It’s been two years since our initial research on populism, and populist-inspired policies continue to advance today on multiple fronts. As we see it, investors should expect more of the same ahead—influencing everything from global economic growth and inflation to policies directed specifically at the corporate sector.

Populism has turned out to be more deeply rooted than mere residual anger from the global financial crisis of 2008–2009—or the handling of the European sovereign crisis. Economies have recovered further over the past couple of years, but politics and policy haven’t returned to “normal.” In our view, investors should think of populism as a lasting structural theme—driven by rising inequality, stagnant incomes, fears of disruption and a sense that the political system isn’t delivering.

Disillusionment Continues to Grow

Populists now rule in Italy, which isn’t surprising given the country’s poor economic performance under the European Monetary Union. But even in Germany, recent state electoral results show more deterioration of the political center in favor of both the left and the right.

The erosion of the center is picking up across emerging countries, too, with populists recently elected to lead Latin America’s two biggest economies. Andrés Manuel López Obrador, from the left side of the political spectrum, was elected in Mexico last July; from the right, it was Brazil’s Jair Bolsonaro in October. The Brexit saga continues to roll on, and US midterm elections fell short of the “blue wave” revolt that some expected.

All in all, it seems safe to say that concerns about what populism might bring next are only intensifying.

Assessing Advances in Policy Channels

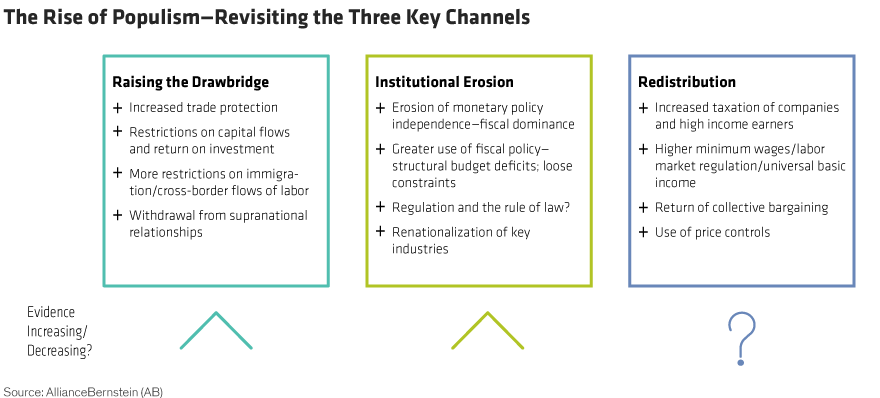

How effectively have these political forces translated into tangible actions? When we revisit the framework from our original research, we find that populism has continued to move forward—but to different degrees in each of three key channels (Display).

1) Raising the drawbridge. We’ve seen plenty of evidence of advances in this channel, with policies becoming more national and less global. There’s been trade conflict between the US and its partners, including China, Canada and Mexico. We’ve seen withdrawals from multinational arrangements, such as the Trans-Pacific Partnership and the Paris Agreement. Brexit and anti-Brussels sentiment fit the mold, too.

2) Institutional erosion. There have been many examples of efforts to undermine or ignore mainstream institutions. In the last couple of years, these included attacks on media independence, from complaints about “fake news” to the closing or limiting of media outlets in Hungary and Turkey. Fiscal policy constraints are being ignored, too—notably in the US, but also in Europe, by way of Italy’s budget proposals.

The days of independent central banks show some signs of being numbered, from criticism of the US Fed to Turkish president Recep Tayyip Erdoğan’s statement that his patience on central bank policy “has limits.” The dispute between India’s Prime Minister Narendra Modi and former governor Urjit Patel—leading ultimately to Patel’s resignation—over the Reserve Bank of India’s independence is yet another example.

3) Redistribution. From the standpoint of income redistribution, the evidence of policy action has been scarcer. National income has been shifting away from labor for some time in industrialized countries, but this trend has largely flown under the radar so far. Globalization, technological disruption and institutional change have squeezed living standards for workers at the middle to bottom end of income distribution while bolstering corporate profits.

But the corporate sector hasn’t been a lightning rod for populist anger to this point. We’ve seen some efforts to raise minimum wages—South Korean president Moon Jae-in’s minimum-wage hikes of 16% in 2018 and 10% in 2019, for example. But we haven’t seen broader efforts to shift the balance of bargaining power from capital back toward labor—at least not yet.

But corporations might be next on the agenda. This could mean rethinking antitrust policies, addressing the notion that competitive dominance also means political power and more influence on public policy. Efforts to shift power back toward labor could find their way into policymakers’ hands. The UK Labour Party’s manifesto outlines some of the possibilities, including shorter workweeks, mandatory employee presence on boards and a bigger role for unions in collective bargaining.

Assessing the Big-Picture Impact

The populist surge is already shifting the global macroeconomic outlook. For some time, we’ve been emphasizing the ramifications of these policies in influencing the medium-term inflation path, but there are near-term consequences, too.

For example, the Trump administration’s fiscal-spending boost is putting upward pressure on US interest rates. The ongoing US-China trade dispute is muddying China’s growth prospects. Tangled Brexit negotiations and uncertainty about Italy’s politics cast a shadow on Europe’s economic outlook.

The bottom line, in our view, is that we shouldn’t expect a return to the policymaking orthodoxy of the decades that led up to the global financial crisis. We’re likely to see more populist-inspired initiatives through the three main channels.

Together, these policies are likely to shift potential macro outcomes in a more challenging direction. Even if nominal income growth were to stay the same, the mix would surely change, and we would see higher inflation, lower economic growth rates and more pressure on corporate profit margins.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.