The recent stall-out in US bond yields has thrown equity investors into a funk. But, in our view, it’s a pause that refreshes. Remember, there are still powerfully supportive forces in play for the economy and stocks.

The eight-year bull market in equities owes much to the bunker mentality that has kept interest rates at some of the lowest levels ever. With every shock, investors ran for cover and loaded up on low-risk bonds. That has been wildly bullish for stocks. It not only allowed companies to borrow at superlow rates, but it also increased the relative attractiveness of dividend and earnings yields of stocks versus bonds. And though US growth has been disappointingly slow, it has been steady—and that has done a lot to heal the wounds of the crisis.

Turning Point

Enter 2017. Today, investors are pinning their hopes on faster economic growth and the higher rates that come with it. We don’t rely on such forecasts, but we didn’t dispute the consensus view that rates would head higher as reflationary forces driven by a stronger economy and pro-growth government policy proposals took hold. After all, the economy was still creating jobs and growing. Business conditions were quite strong, and the Republican sweep in November made the imminent passage of a big corporate tax cut more probable.

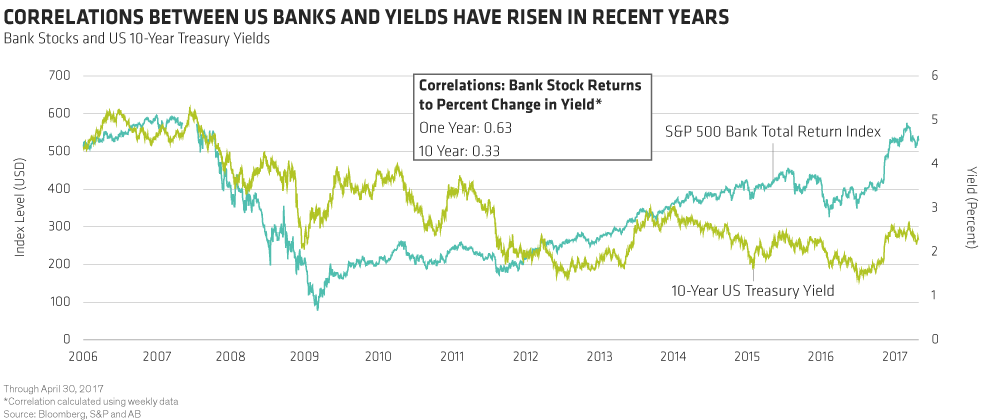

Indeed, the so-called reflation trade ran its course through February, when the 10-year US Treasury bond yield reached a high of 2.63%. But then everything changed. Some economic trends eased, commodity prices rolled over and dysfunction rather than bold action emanated from Washington, causing the 10-year yield to fall to 2.17%. Postelection laggards—notably quality growth and higher-yielding stocks—regained favor. Cyclical stocks that benefited from the Trump bump, including financials, corrected sharply. Bank stocks were especially hard hit, despite the US Federal Reserve’s official rate hike in March (Display).

A Step Too Far

In our view, the market’s obsession with low rates has gone too far. How many times have you heard over the past two months that a flat yield curve is bad for banks? We’ve heard it a lot. But we did some research—and the reality is more nuanced.

Yes, banks do best when the yield curve is steepening, all else being equal. But banks don’t “fund short and lend long” to benefit from the gap between short- and long-term interest rates, like the savings and loan institutions did long ago. Now, they’re more likely to fund short and lend short (via floating rates). What’s more, fees account for a large portion of bank business today and are unaffected by the shape of the yield curve.

But don’t take our word for it. Look what’s happened this year: despite the significant flattening in the yield curve, bank earnings forecasts are on the rise. Earnings estimates for the S&P 500 Bank Total Return Index have climbed about 3% year to date, yet the stocks have barely moved. After these revisions, forecasts for this group call for year-over-year earnings growth of nearly 15% in 2017.

Estimates up, stock prices flat to down—that’s usually a good time to buy. But there is one more thing to remember when bank stocks are following rates lower: bank stocks are still stocks. Lower rates make dividends and earnings more valuable. This is particularly good news for banks with the business momentum and balance-sheet strength to support generous and sustainable dividend growth.

Interest rates have pulled back sharply after rising in the second half of 2016. But strip out the political noise and take comfort from the continued strength in underlying business conditions. We still believe that long-term rates will head gradually higher. In the meantime, take a closer look at stocks, particularly those that have pulled back while fundamentals stay strong.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.