For yield-hungry investors, the lure of structured notes may seem difficult to resist. However, our analysis shows that the promise of safe, outsized yields shouldn’t be swallowed whole.

Like another bank structured note we analyzed in an earlier post, n above-market-yield note we recently saw makes a bold claim: in this case, a 7% yield with a 10-year maturity. That sounds attractive in a market where 10-year Treasury bonds now offer just 2.3%.

But as always, the devil is in the details. In this case, unwary investors could be inadvertently signing up for a 10-year note with no income, an uncertain term, liquidity constraints, and potential loss of significant principal.

Heads They Win, Tails You Lose

How could this happen? For starters, although the note starts out with a 10-year term and 7% yield, its term and annual interest payments can change depending on the performance of the two relatively volatile indexes to which it’s tied: the MSCI EAFE and the Russell 2000. For instance, under certain conditions, the note is automatically called, starting in the second year. That means investors’ time horizon could shrink from 10 years to as little as 15 months.

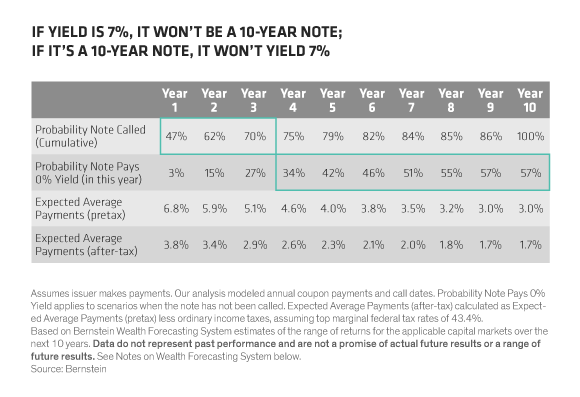

When we analyzed the fine print on this note, here is what we found: If the note’s yield is 7%, it probably won’t be a 10-year note; and if it’s a 10-year note, it likely won’t yield 7%. Consider the Display below, which shows our estimate of the likelihood that the note will be called before maturity, as well as the probability that it would yield zero in any given year.

As you can see, there is a 70% chance that the note is called within the first three years. And if the note isn’t called, the probability grows that its yield drops to 0. When you factor in the increasing likelihood that the note stops paying interest, the expected payout drops over time to 3% by year 10.

Sub-Optimal Substitute

Let’s put the note to the test by placing it in the context of an actual portfolio. Would it make a good replacement for municipal bonds? Clearly not, in our view. The note’s expected after-tax yield isn’t very attractive compared to municipal bonds—especially in later years, when the expected after-tax yield is approximately 2%.

The note is also highly correlated to equities: When stocks perform well, the note will, too. Unfortunately, the corollary is also true: When equities perform poorly, the note is more likely to offer little or no yield. Plus, because the note’s secondary market price may be unattractive, cash-strapped investors might be forced to sell off their more liquid investments at the worst possible time. In contrast, a high-quality bond portfolio would offer consistent income and is likely to appreciate in the same scenario.

You should only consider this investment if you’re willing (and able) to have your principal locked up for 10 years and possibly receive no income. If this is the case, a direct investment in the underlying equity indices almost certainly represents a better option, in our view.

Swapping equity exposure for the note represents another poor trade-off. In fact, our model estimates you’d be better off investing directly 84% of the time. Using our Capital Markets Engine forecasting tool, we calculate the median amount of return that investors would forego at almost 14% , in pre-tax terms. An equity portfolio also provides favorable tax treatment relative to the note’s ordinary income. With equities, income and appreciation will primarily be taxed at the lower long-term capital gain rates.

So the next time you’re thirsting for yield, remember the old adage about free lunches. Then, take a look at the questions we pulled together in another recent post. We’re confident that in most cases, if you pose them to your structured note provider, they’ll take a rain check on that lunch.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Bernstein does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions.

Notes on Wealth Forecasting System The Bernstein Wealth Forecasting System uses a Monte Carlo model that simulates 10,000 plausible paths of return for each asset class and inflation and produces a probability distribution of outcomes. The model does not draw randomly from a set of historical returns to produce estimates for the future. Instead, the forecasts (1) are based on the building blocks of asset returns, such as inflation, yields, yield spreads, stock earnings and price multiples; (2) incorporate the linkages that exist among the returns of various asset classes; (3) take into account current market conditions at the beginning of the analysis; and (4) factor in a reasonable degree of randomness and unpredictability.