Investors often reduce allocations to corporate bonds—particularly those on the lower rungs of the ratings ladder—when the economic outlook gets cloudy. And there have been plenty of clouds on the US and eurozone horizons, including inflation, rapidly rising interest rates, and lingering concerns about midsize and regional banks.

That doesn’t mean investors should be shying away from corporate credit, in our view. Slower economic growth is unlikely to result in wholesale deterioration of credit conditions or, in the case of high-yield bonds, a wave of downgrades or defaults. Here’s why:

Reason 1: Starting Fundamentals Are Strong

Top line growth and earnings among corporate borrowers have lost some momentum—not too surprising given the rapid tightening of financial conditions over the last year. But context matters. Corporate fundamentals are usually weak on the brink of a slowdown. Today, both investment-grade and high-yield companies enter this period from a position of strength.

Start with investment-grade issuers: revenue growth and profit margins are coming off their highest levels in more than a decade, and companies are managing their balance sheets conservatively, with both operating and sales costs declining as a percentage of revenue. That’s helped first-quarter earnings beats outnumber misses. Cyclical industries such as autos and capital goods that would be expected to struggle in a slow growth environment have done well.

Companies also did an excellent job of locking in lower yields in recent years; it will take time for the impact of higher rates to flow through to interest expenses. Leverage and coverage ratios and free cash flow among investment-grade issuers have all improved.

On the high-yield side, many issuers began managing balance sheets and liquidity more conservatively during the pandemic, helping profitability recover. The weakest issuers, on the other hand, were weeded out when high-yield defaults peaked at 6.3% in October 2020. That was less than three years ago. Since then, there simply hasn’t been enough time for the survivors to develop unhealthy financial habits.

What’s more, some defaulted bonds were replaced by those from the lowest-rated investment-grade bonds that fell into the high-yield market. These “fallen angels” helped to raise overall index credit quality. Today, BB-rated bonds—the highest high-yield rating—make up 49% of the market, compared to 43% on average over the past 20 years.

High-yield companies also extended maturity runways following the pandemic, a key component of the de-risking playbook. But many borrowers have opted not to refinance since the Federal Reserve began raising rates in 2022, as doing so would have involved exchanging a current average coupon rate of 5.8% with one closer to the market’s yield to worst of 8.5%. The result: the weighted average maturity of the broader market dropped to 5.1 years from a long-term average of 6.6 years. Over the next 12 to 18 months, the amount of debt set to mature appears manageable; we expect the US default rate to remain in a low range of 4% to 5% over that time. Beyond that, however, refinancing needs will rise. How well the economy fares over the medium term will determine how difficult refinancing will be—and underscores the importance of a selective investment strategy.

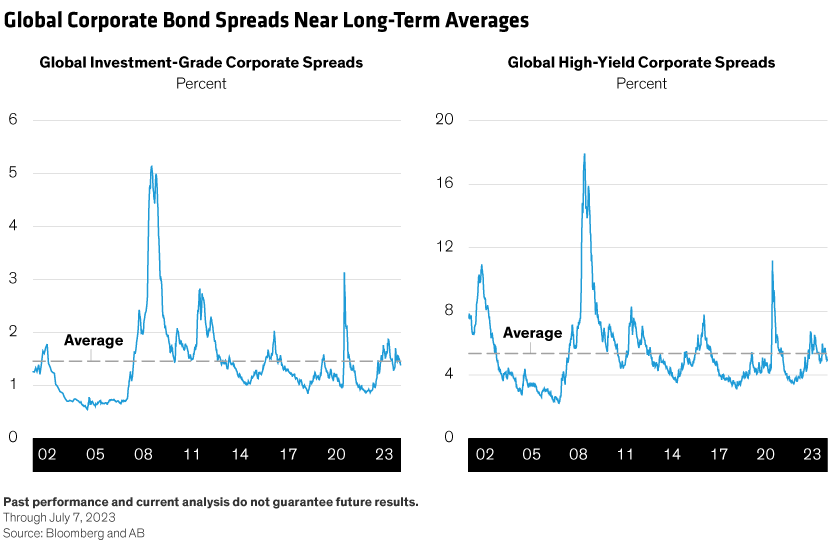

Reason 2: Valuations Are Reasonable

Credit spreads—the difference between corporate bond yields and government bond yields—are hovering near their long-term averages for both investment-grade and high-yield debt (Display), while average prices for US dollar- and euro-denominated bonds are near lows last seen during the Global Financial Crisis.

Today’s low prices are largely a function of the rise in government bond yields since early 2022; typically, it would take significant spread widening to push prices to these levels. But lower prices can provide cushion if future market volatility does widen spreads. That’s what happened in March when the failures of several midsized US banks rattled markets.

In the US, rising Treasury yields have helped drive investment-grade corporate yields higher as well. That comes with a bonus: historically, high yields have been good predictors of forward returns.

Among US investment-grade securities, senior bank bonds have particularly attractive valuations and strong starting fundamentals and may benefit from an improving technical backdrop. At the same time, bank supply continues to underwhelm, with new issues from financials down 31% on the year through June.

European banks trade at a discount to their US peers and may be sheltered from some of the challenges facing US regional banks. Globally, investors might also consider covered bonds—a high-quality segment that can serve as a buffer within the more cyclical banking industry.

Reason 3: High Yields Are Truly High

If spreads widen, however, today’s elevated yields—particularly in the lower-rated high-yield market—should provide ample cushion for investors. High-yield bonds supply an income stream that few other assets can match, and over a longer time horizon, investors are likely to convert those yields to return.

Yields on high-yield debt today are higher than they’ve been in quite some time and starting yield has been a strong proxy for a bond’s likely return over the ensuing five years. The yield-to-worst for the broad US high-yield market stands at 8.5% (Display).

This relationship between starting yield and five-year forward return held steady even during the Global Financial Crisis, one of the most stressful periods of economic and market turmoil on record. If an investor had bought high yield in May 2007 at a yield to worst of 7.5% and held onto that investment for the next five years—riding out a 36% drawdown in the high-yield market—that investor would have earned 7.6% in total return on an annualized basis.

Even so, we recommend caution when it comes to CCC-rated debt, the lowest-rated corporate bonds, which are most vulnerable in an economic downturn. Investors may also want to be choosy when it comes to high-yield bank loans, which we believe are more vulnerable in this cycle due to the impact of significantly higher borrowing costs.

But the global corporate bond market is a diverse and resilient one. Even in the late stages of a credit cycle, it can offer an attractive mix of income, stability, and potential return.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.