As the summer progresses, US vacationers are out in force while the European and Asian holiday scene remains relatively subdued. Identifying travel-related trends can help investors capture the global recovery from the pandemic mobility shutdown in diverse sectors.

COVID-19 has accelerated many behavioral changes for consumers. But one tradition—vacations—is highly unlikely to change. If anything, we believe the suppressed travel of the last 18 months is likely to give way to a travel boom when people feel safe to get back on trains and planes and to stay in hotels. The recovery of travel around the world is unlikely to be uniform. But with the help of big data, we can observe how vacation appetites are playing out in real time this summer and develop actionable investment insights.

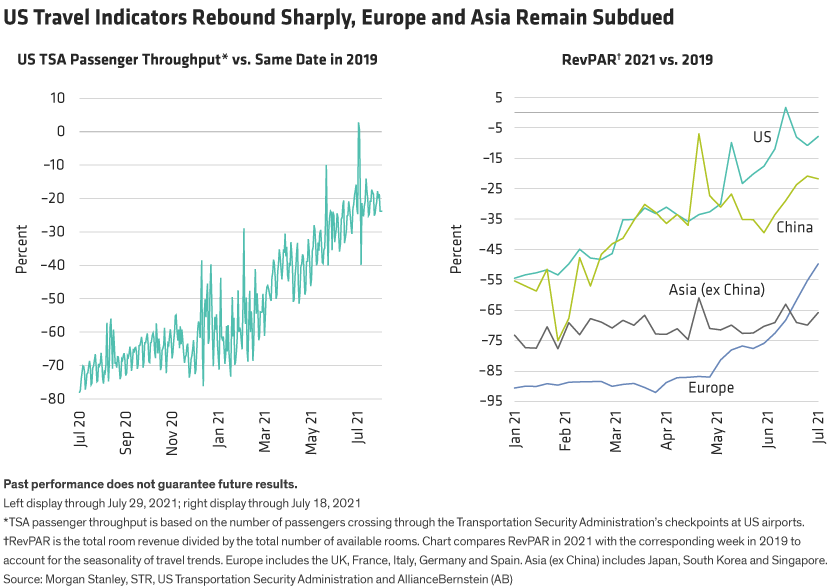

Major Milestone in US Hotel Bookings

Travel has recovered in fits and starts so far. In the US, a major milestone was reached over the July 4 holiday as passengers screened at US airports exceeded pre-pandemic levels for the same week in 2019 (Display, left). Hotel bookings confirm the US recovery.

For example, higher prices at US hotels have helped offset volumes that remain slightly below 2019 levels. As a result, RevPAR, a measure of nightly revenues to the hotel industry per available room-night, has been steadily rising and briefly exceeded the pre-COVID-19 level in July (Display, right)—well before many Americans are comfortable traveling. Good luck getting a holiday hotel reservation!

But the reopening trends seen in the US aren’t universal. Europe and Asia are still suffering from depressed levels of activity and the travel and leisure industry may be facing another “lost summer.” Indeed, RevPAR statistics for Europe and Asia are still down sharply from 2019 levels.

From Vaccinations to Vacation

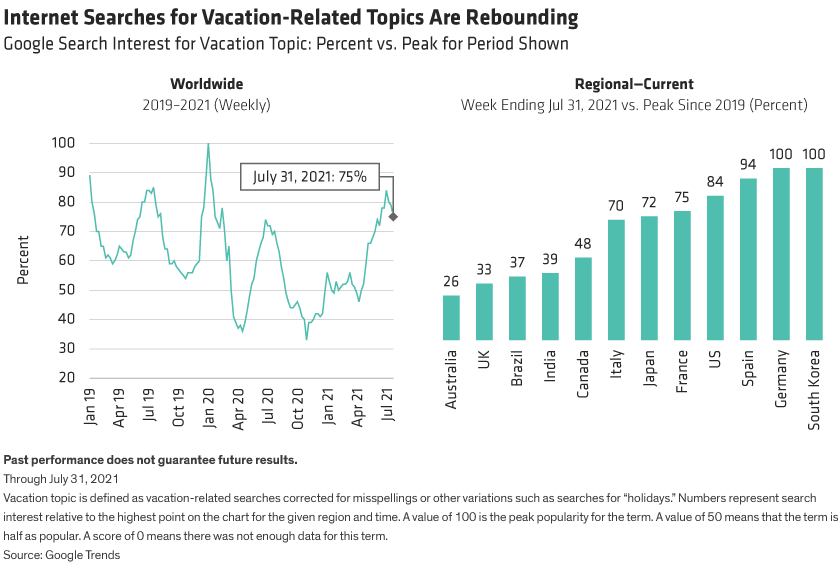

As investors, our goal is to anticipate what happens next, with an awareness of appropriate timeframes. Looking at vaccination rates by country as well as Google searches for vacation-related topics provides insights.

Vaccination rates in the US were initially well ahead of the rest of the world. By April 30, 44% of the US population had received at least one dose of a vaccine, according to Our World in Data. This compared to rates of around 25% in Western Europe. But by the end of June, the US and Western Europe both recorded similar one-dose vaccination rates of approximately 55%.

While the Delta variant is causing COVID-19 cases to rise around the world, when we are on the other side of this spike, we believe Western Europe will start to look more like the US in terms of mobility and activity. This possibility isn’t well recognized today. In fact, Google searches for vacation-related topics have recovered worldwide to about 75% of their pre-pandemic peak. But it varies by country, with interest in Germany and South Korea surging, Spain and the US near pre-pandemic peaks, while Australia and the UK still show little interest in holiday-making.

Investment Insights: Beyond “Pure” Travel and Leisure

So how do these data-driven insights translate to portfolio actions? It all depends on an investor’s risk appetite. Cruise ships, airlines and hotels might seem like the obvious way to invest in a travel rebound. But these companies are the higher risk, higher reward options; if a new variant emerges post delta, the recovery would be pushed out again and “pure” travel stocks would face a setback.

Instead, look for strong businesses that are likely to enjoy an added boost from a normalization of vacationing. This is a lower-risk approach, targeting companies outside the transport and leisure industries that also benefit from renewed travel.

Some financial services companies are important enablers of travel. When cross-border travel picks up, vacationers will use their credit cards for more purchases in foreign currency. Cross-border transactions are very profitable for credit card companies such as Mastercard and Visa. In Europe, a revival of leisure travel would also boost regional payment activity. That’s good news for companies like Worldline, a France-based operator of transaction-processing platforms across Europe.

In recent years, travel bookings have become a predominantly digital business. So as people around the world start to vacation again, online bookings are likely to rise, fueling revenue growth for companies like Booking.com and AirBnB. Beyond these direct beneficiaries, broader internet searches for travel-related bookings can be expected to rise. For example, when Google searches convert to travel bookings, it generates real revenue for Alphabet.com, Google’s parent company.

Travelers love to shop. Several luxury brand companies have historically enjoyed solid revenue gains from tourists. Easing travel restrictions could provide a brisk sales boost for products from cosmetics to swanky handbags. This could be a boon to luxury goods companies like Estée Lauder and L’Oréal, especially given the pent-up spending power accumulated during last-year’s pandemic shutdown.

Vacationers on the move are an important sign of a return to normalcy in the global recovery. Investors should follow trends in regions that haven’t fully recovered to identify companies with solid businesses in diverse industries that are poised to enjoy an added boost from a return to travel. The absolute upside might not be as exciting as investing in companies that are direct winners from a binary travel boost; yet, we believe the risk-adjusted return potential is more attractive by pursuing great businesses that will get even better as people hit the road again.

James T. Tierney, Jr. is Chief Investment Officer of Concentrated US Growth at AllianceBernstein (AB)

Dev Chakrabarti is Co-Chief Investment Officer—Concentrated Global Growth at AB

Jonathan Berkow is Director of Data Science for Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AB. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable.