The US stock market continues to hit new highs this month, buoyed by optimism that the Fed will resume monetary policy accommodation—by lowering interest rates—which should further support the economy and corporate profitability. Despite this, investors are still fixated on the duration of the current bull market—now over 10 years. The implication of these concerns is that the rally’s duration is reason enough to become more cautious. We disagree.

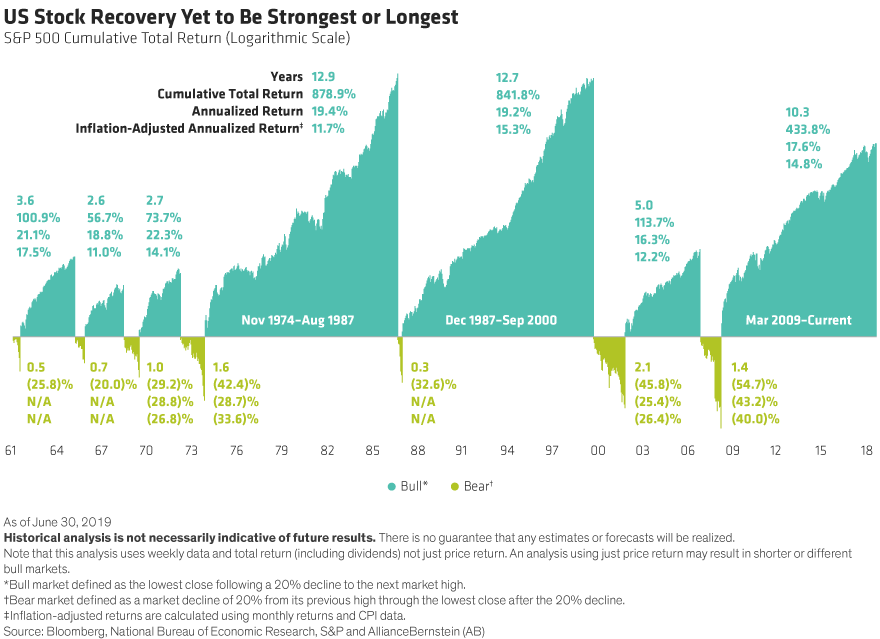

There is fundamental support for the strength in the equity market—relatively loose financial conditions and reasonable global valuations are just two factors—but there’s also precedent that a bull market can continue for extended periods if conditions are supportive. Consider the following chart:

This chart shows the seven bull markets since 1961. What’s notable is that the current bull market is neither the strongest nor the longest. The two markets that cover the period from 1974–2000 (with “Black Monday” of 1987 in between) produced bull runs in excess of 12 years each and annualized returns of better than 19%. In contrast, the rally that began at the end of the Global Financial Crisis in 2009 is only in year 11, with returns at 17.6%. We highlight these specifics to substantiate a point: Expansions (and bull markets) don’t simply die of old age, something kills them.

What could kill this bull market? We have our eye on several risks, including a tariff-related slowdown in global trade, but none strike us as overly worrisome at this time particularly given the Fed’s commitment to sustain economic growth through accommodative monetary policy.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.