The CMBX.6. The acronym has splashed across headlines and become a source of controversy on Wall Street. It’s such a popular trade by speculators placing bets on store and mall closings that shorting the CMBX.6, a commercial real estate mortgage index, has been profiled in the media as the next “big short.”

Controversy has brewed because of short sellers’ assertions that the American mall is dying and that near-term defaults and losses on the CMBX.6 loan pool will therefore be high. We dispute these views.

In fact, our research shows that the American shopping mall is evolving, not dying.

It’s true that apparel retailers are retrenching. Many mall assets are headed toward obsolescence. Some mall owners are reluctant to provide new investment. As many as one-third of the 1,100 regional malls in the US are at risk.

But that’s only part of the story. Dig deeper, and the truth becomes far more complex and nuanced. Mall owners often support their assets, especially if a mall is regionally dominant. Such a mall has the potential to consolidate tenants when other, obsolete competitors exit its landscape.

Some of the 37 regional malls represented in the CMBX.6 can’t survive. But most are dominant within their trade areas, produce ample or sufficient internal cash flow to support both capex and debt service, and have enough sponsor equity to reposition to meet evolving consumer demands.

Even if the American mall were dying, short selling the CMBX.6—which holds less than half of one percent of malls in the US—to express that view is inefficient. Our fundamental research suggests that not only will overall loan losses likely be modest but also returns on the CMBX.6 will ultimately be attractive, even under extremely stressful scenarios.

In our view, short sellers may be missing critical points that support the protection seller of the CMBX.6 rather than the protection buyer:

- Most of the CMBX.6 is backed by non-retail assets that have enjoyed material growth in net operating income (NOI), considerable commercial real estate appreciation since 2012 (the year the CMBX.6 was created) and more defeased loans than usual. These assets are not expected to suffer meaningful losses.

- Short sellers expect near-term regional mall loan defaults with significant losses. But most of the 37 underlying malls produce significant internal cash flow and we expect them to continue to do so. This makes term defaults less likely.

- Mall closures and loan losses among the 37 malls are well below short sellers’ assumptions—and are likely to remain so. The regional malls in the CMBX.6 are likely to fully or at least partially pay off their loans at maturity.

- Mall loan losses may not occur as quickly as short sellers anticipate. Rather than forcing high-loss-severity liquidations of viable assets, special servicers are likely to work with borrowers to minimize losses by extending loan maturities and making loan modifications.

- Loan losses on the entire CMBX.6 collateral pool will likely be modest, with more significant tranche-level losses concentrated in specific deals.

- Thanks to the composition and characteristics of its underlying assets, returns on the CMBX.6 are likely to be much higher in the long run than short sellers expect.

The performance of this complex trade depends on a host of diverse and interdependent factors requiring equally complex analysis. That’s why the story of the American mall and of the CMBX.6 is best viewed in full color, not in black and white.

Is There Really Too Much Retail in the CMBX.6?

Speculators are betting against the CMBX.6 in part because of its heavy exposure to retail. And indeed, at the time of the index's origination in 2012, retail collateral—regional malls, power centers, strip centers, community shopping centers and factory outlets—comprised 36% of the loan pool. That represents a significant overweight to the retail sector. In comparison, just 29% of the average CMBS deal issued since 2010 has been retail loans.

Throughout this paper and for the purposes of our analysis, we employ an even more conservative metric: current loan balance net of defeased loans as a share of current loan balance. This metric gives us a current exposure to retail collateral of 44%.

While this figure sounds high, the equivalent defeasance-adjusted credit enhancement of the series has also improved since origination, from 6.8% to 10.7% for BBB– tranches and from 5.3% to 8.2% for BB. The substantially improved credit enhancement means that the default rate on the retail loans must now be materially higher in order to result in bond-level losses.

Loss-adjusted yields on the CMBX.6 look compelling even in high-stress scenarios

To demonstrate this, let’s look at an extreme example in which losses stem only from retail loans. For our hypothetical case, we’ll assign a loan loss severity of 50%. Assuming original levels of credit enhancement, the default rate must hit 37% to wipe out the BB tranche and cause a first-dollar loss on the BBB– tranche. However, when we raise the credit enhancement to 8.2%—the current defeasance-adjusted level—the default rate must rise to 49%. That’s a high hurdle, especially since, from 1995 to 2017, the historical default rate for retail loans with material losses was 10.1%, according to Wells Fargo.

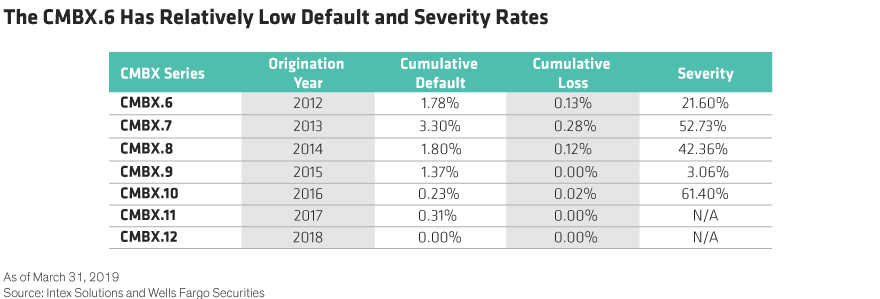

What’s more, given the CMBX.6’s seven years of seasoning, the pool has both a remarkably low default rate and rate of loans that have been liquidated with a loss (Display).

The high loan payoffs and low delinquency rate are consistent with commercial real estate’s 10 years of recovery since the global financial crisis. According to Real Capital Analytics (RCA), the Commercial Property Price Index (CPPI), a national index of all nondistressed commercial properties, has appreciated 79% since the start of 2012. Even the lagging retail sector has appreciated nearly 50%, mostly driven by non-mall properties such as community shopping centers.