In one of the most challenging years for markets, 2022 brought persistently high inflation, aggressive central bank tightening and heightened geopolitical risks, leaving investors with few places to hide. With major sell-offs and dislocations in practically every corner of the market, traditional stock-bond mixes like the 60/40 have struggled. As a result, many income investors are uneasy about what to expect in 2023.

Income Options Are Broader than Many Investors Think

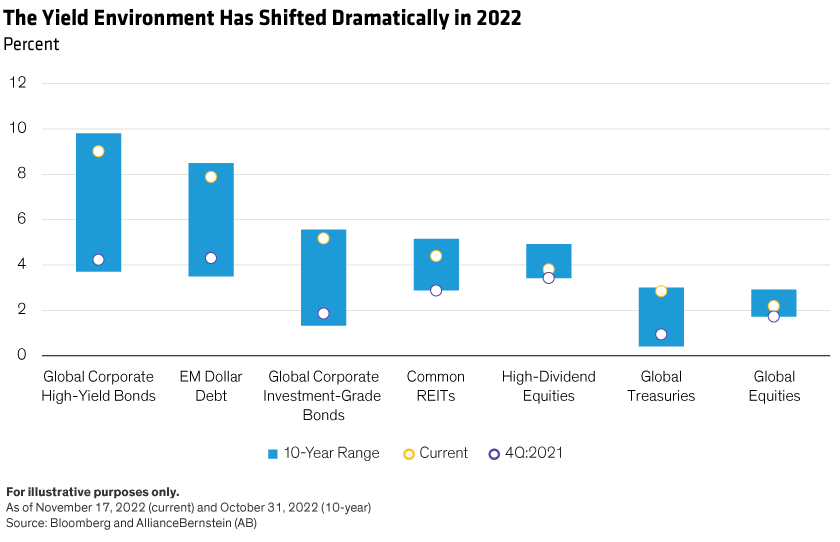

The landscape for multi-asset investors, particularly those on an income path, has shifted dramatically. Yields began the year at the bottom of their 10-year ranges but will likely finish near decade highs (Display). High-yield credit, for example, offered a yield to worst of 4.2% in late December 2021, not much more than high-dividend equities. Now, it’s more than doubled that level.

This scenario played out across income-generating investments, including investment-grade bonds, hurting near-term returns for income seekers. But it also leaves investors with a wide range of opportunities, provided they have the flexibility to consider a broad spectrum of asset classes.

Looking to 2023, we think income-oriented multi-asset investors should consider three key themes:

1. Seek Diversified Sources of Equity Return

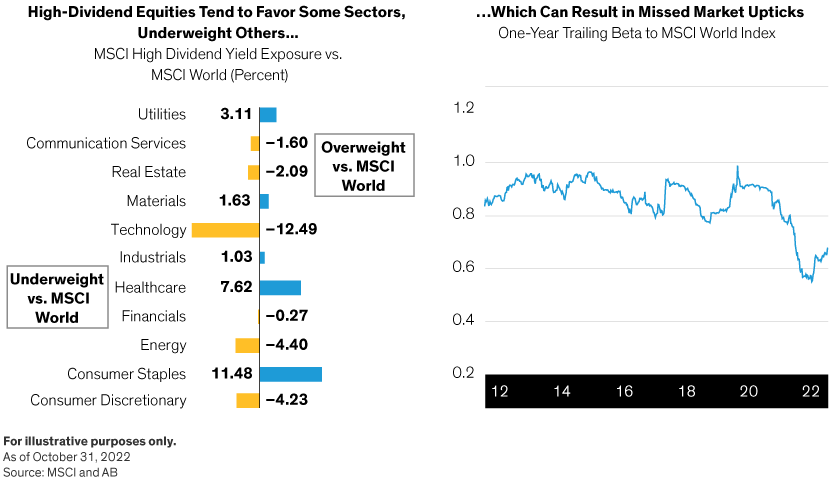

Income investors naturally favor the reliability of high-dividend stocks, especially lately. With their defensive characteristics (stable income streams and more mature business models), dividend-payers proved steadier as markets grew choppy during the year—in fact, the sell-off for high-dividend stocks was half that of cap-weighted equities in 2022.

If market volatility and economic uncertainty persist, high-dividend outperformance may continue. Then again, market leadership across equity styles and sectors can change hands over time. That’s why we believe that investors should pursue high-dividend equities with a systematic, factor-based approach in order to better balance sector and style exposure. This can help avoid concentration risk, which tends to occur in more “vanilla” approaches to dividend income (Display).

Beyond high-dividend stocks, investors should look to profitable, resilient companies trading at attractive valuations. We consistently find that companies with sustainable earnings, stable cash flows and capital-spending discipline have outperformed and, with future volatility still uncertain, can help dampen the downside.

This “quality, stability and price” discipline has also outperformed the market when inflation runs high and fast. As prices rise, companies face pressures on both the cost and income sides of their ledgers. High-quality companies with strong cash flows have more ways to protect their margins. These stocks also complement high-yield credit very well, since high-yield issuers generally tend to have more leverage and unproven track records by comparison.

2. Consider High-Yield Credit

Credit is another important income source, especially with yields up so dramatically. As global central banks aggressively raise interest rates to curb inflation, credit yields have soared and valuations are much more attractive than they were this time last year.

High yields aren’t the whole story, however; the fundamental backdrop matters too. Bottom-line pressures usually intensify this late in the business cycle: corporate excesses build and shrinking demand and tightening credit conditions challenge companies to raise capital at affordable rates.

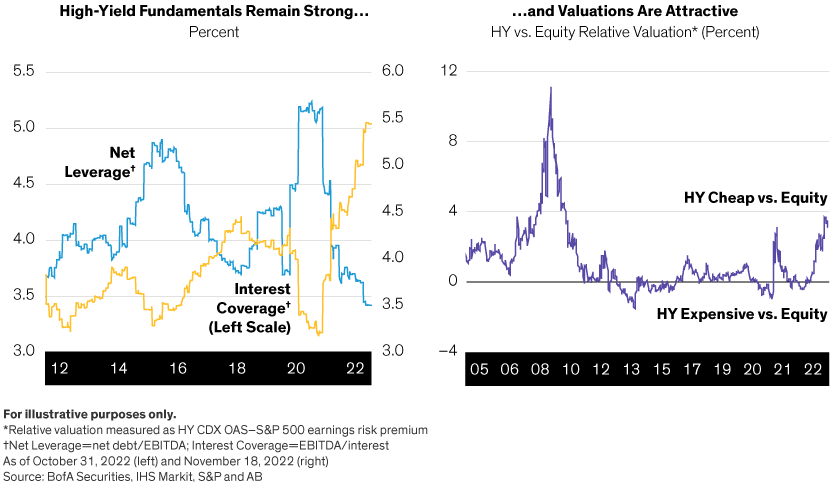

Fortunately, we’re not seeing such high distress levels in the current late-cycle environment. Issuers’ fundamentals remain strong and of high quality, and they took advantage of low rates during the pandemic to restructure debt and extend maturities. Today, high-yield debt-servicing ability is its strongest in many years, while valuations remain very attractive—especially versus equities (Display).

We expect default rates, now at historic lows, to rise but stay below averages—and well under levels seen in past recessions. US high-yield issuer ratings reflect this; more than half of issuers by market value are now BB-rated, and those with CCC ratings are at the lowest level in more than a decade.

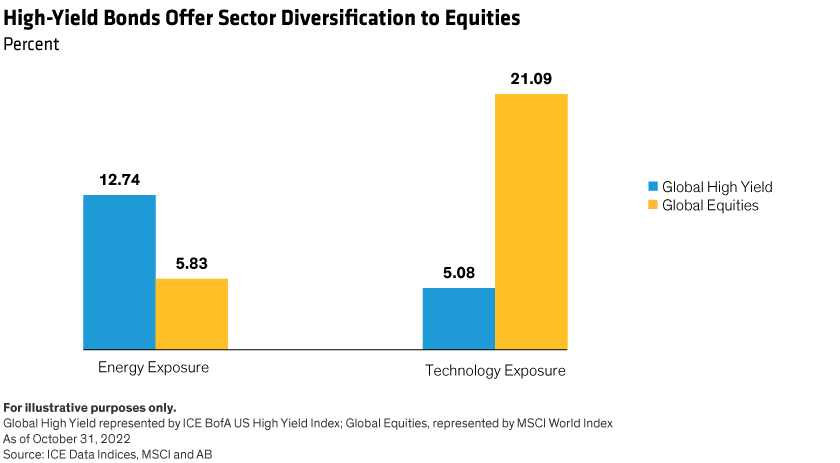

Moreover, the high-yield bond index leans structurally toward energy and less toward technology firms, in contrast to the broad equity market. So, with energy currently benefiting from elevated commodity prices, high-yield exposure is a helpful equity diversifier (Display).

Credit valuations and fundamentals are relatively favorable. But caution and selectivity remain the watchwords if heightened volatility, rising rates and late-cycle dynamics continue to play out in early 2023.

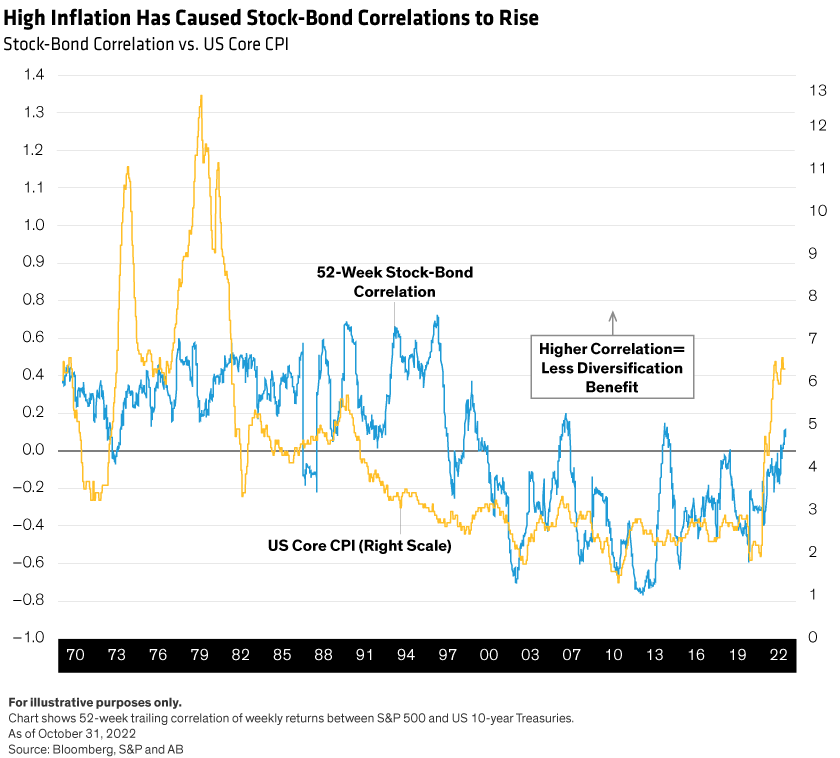

3. Revisit the Role of Government Bonds as Diversifiers

Global treasury bonds have long been viewed as a safe haven asset—a reliable backstop during periods of market stress. In 2022, though, high inflation and rising rates sapped government bond returns as equities tumbled, eroding the traditional diversification benefit of duration exposure.

Sharply rising bond yields made holding government bonds somewhat painful for most of 2022, but we think they still have a role within multi-asset income strategies in 2023. Their yields are the highest in 10 years, making them a viable income source. In our view, current yields have largely priced in the risks of further monetary policy tightening, so we expect less volatility and downside risk from here.

The diversification benefits of government bonds could return now that inflation is showing signs of peaking, based on historical trends. We expect the correlation between stocks and bonds to again help diversify returns (Display) and reduce downside risk if we enter a stretch of economic stress.

To sum things up, the outlook for 2023 may feel somewhat gloomy, with growth potentially slowing, inflation still high and tighter financial conditions. But compelling valuations, combined with higher yields across a range of fixed income and equities, could make next year a brighter one for income investing. Staying flexible and selective in asset-allocation exposures will be key to success.

Karen Watkin is Portfolio Manager, Multi-Asset Solutions and Edward Williams is Product Manager, Multi-Asset Solutions at AllianceBernstein (AB)

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.