Recent news about the efficacy of potential COVID-19 vaccines sparked a sudden shift in equity market leadership in November. While it’s too soon to say whether these trends will persist, investors should examine the balance of their equity exposures for resilience to a potential change in return patterns.

Pfizer’s announcement on November 9 that its vaccine candidate has 90% efficacy based on clinical trials raised expectations that the virus could soon be brought under control. Just a few days later, Moderna announced encouraging results in trials for another vaccine candidate. Although a difficult winter lies ahead, with case numbers and hospitalizations rising in many places, the vaccine news has given investors confidence that worst-case economic outcomes are now unlikely and that a broad economic recovery is possible in 2021.

Vaccine Hopes Awaken Equity Laggards

The news itself may not be enough to sustain the recent broad equity rally. But it has led to a dramatic shift in market leadership, with stocks that led the market for most of the year underperforming, and those that had lagged rebounding. On some measures, the day of Pfizer’s news release saw the most abrupt momentum reversal in more than a decade.

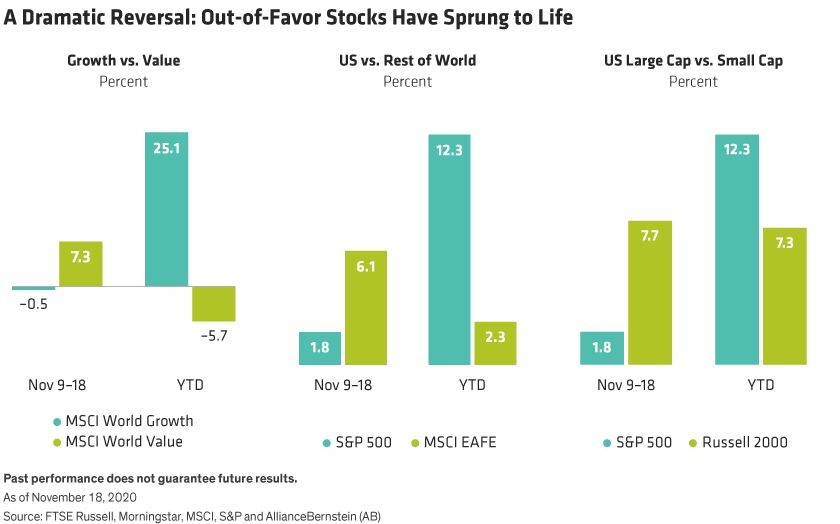

Since November 9, this shift has unfolded in several parts of the market. Small-cap stocks outperformed larger peers. Non-US stocks outperformed US stocks. Out-of-favor sectors, notably financials and energy, have outperformed technology, the sector leader for much of this year. And the MSCI World Value Index rose by 7.3% this month, as of November 18, in US-dollar terms, outperforming the MSCI World Growth Index by a wide margin. That’s a stark contrast to performance patterns since the beginning of the year; value stocks have fallen by 5.7% in 2020, while the technology-heavy growth index has surged by 25.1% (Display).

Will these trends persist? After all, it’s not the first time style leadership has shifted this year. Earlier episodes in the spring and in September, though less dramatic, quickly reversed. It’s too soon to say for sure, but the vaccine news may well prolong a switch into stocks that are more sensitive to economic growth, a trend which started in the third quarter. Conversely, mega-cap US technology and consumer companies, which benefited from the effects of global lockdowns, might look less attractive in relative terms if economic life is likely to return to normal sooner rather than later. This has significant implications for the performance of different sectors and regions, as well as for different style factors.

Were Market Imbalances Ripe for Reversal?

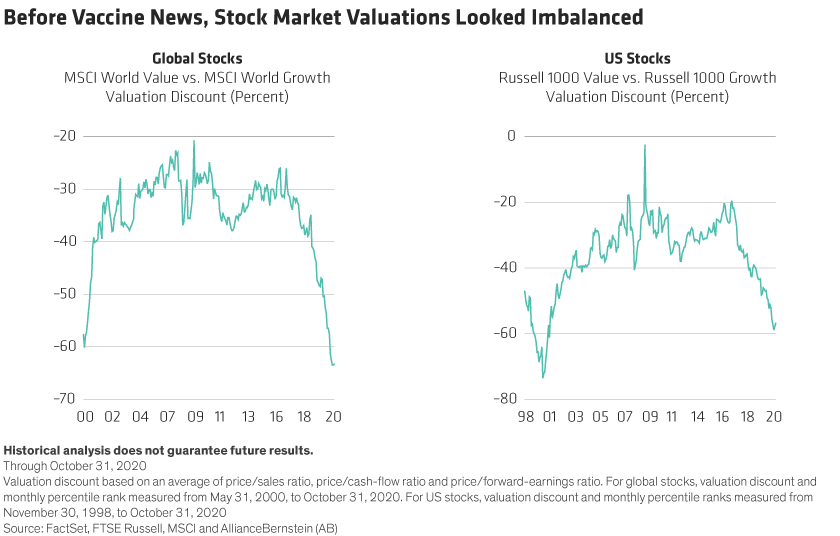

Before the recent shift, equity return patterns had created big imbalances in markets. In style terms, for example, by the end of October, the MSCI World Value was 63% cheaper than the MSCI World Growth, based on a combination of three value metrics: price/sales, price/cash flow and price/forward earnings (Display, left). That’s the deepest discount in 20 years. In the US, the Russell 1000 Value Index traded at a 57% discount to its growth counterpart (Display, right)—also close to historical low levels.

Inflation and Interest Rates Shape Stock Return Patterns

Specifically, many investors are now asking: Should I sell growth stocks and buy value? If global growth accelerates, we believe many cheaper, more cyclical companies—which are more typically held by value portfolios—are likely to see better earnings growth in 2021. And if growth is more abundant, investors may be less willing to pay a premium for higher-growth stocks, such as those that performed well in 2020 during COVID-19.

In an economic recovery, inflation could also rise, which would put upward pressure on interest rates. Rising rates usually benefit value stocks and act as a restraint on growth stocks, where more of the company’s value is derived from cash flows many years in the future. AB’s economists expect the 10-year US Treasury yield to rise modestly from its current level of less than 0.90%. However, after a decade of ultralow rates, investors should be cautious about building a strategy on a lasting change in interest-rate levels.

Time to Check Equity Allocations

Whether or not the value rally has legs, recent return patterns may have helped expose an imbalance in your allocation. Most investors know the benefits of diversification and rebalancing, but it can be hard to put theory into action after a prolonged period of one-sided performance.

Recent performance should prompt investors to take a close look at their equity allocations, in our view. Ask what risks your current positioning might entail. Do you hold enough assets that should perform well in an accelerating economic recovery or if interest rates start to rise? Are your geographical exposures sufficiently diversified? Is your growth equity exposure too concentrated in richly valued giant stocks, or spread out among a broader array of companies with distinctive growth drivers?

The answer to these questions will of course vary by every investor’s risk appetite and financial goals. But when style winds change as dramatically as they have this month, it would be remiss for investors not to check whether their sails are set right for more potential changes to come.

Christopher Hogbin is Head of Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein