After a strong rally for value stocks in recent months, some investors are wondering if the rebound will continue. We think several forces are unfolding that should support a continued value resurgence as the world emerges from the ravages of the pandemic.

Value equities have been enjoying stardom after many tough years. The MSCI World Value Index has surged by 33.2% since November, outperforming growth stocks by a wide margin (Display). Investors have rediscovered the appeal of undervalued stocks, which often are facing controversy, in a diverse set of markets from Japan to Europe to the US. Since COVID-19 vaccines were unveiled in late 2020, hopes for an accelerated macroeconomic recovery fueled strong returns from cyclically sensitive sectors such as financials and energy, which are more heavily represented in value benchmarks.

Value’s Weakness Is Unprecedented

So, what’s been driving the value recovery so far, and is there more to come? To answer that question, we need to first look back at equity market trends before the pandemic. It’s no secret that value stocks have had a rough ride in recent years. Yet the sheer scale of the underperformance simply has no precedent in modern market history.

In the past, value stocks delivered consistently strong returns over time. In the US market, where the longest data history is available, the cheapest 30% of stocks, based on price/book value, outperformed the most expensive 30% of stocks by an average of 4.1%, annualized on a 10-year rolling basis since 1936. But by the end of 2020, as the COVID-19 pandemic devastated economic growth, the trailing 10-year returns for the cheapest cohort of stocks had underperformed the most expensive stocks by about 8% (Display). This lost decade was by far the worst period on record for value, well beyond the poor performance seen during the internet bubble of 2000 and even the Great Depression of the 1930s.

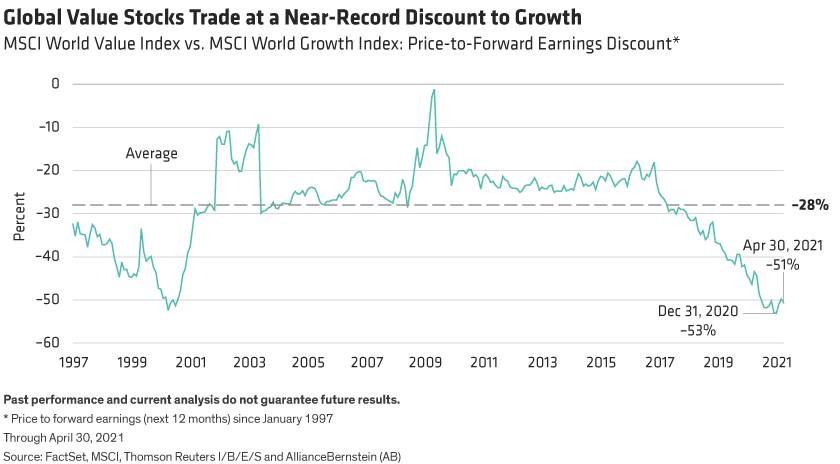

As a result, value stocks were left trading at a historic discount compared with growth stocks. Based on price/forward earnings, the MSCI World Value was 53% cheaper than the MSCI World Growth Index (Display) by the end of 2020. That’s nearly double the 28% average discount that global value stocks have traded at since 1997 and a deeper discount than at the peak of the dot-com bubble in 2000—a period followed by several years of supercharged value outperformance.

Value’s underperformance was widespread. By the end of 2020, in industries as diverse as consumer durables, healthcare equipment and telecom services, value stocks were cheaper than they’ve been, relative to growth stocks, at any time since 2001. The same was true of value stocks across most major regional markets.

Even after the recent rally, the discount of value stocks to growth stocks remains exceptionally wide. By the end of April, the MSCI World Value still traded at a 51% discount to the MSCI World Growth—well below the 28% long-term average, as shown above. And across sectors and regions, the discounts have only moved slightly off the historical extremes seen at the end of 2020.

Opportunity or Trap?

It’s tempting to conclude that value’s bargain-basement prices alone represent a screaming buy signal. But that would be too simplistic, given the persistent underperformance. As experienced value investors know all too well, cheap stocks can get cheaper, and extreme discounts may signal a value trap. Sometimes a stock is cheap because the company’s earnings have become permanently impaired.

For investors, the deep discounts present a conundrum. Do they reflect a new and permanent reality that investors are ignoring—the imminent death of value investing? Or do these discounts represent pent-up performance in value stocks that may signal outstanding recovery potential as market conditions turn?

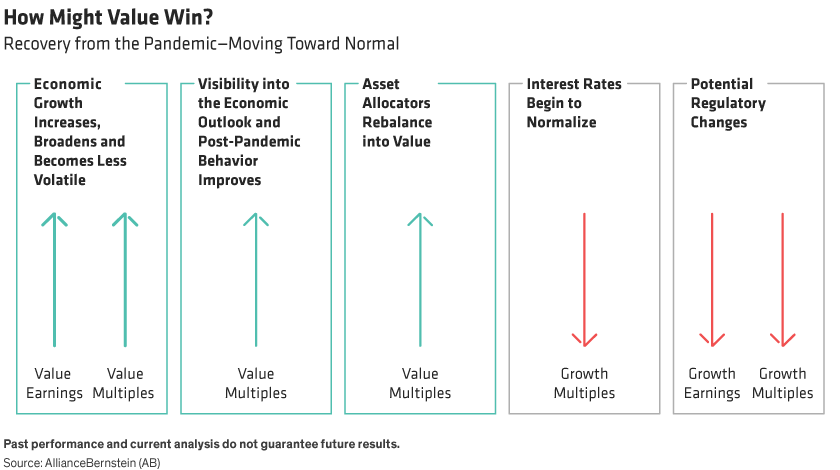

In our view, the dramatic effects of the pandemic may be a catalyst for change, as five key developments (Display) could foster an unwinding of the extreme divergence of value and growth stock valuations in the coming years.

Value earnings and multiples should benefit as economic growth increases and broadens, while visibility into post-pandemic behavior improves. These trends could also prompt asset allocators to shift more funds toward value portfolios. A normalization of interest rates from historic lows—as we saw in early 2021 with the rise of 10-year US Treasury yields—could put pressure on growth stock multiples, which tend to benefit more from lower rates. Growth stock multiples may also suffer from potential regulatory crackdowns on megacap growth giants in the technology and consumer sectors.

COVID-19 has produced the ultimate value controversy. Many companies that are struggling with uncertain long-term prospects have been severely punished. Yet market conditions have also created what we believe is an unprecedented recovery opportunity for investors willing to initiate or expand allocations to value stocks today. Indeed, in the first quarter, many value companies posted strong earnings growth, so even as share prices advanced, their P/E multiples remain attractive.

In our next blog, we will examine why growth stocks dominated market returns in recent years. This analysis helps explain why the market forces described above could fuel a continuation of the value equity recovery in the months and years ahead.

This blog is the first excerpt in a series based on our recent white paper Value’s New Hope, Will the Pandemic End be the Catalyst?, published in March 2021.

Avi Lavi is Chief Investment Officer—Global and International Value Equities; Portfolio Manager—Global Research Insights

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.