Growing fears about the coronavirus have hit Chinese stocks. While markets will remain unstable until China gets the outbreak under control, equity investors should revisit lessons from previous epidemics and consider the potential longer-term effects of the current crisis.

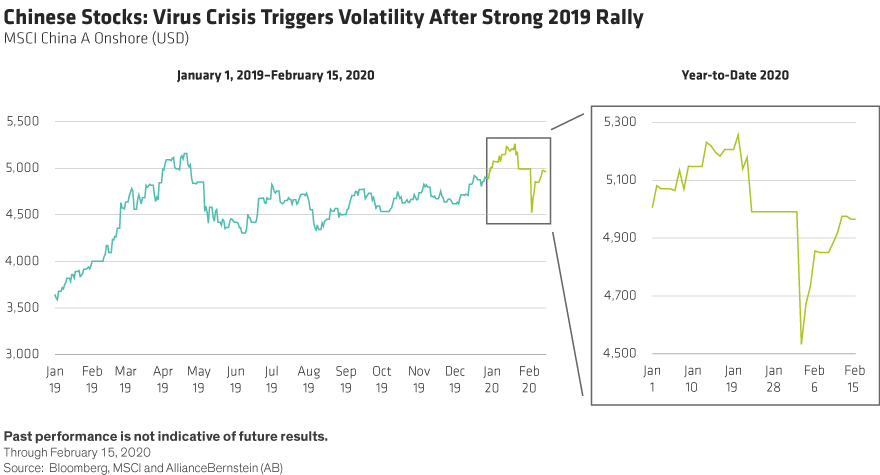

As the death toll rose and global infections spread, investors’ reaction to the coronavirus intensified. The MSCI China A Onshore Index tumbled by 9.2% on February 3 in US-dollar terms, but rebounded over the next two weeks to recover most of the losses by February 15. (Display). The recent volatility followed a 2019 rally in which Chinese stocks surged by more than 37%. Investors fear that the lockdown of millions of people could inflict a big blow on China’s economy that might also affect global growth. Yet they’ve also been reassured by rapid Chinese government stimulus to offset the potential damage.

Market Rebounds Are Often Quick

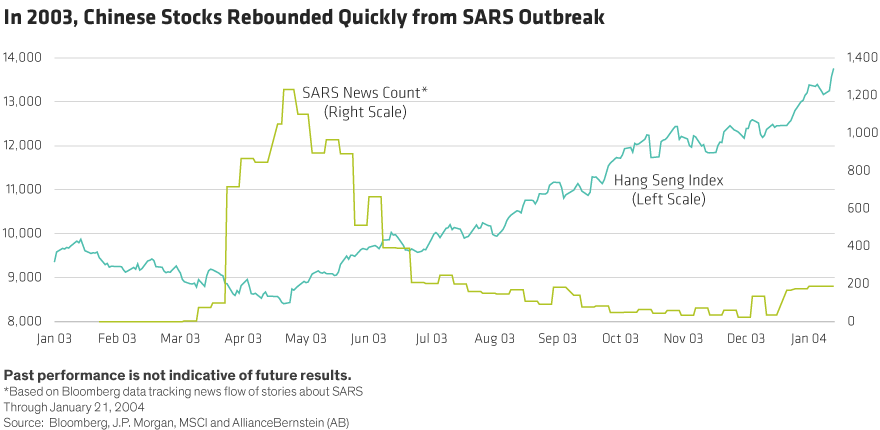

These concerns are understandable. However, in similar past episodes, market corrections were relatively brief and comparatively shallow. For example, during the severe acute respiratory syndrome (SARS) epidemic in 2003, the Hang Seng Index dropped by about 7.7% from March 5 through April 25, when new infections were increasing, but recovered quickly when the situation improved (Display). Similar market patterns have played out in previous epidemics and pandemics. In each case, market sentiment shifted from initial panic to bargain-hunting when investors gained confidence that the disease had come under control.

For now, there’s no such certainty about the coronavirus. As a result, the volatility we’ve seen will probably persist until some tangible good news is received. But investors should also remember that the snap back from panic to positive momentum can be quick—especially in China’s markets, which are dominated by retail investors.

Varied Effects on Production and Consumption

Even without clarity on the virus, the potential macroeconomic effects can be assessed. Efforts to stem the spread of the virus by confining people to homes and imposing a quarantine on entire cities will, of course, have a real impact on the economy, via production and consumption.

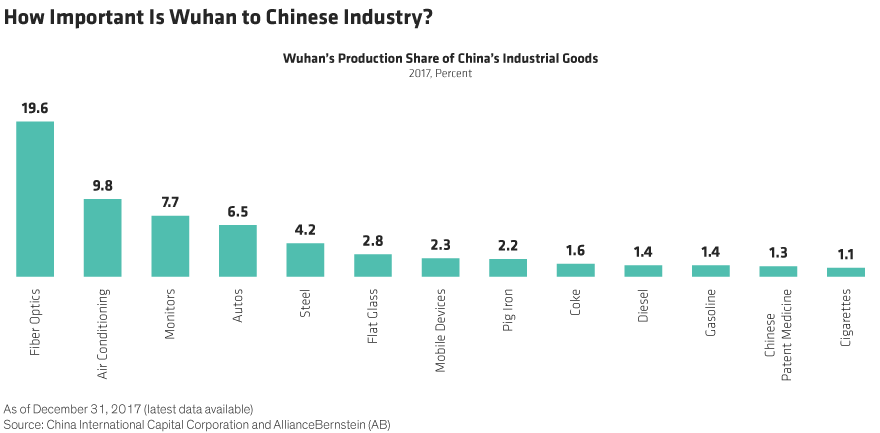

Over the last two decades, China has become the world’s factory, supplying goods and raw materials to many industries. Factory shutdowns are likely to result in varying degrees of supply disruption. For example, Wuhan—the epicenter of the coronavirus—is a manufacturing hub for telecom equipment, from fiber optic cables (Display) to printed circuit boards (PCBs). Production of these components may be impacted, which would have broader implications for technology supply chains, both in China and potentially globally, if the disruptions persist.

Wuhan is also the headquarters for a few large industrial companies, including one of the largest automakers in China. At these companies, production will undoubtedly be curtailed until the outbreak comes under control and the factories can resume normal operations.

Declining consumption will hurt retailers—especially those with predominantly brick-and-mortar stores. However,

e-commerce companies may weather the storm well, as consumers shift demand to online retail vendors. Some of China’s online supermarkets and food delivery services have already reported increased usage as shoppers stay away from stores. Investors will need to monitor how different industries and companies will be affected in different ways by fallout from the coronavirus crisis.

Will the Virus Lead to Longer-Term Changes?

During an endless news cycle of unfolding dramatic events, it’s hard to think past the immediate crisis. However, we think that the current events could potentially trigger longer-term structural changes that will affect companies and industries. Indeed, the 2003 SARS epidemic probably helped push the adoption of e-commerce in China and in Asia overall.

What might happen after the coronavirus? Right now, we’re in the midst of the largest-ever experiment of working from home in China and large parts of Asia. Tens of millions of Chinese students are being forced into online learning as schools shut down for extended periods. These experiences could trigger fundamental changes in how people work and how lessons are taught in the education system. If this happens, could we see a decade of growth in the adoption of remote working and learning products? How would the infrastructure for communications networks and data centers change to accommodate higher demand? Questions like these are hard to consider now, but when the immediate danger subsides, they will become more relevant for investors.

As long as the coronavirus situation remains unresolved, we think investors in China should reduce exposure to companies that are directly affected, including in the leisure and travel industries. At the same time, based on experience, a Chinese portfolio should be positioned for the long term and prepared for the possibility of a sharp recovery when the crisis is resolved.

John Lin is Portfolio Manager of China Equities at AllianceBernstein (AB).

Stuart Rae is Chief Investment Officer of Asia-Pacific Value Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.