Roughly 60% of Americans make a New Year’s resolution every year—half of which focus on achieving a healthier lifestyle. But while resolving to improve your physical well-being, don’t neglect your financial health either. Just like tracking your exercise or monitoring your heart rate is important for your overall wellness, there are important financial numbers you need to know to answer the all-important question: Do you have enough money to maintain your lifestyle, and give to your family or favorite charity? Unfortunately, many New Year’s resolutions fall by the wayside after a few weeks (or days)! Luckily, understanding your financial health is a much easier feat.

What Do You Need to Sustain Your Lifestyle?

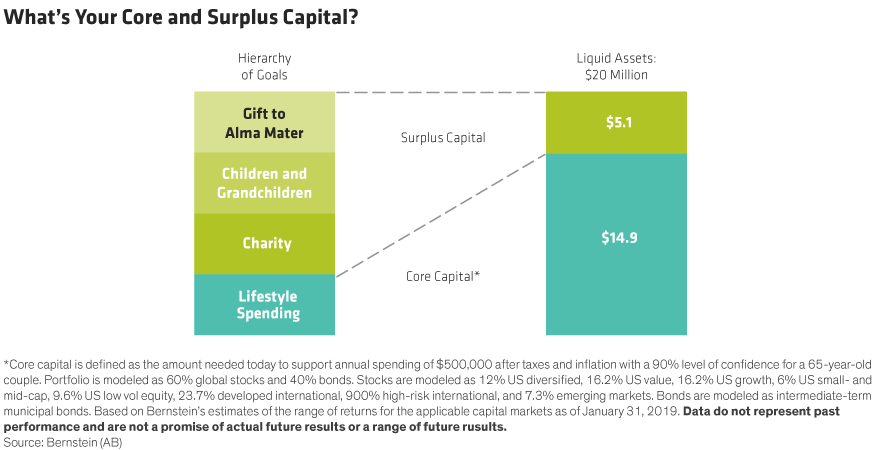

We developed a framework to help you understand how much money you need today to sustain your lifestyle over a lifetime, so that you can know your capacity to give or spend. We focus on two types of capital—core and surplus. Core capital is the amount of money needed today to secure living expenses for the rest of your life. Assets above the core capital are surplus that could be used on big, optional purchases—such as a country home—or to give to friends, family, or charity.

Our Wealth Forecasting SystemSM estimates core capital by making a few conservative assumptions—you may live beyond what mortality tables suggest, that high inflation might drive up your spending needs, and that deep bear markets may depress portfolio values, at least temporarily. Your asset allocation, age, and how much you may need to draw from your portfolio over time are key drivers in calculating your core capital. Let’s see how it works:

How Strong Is Your Core?

Addy, a recently retired 65-year-old, has $20 million invested in a moderate allocation portfolio. She spends $500,000 per year, after taxes. She’s considering giving $1 million to her alma mater, which is building a new campus museum. Our analysis shows that she needs $14.9 million to support lifetime personal spending, and has $5.1 million of surplus capital, certainly enough for that $1 million gift she’d like to make. That’s great! The next question is, how should she structure her gift?

Structure Matters

Before Addy makes a large, irrevocable gift, she should determine how to best structure the gift. Instead of gifting the $1 million all at once, for example, she could make smaller (but still substantial) annual gifts, which could be stopped if an unexpected medical expense arises, or she becomes enamored with another cause. Addy could also use a variety of charitable vehicles to provide her alma mater with gifts for many years but leave the remainder to family. Alternatively, she could provide her children with an annual income, and leave the remainder to the school. Or, after careful reflection, she could proceed with her original plan, or possibly give her alma mater even more. Once she knows her capacity to give, the possibilities of how to structure her gifts are vast.

A Holistic Approach

Not unlike taking a holistic approach to wellness that focuses on physical health, emotional well-being, and spiritual centering, your wealth strategy should consider all your planning goals—your desired lifestyle, family legacy, and charitable inclinations. It starts with knowing two numbers—your core and surplus capital. So as you think about what you’d like to accomplish financially in 2020, starting with knowing your core and surplus capital will get you on your way.

The views expressed herein do not constitute and should not be considered to be legal or tax advice. The tax rules are complicated, and their impact on a particular individual may differ depending on the individual’s specific circumstances. Please consult with your legal or tax advisor regarding your specific situation.