China’s currency, the renminbi (RMB), remains strong even though many of the factors that have driven its performance over the last two years have weakened. To understand the currency’s short-term outlook, investors need to unpick the nuanced dynamics now driving it.

As China exited the first wave of COVID-19 ahead of other countries, its stronger growth rates, higher interest rates and an export-led recovery saw demand for the RMB rise. Now that those support pillars have eroded, the currency’s recent strength has puzzled investors.

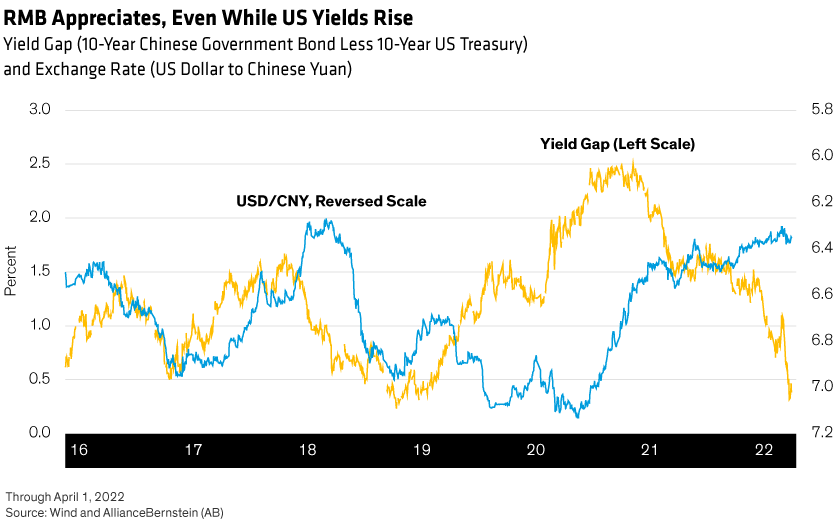

It’s persisted even as the difference between 10-year US Treasuries and Chinese government bonds has narrowed, with Treasury yields rising (making them more attractive to buyers) and Chinese yields falling.

For example, the “yield gap” between the US and China 10-year bonds has fallen from a record high of 2.5% in November 2020 to close to zero recently.

This fueled expectations that the RMB would weaken against the dollar on the basis that the “carry,” or additional yield available in China versus other markets, had disappeared. As China’s bonds would see reduced foreign investor demand, the RMB would see less support. Instead, however, the RMB appreciated against the USD, from CN¥6.6 to CN¥6.35 (Display).

Also puzzling is the fact that, despite being relatively closely correlated to the US dollar trade-weighted index historically, the RMB has sharply diverged from it recently. And the People’s Bank of China (PBOC)—which, in the past, intervened to moderate the RMB’s strength or weakness—has taken no strong action on this occasion.

Unravelling these puzzles is the key, in our view, to understanding the RMB’s short-term outlook.

Rate Differentials Have Limited Impact

In theory, it makes sense that interest-rate differentials—as measured by the yield gap between the Chinese and US bond markets—should have some impact on the USD-CNY exchange rate.

However, statistics show that the historical relationship between Chinese and US yield differentials and USD-CNY is not very strong compared to similar relationships elsewhere—a reflection, in part, of the fact that China is still among the least financially open economies in its per-capita income range.

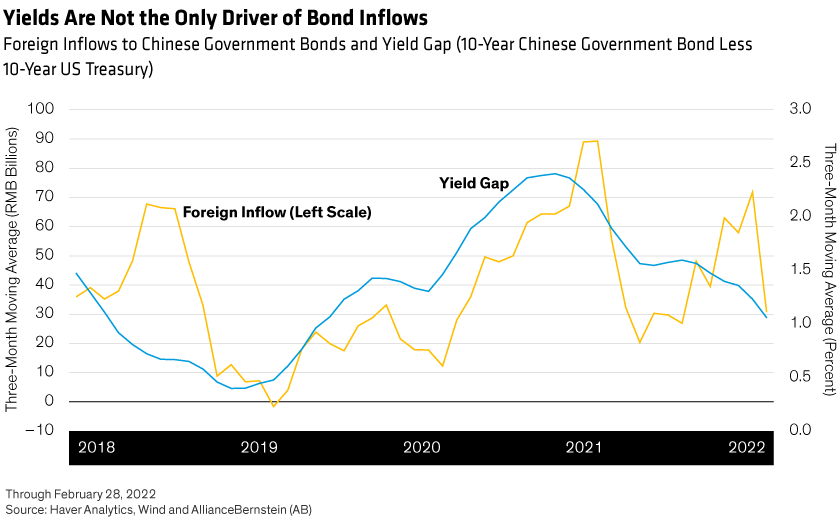

Similarly, there’s no clear-cut link between foreign fund inflows into the Chinese bond market and yield differentials. Inflows into Chinese bonds increased from April 2021 through year-end even while US yields, as shown by the narrowing yield gap, rose relative to Chinese yields (Display).

Clearly, factors unrelated to yield differentials helped to support the inflows. These would have included structural demand from foreign investors to allocate to RMB assets and demand for Chinese government bonds caused by their inclusion in the FTSE World Government Bond Index in November 2021.

Foreign inflows have dropped sharply since February 2022. While the yield differential might have been a factor, low net supply of Chinese government bonds and global market turmoil amid the Russia-Ukraine crisis are likely to have played a part, too.

Market Forces Dent USD-CNY Correlation

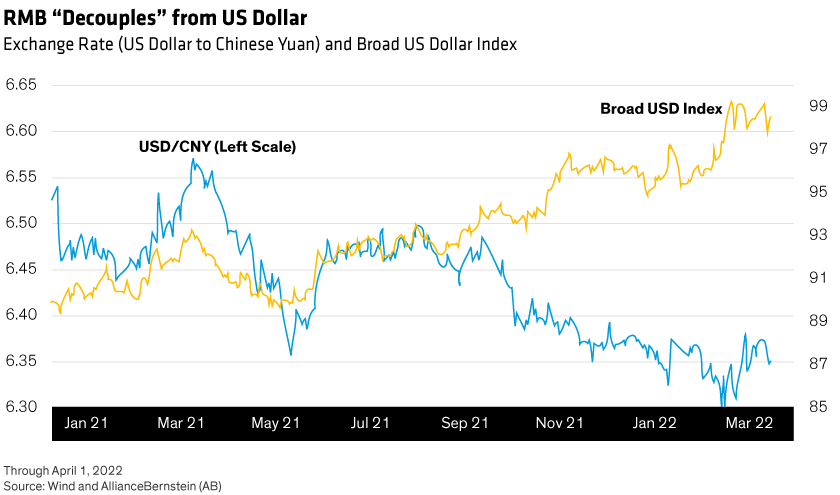

Currently there are two elements to the mechanism by which China establishes the daily USD-CNY “central parity”: market forces (which can be measured by comparing the spot closing rate with the previous day’s fixing), and the broad or trade-weighted US dollar index. The USD-CNY spot rate can move within a 2% band around the fixing.

Historically, the USD-CNY fixing and the USD index have been closely correlated. Recently, however, they have diverged (Display).

The divergence has been triggered largely by market forces, reflected in the fact that, in recent months, the USD-CNY closing rate has been consistently higher than the previous day’s fixing rate.

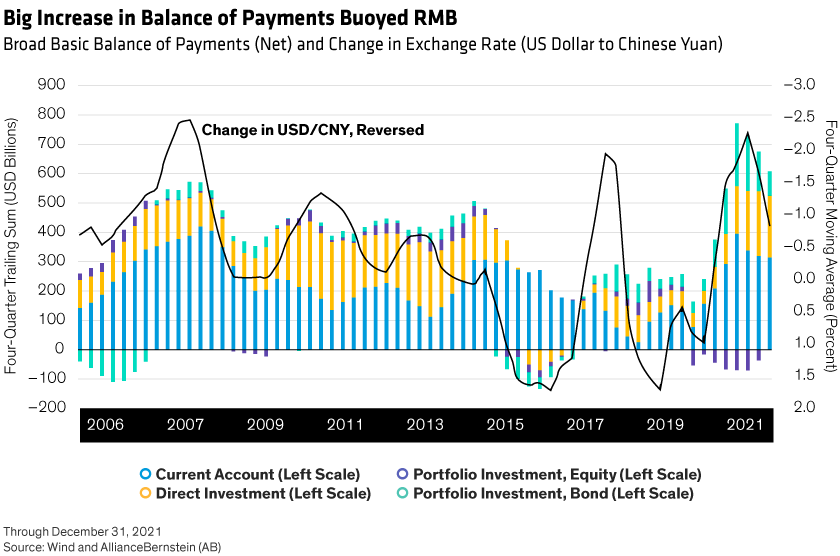

A major contributor has been the large trade surplus which, in fourth-quarter 2021, averaged US$84 billion a month and reached a monthly record of US$94 billion in December. The surplus has remained strong in early 2022, seasonally adjusted.

The impact runs across the broad basic balance of payments (BBOP), including the current account balance, net direct investments and net portfolio flows. While portfolio investment inflows have benefited from the opening of China’s bond and equity markets, the current account and direct investments remain more important. China’s current account surplus has increased notably in the last two years thanks to strong goods exports growth and a lower service trade deficit (Display).

Overall, a significant increase in the BBOP has been a major factor driving the RMB higher.

PBOC Favors Flexibility

In our view, the absence of PBOC intervention is less of a puzzle than it might appear. It’s been several years since the central bank took such action (for example, to defend the currency’s competitiveness in export markets), and it has explicitly disavowed plans to do so again.

The PBOC significantly increased the RMB’s flexibility in recent years, as a response to more volatile capital flows and to increase the independence of monetary policy. Partly because of this, CNY has been increasingly driven by market forces.

The PBOC does care about USD-CNY—but, rather than changing its direction or defending a “magic level,” the central bank is more concerned about the potential accumulation of pro-cyclical and speculative factors in the market, which could happen when the pace of appreciation or depreciation is too fast.

Importantly, direct intervention through foreign-exchange reserves has been sharply reduced, and the PBOC has preferred indirect policy tools such as macroprudential measures to curb the currency’s excesses.

All Things Considered, Stability Is Likely

Against this background, what is the short-term outlook for the RMB?

While all the above factors play a role, the most important, based on our research, is the BBOP. The current account surplus is likely to moderate this year, but we expect it to remain positive and significant. Foreign direct investment (FDI) inflows have trended upwards since 2015, despite a slowdown during the 2018–2019 trade war, and FDI data early this year together with industry surveys suggest they should remain steady.

Bond inflows could come under pressure from the geopolitical crisis and narrowing rate differentials, but the index-inclusion effect and potential increase in reserve allocation towards Chinese government bonds could help support flows. Equity inflows could benefit now that the government—following the equity market sell-off caused by macro policy uncertainties and the significant northbound equity outflow in early March—aims to improve communication with markets, policy coordination and transparency.

These factors, together with an expected improvement in growth fundamentals in coming quarters, should be positive for RMB.

Regarding yield differentials, while the 10-year US Treasury yield could rise further in coming months, we expect the comparable Chinese government bond yield to rise too, limiting scope for the yield gap to narrow further. Although narrower rate differentials could put some pressure on CNY, it is unlikely, in our view, to dominate its direction.

Taking all these factors into account, we expect the RMB to be broadly range-bound and stable against the US dollar in the short term.

Brad Gibson is Co-Head of Asia Pacific Fixed Income at AllianceBernstein (AB).

1 CN¥ = Chinese yuan, the unit of account of the RMB currency.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.