With global markets growing more volatile, we’re often asked what we think are the most underappreciated risks that investors face today. One in particular stands out: currency risk—especially for non-US dollar–based investors.

To see what we mean, let’s consider the case of institutional investors in Asia. In recent years, many have begun to move away from narrow investment mandates and toward more flexible, well-diversified global multi-asset strategies—a move we think can help to generate consistent returns.

As part of this diversification trend, these investors have sizeable exposures to global currencies, with a significant proportion to the US dollar. Very few investors hedge that currency exposure appropriately, making portfolios vulnerable to unintended currency risk that can hurt performance.

One reason for the dollar’s dominant role in these portfolios might be that most global asset managers offer many investment services denominated in dollars. And the US accounts for a large share of global equity and bond indices, ensuring that the dollar plays a prominent role in global mandates.

Why are so many investors with liabilities denominated in their local currencies comfortable being long the dollar? Probably because doing so has boosted performance. Thanks to a prolonged rally, the dollar is hovering near a two-year high against a basket of major currencies—and soared against many emerging-market (EM) ones.

The dollar rally has had a lot to do with the relative strength of the US economy, which until recently allowed the Federal Reserve to raise interest rates above those in other advanced countries. With policy rates at zero or below, and with bond yields negative in the euro area and Japan, the dollar is still perceived by many to have more room to rise, despite the negative US current account and fiscal deficit.

Time to Manage Currency Risk?

But all trends eventually end. A worsening US-China trade war and slower global growth have already pushed the Fed to cut interest rates, and it’s expected to do so again this year. If Washington and Beijing reach a trade deal before next year’s US presidential election, growth could rebound and the dollar may decline, particularly against currencies from Asian exporting countries that are currently being hurt by trade tension.

In our view, now may be the time for investors to start exploring ways to better manage their currency risk. Over many years, large currency movements can take a big bite out of returns and potentially derail portfolios from their investment objectives.

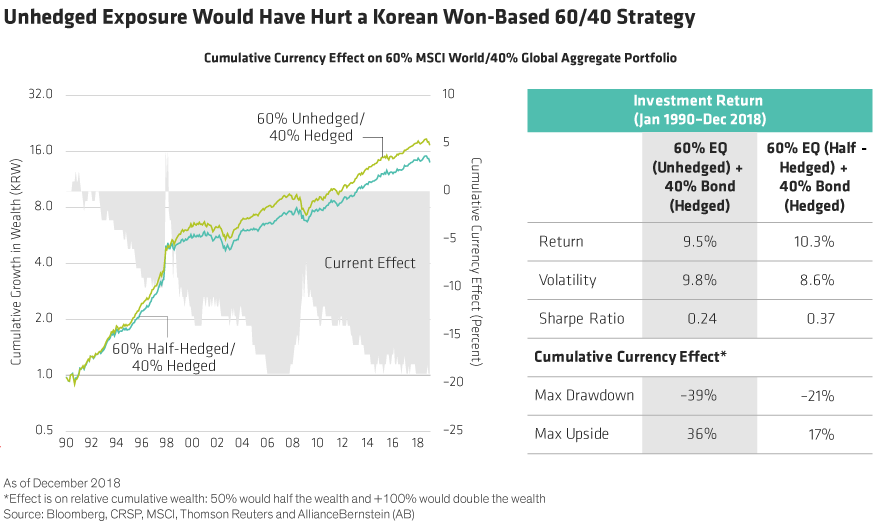

As the following Display shows, a South Korean investor who did not currency hedge the equity exposure in a typical 60/40 portfolio would have seen lower risk-adjusted returns and a larger maximum drawdown over the past 28 years than an investor who hedged half of the dollar exposure in the equity allocation. This is largely because the won provided a strong total return for much of this time, the result of a large interest-rate differential between it and other currencies.

Asian investors with unhedged exposures don’t need a dollar sell-off alone to run into trouble. Global equity and bond indices also have sizable exposures to the euro, yen, British pound and other majors, which can also hurt if they weaken against investors’ home currencies.

The Thai baht, for example, has been an outlier among EM currencies, having risen more than 5% against the dollar since early 2018. That would have hurt Thailand-based investors who didn’t do much hedging of foreign currency exposures. The takeaway here? Investors with local-currency liabilities should have at least some local-currency exposure.

How Much Hedging? It Depends

It’s true that wide interest-rate differentials between the dollar and other currencies make hedging costly for Asian and European investors today. For instance, a Japanese pension fund that wants to hedge dollar exposure must sell the cash rate of the currency it’s hedging from—more than 2% for the dollar—and buy the cash rate of the yen, which sits at zero.

But does avoiding the high cost of hedging justify accepting the high risk of an unhedged allocation? We think it makes more sense to strategically hedge dollar exposure. That doesn’t mean hedging away all currency risk—and the potential returns it can offer. In many cases, keeping exposure only to lower returns available on local assets would make it hard for investors to close liability gaps. But we think partially hedged allocations may make sense. For some investors, it might be a 30% hedge ratio. For others, perhaps 50%.

Other important considerations include the long-term fundamentals of foreign currencies and an investor’s home currency—and the diversification benefits currency exposure can provide.

Currency Hedging: Don’t Set It and Forget It

We think it’s important to dynamically manage currency risk in any multi-asset solution. That means retaining the flexibility to be tactical and adjust hedges as needed. Such adjustments might be based on changing investment goals, economic conditions or asset valuations. They can also depend on what’s going on in the world. Today, that means things like Brexit and the US-China trade war. Passive hedging—setting a ratio and forgetting it—isn’t likely to offer the same level of protection.

It’s also possible to treat currencies as another potential generator of excess returns, or alpha, along with equity, bonds and other asset allocations. But because exchange rates can be volatile, this strategy requires a high tolerance for risk and a hands-on manager with a firm grasp of existing currency risk.

There’s no doubt that the US dollar’s gains have been a tailwind for unhedged multi-asset mandates of late. But if other currencies start to rebound against the greenback, these investors could see a portion of their recent gains reversed. We think currency exposure is an underappreciated risk that deserves consideration.

Leon Zhu is Portfolio Manager, Global Currency Strategy, Multi-Asset Solutions at AllianceBernstein.

Aditya Monappa is Head of Business Development, Multi-Asset and Alternatives, Asia ex-Japan at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.