After an extraordinary year in global markets, positioning equity allocations for 2021 looks challenging. But given the market distortions created during 2020, we think investors can find ways to broaden exposures with confidence despite uncertainties about the recovery.

Global stocks rose during 2020, fueled by massive monetary policy efforts from central banks and fiscal policy support aimed at preventing a total economic collapse under the coronavirus pandemic. Even as COVID-19 upended lives and businesses around the world, the MSCI World rose by 13.5% in local-currency terms (Display, left), leaving the first-quarter market crash a distant memory. US stocks led gains in major developed markets, while European and Japanese stocks underperformed. Emerging markets did well, powered by Chinese stocks.

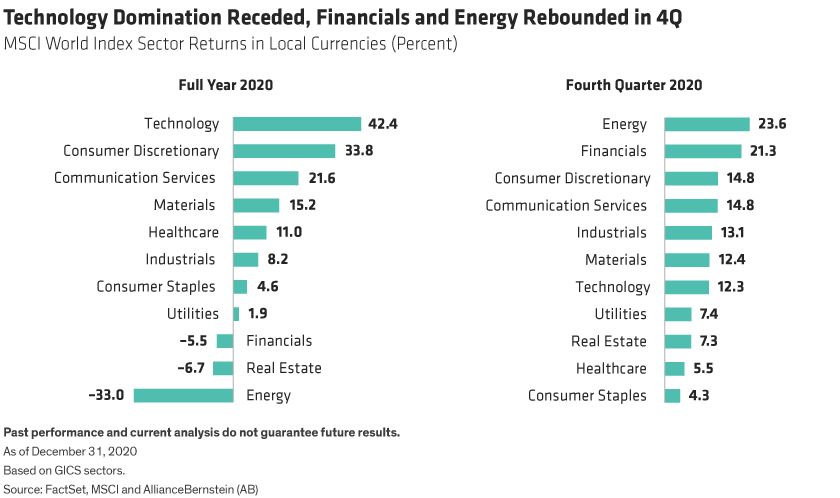

Sector and style performance for the full year reflected the pandemic’s impact (Display, below). Technology stocks surged, driven by mushrooming demand and accelerated technological disruption in a socially distanced world. Energy shares plunged as oil prices slumped. Sectors that were traditionally considered defensive, such as utilities and real estate, were weak.

Investors flocked to high-growth names such as Facebook, Amazon.com and Google (the FAANGs), partly because growth elsewhere was so scarce. Meanwhile, in other industries such as retail and leisure, traditional business models were upended, and companies that failed to adapt may be permanently impaired.

These developments—combined with ultralow rates that tend to favor growth-oriented stocks—fueled unprecedented market concentration. By year-end, the five largest US mega-cap stocks accounted for about 36% of the Russell 1000 Growth Index. Similar trends were observed in China. Investor portfolios that weren’t heavily invested in the largest names underperformed the market in 2020.

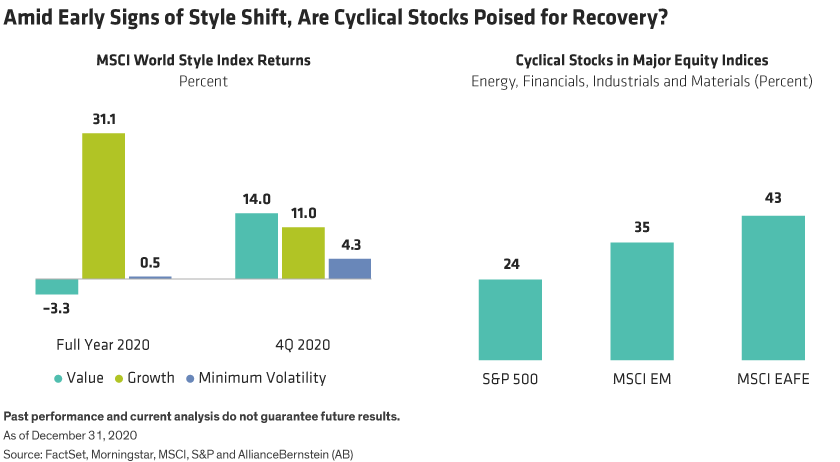

For most of the year, growth stocks outperformed value by a wide margin (Display, below left). Minimum volatility stocks were surprisingly weak, leaving traditional defensive stocks attractively valued at a time of continued uncertainty.

Late-Year Optimism Prompts Shift in Sentiment

Toward the end of 2020, things started to change. Even as the virus continued to inflict a terrible human toll, news of COVID-19 vaccine successes persuaded investors that the pandemic might end during 2021. As a result, since November, value stocks rallied, driven by hopes of a broader recovery of GDP growth. Shares of energy companies, banks and smaller companies in general, rebounded sharply.

Fourth-quarter return patterns were markedly different from the rest of the year. While it’s too soon to say whether these trends will persist, market moves since November serve as an important reminder that reversals in equity return patterns can be swift across styles, sectors, stock size and regions. Investors should not be complacent.

Three Phases of the Post-Pandemic Recovery

So how should investors think about positioning for 2021? Start by mapping out a possible course for the potential macroeconomic recovery, which will shape market trends. We see the recovery unfolding in three phases.

Phase 1 will be characterized by a tussle between two conflicting developments. During the next few months, investors will be challenged to balance encouraging news about vaccines and their potential to spur recovery, against difficult news as the virus continues to spread—and mutate—through a tough winter in the Northern Hemisphere, further damaging economies.

In phase 2, as the global rollout of vaccines starts to contain the pandemic and consumers unleash pent-up spending, we think many companies should enjoy a strong recovery in earnings growth, especially given the low level of comparable profits in 2020.

Phase 3 could see a post-pandemic hangover as companies struggle to keep up the accelerated pace of recovery in 2021 and GDP growth around the world faces the same headwinds that prevailed before COVID-19.

Throughout the stages of this recovery, there are many risks to consider. The pace at which the world will move through these phases will depend critically on how quickly the vaccine curbs the spread of the virus, which will vary by country. If a pickup in economic activity prompts investors to worry about possible inflation, market interest rates may rise from current historic lows, which could trigger volatility. And longer-term economic growth remains uncertain with the global economy still facing many obstacles, including populism, rising geopolitical tension between China and the West, and elevated debt.

We believe recent market gains may reflect optimism for 2021, and strong earnings growth may already be priced into shares in many cases. Yet elevated valuations might not fully reflect the longer-term challenges that economies and companies will face in a post-COVID-19 world.

Global Perspectives on Elevated Valuations

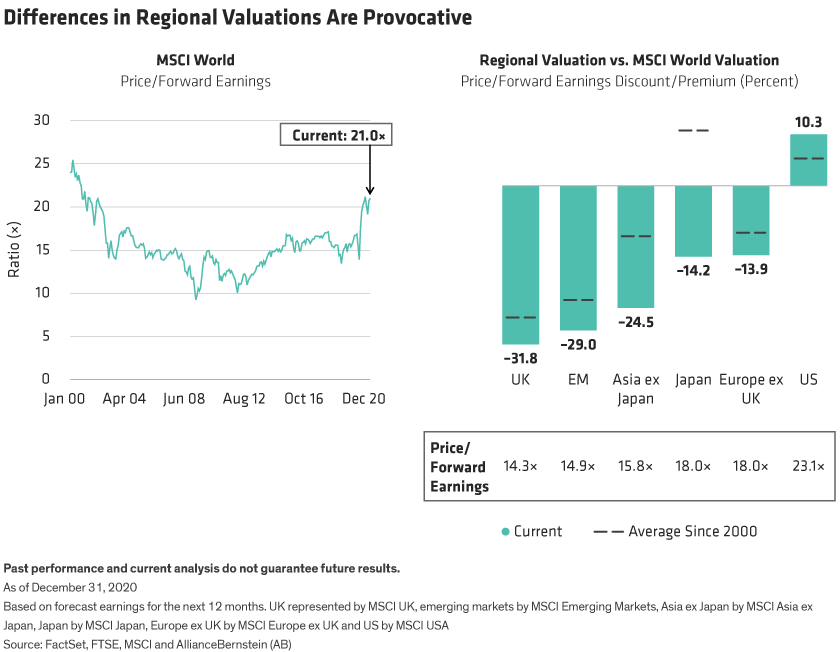

A broadening recovery could favor non-US markets, where companies that are especially sensitive to macroeconomic growth make up a greater proportion of key equity benchmarks (Display, above right).

By the end of 2020, differences in regional valuations were provocative, with US stocks relatively expensive versus the MSCI World’s price/forward earnings of 21.0x. Markets in Europe and Asia traded at bigger discounts than usual to global stocks (Display, below). Non-US stocks, particularly those in emerging markets, should also benefit if the US dollar continues to weaken.

Applying Investing Principles in an Uncertain Recovery

Despite the uncertainty about the outlook, we think many principles of long-term equity investing have been reinforced by the crisis. These should serve investors well in preparing for the next stages of recovery.

First, trying to time the market is unwise. As the first signs of coronavirus came from China at the end of 2019, few predicted a global pandemic or the ensuing market crash. Yet even for investors who correctly anticipated the sharp downturn that began on February 19, getting out of the market was only half the story. It was perhaps even harder to predict the March 23 inflection point, when markets started to recover in defiance of macroeconomic despair. For investors to win by timing the markets requires getting out, and back in, at exactly the right time—a nearly impossible task.

Second, investors shouldn’t try to outsmart the market on issues for which no real insight is available. For example, when dozens of drug companies are racing for a COVID-19 vaccine, building an investment thesis on a potential winner is a highly speculative strategy, while focusing on underlying business fundamentals of pharmaceutical groups makes much more sense.

Third, beware of following crowds to stocks that have done well recently. Until at least early November, momentum was an especially strong-performing equity factor across markets in 2020. But momentum is also extremely volatile. Based on historical trends, riding a momentum wave potentially sets up investors for a painful crash if trends revert to normal, in our view. Indeed, in the fourth quarter, global stocks with the highest momentum underperformed significantly.

Finally, fundamentals still matter. Yes, markets were supported in 2020 by enormous central bank liquidity, but ultimately, the stocks that led the pack were those seen to have better earnings prospects, even in an unstable and unfamiliar world. Selective investors will find huge differences across sectors and within industries between companies that have sustainable business models, cash flows and earnings, and others that don’t.

Revisiting Equity Exposures for a Changing Environment

Looking back on 2020, some equity investors might conclude that US mega-cap recent winners are the only place to be. We think that’s a simplistic conclusion. While the FAANG companies have strong businesses and earnings prospects, investors should closely assess portfolio exposures to make sure their allocations have the right balance of risks, in our view.

Don’t ignore value stocks because of past performance, and don’t steer clear of underperforming regions or sectors. Some companies that have been laggards will rise above the pack as they assert their fundamental strengths in a recovery and amid changing market conditions. For example, if interest rates rise, companies like financials would be expected to do much better.

Make sure growth exposures aren’t overly tilted toward expensive or crowded positions that can reverse quickly. Consider new types of defensive stocks that can help cushion volatility, even if traditional minimum volatility names don’t do the job.

Although elevated market valuations could limit medium-term returns, we believe stocks still offer attractive long-term potential when compared with bonds. And in a world of widely dispersed earnings expectations and uncertainty, we believe investors can achieve better outcomes with equity allocations based on a broad range of carefully selected companies that are suited to the recovery and the post-COVID-19 environment.

Christopher Hogbin is Head of Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.