inflation with quality. Quality companies with strong pricing power often demonstrate consistent profitability, even in inflationary environments. Firms like these are often seen in traditional defensive sectors, such as utilities and consumer staples.

Investors can also offset slowing growth with stability. Stable companies have cushion on the downside because they typically have lower beta—sensitivity to the broader market—than traditional growth firms. Fundamental research can unearth companies with hallmarks of stability across a broad array of sectors, including financials, energy and information technology.

Our research suggests that companies that rate high in both quality and stability have substantial cash and less debt on their balance sheets than even traditional defensive bulwarks. In fact, across 20 market downturns between January 1, 1970, and December 31, 2021, we found that S&P 500 stocks segregated into the highest quintile for QSP characteristics fared well during market downturns.

Quality on its own fared poorly in 2022, but quality coupled with stability performed better, while also mitigating risk. In the case of technology, this performance differential was particularly striking (Display). Low-volatility strategies that sought to balance risk and return through bottom-up stock selection across traditional defensives—as well as sectors such as technology, financials and energy—had more levers to pull to manage volatility.

Of course, pinpointing these high-quality, shock-resistant firms can be challenging. We believe that a high-conviction approach utilizing active management can help identify companies with hallmarks of quality and stability that are competitively priced because they aren’t fully appreciated by the market.

This framework for stock selection can help investors reduce losses in a downturn while participating in most of the upside during a recovery. Even if inflation and volatility remain elevated, smoother performance patterns can help embolden investors to stay invested in equities through downturns and position themselves for better long-term results.

Kent Hargis is Co-Chief Investment Officer—Strategic Core Equities at AllianceBernstein (AB)

Sammy Suzuki is Co-Chief Investment Officer—Strategic Core Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.