CCC-rated residential mortgage-backed securities (RMBS) and CCC-rated corporate bonds have captured investors’ attention in recent years. But why do we think one is investment worthy, while arguing that the other should largely be avoided?

To put it bluntly, other than the CCC label, lower-rated corporates and mortgage-backed securities don’t have much in common.

As we’ve discussed before, it usually makes sense to stay away from CCC corporate bonds. Although their yields may look compelling in today’s low-yield environment, our main reason for concern is credit risk—the probability of default. Once a bond slips into default, it becomes difficult to recoup the money you’ve invested.

On the other hand, non-agency RMBS are made up of home loans pooled together and packaged into investments not guaranteed by the US government (unlike their agency mortgage-backed security brethren). Prior to 2008, non-agency RMBS had very high (AAA) credit ratings. But following the housing bust, all mortgage-backed securities took a hit. This drove prices to distressed levels and lowered ratings—in most cases into CCC territory.

The Case for CCC Mortgage-Backed Securities

Unlike for corporate bonds, credit ratings are not as relevant to distressed-level RMBS, so the “CCC” label is a bit of misnomer. That’s because ratings communicate the probability that a bond won’t repay investors at par, or face value. But since RMBS already trade at very low prices—well below face value—the bigger concern isn’t the rating, but getting your initial investment back.

For example, if an investor is considering buying a CCC-rated MBS at the significantly reduced price of $75 (par is $100), it’s important to first analyze how resilient the bond is and the chances of getting back the initial $75 under different economic scenarios. Our research shows that the likelihood investors will get back their original investment in RMBS is more akin to that of a security rated BBB or BB. Receiving the entire par amount of $100 represents upside potential.

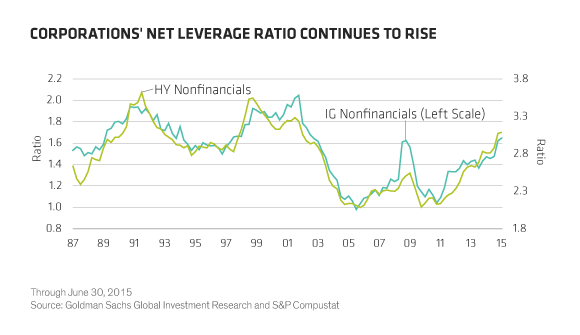

Another point to consider is leverage. Corporate leverage has continued to climb over the past decade (Display 1).

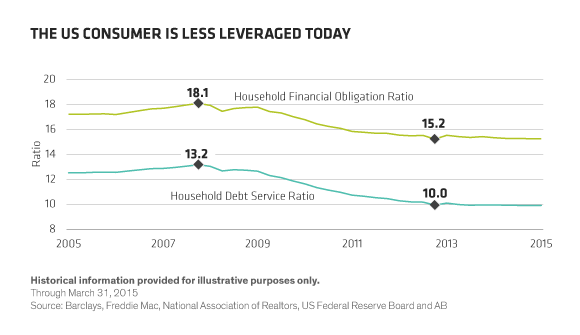

On the other hand, US homeowners and consumers are not as bogged down by debt as they were prior to the housing crisis, and are now dramatically less leveraged (Display 2).

This means that the underlying loans that comprise RMBS today are derived from more creditworthy consumers than in the past, making defaults less likely. Other credit measurements, such as average FICO score and borrower debt-to-income ratio, are at their best levels since 2006—indicating that now is a good time to invest in RMBS.

When considering CCC bonds, it’s important to choose carefully, and remember that all investments are not created equal. The CCC rating is not an accurate reflection of non-agency RMBS, and the chances of losing money are significantly lower than they were before the housing crisis. These characteristics alone make CCC-rated RMBS worth a closer look.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.